Peering through the fog

The Blind Squirrel's Monday Morning Notes, 29th July 2024.

The 🐿️ is back in the ‘Lucky Country’ and the (jet lag inspired) fog of sleep deprivation is making it even harder to parse this past fortnight’s market moves and economic data.

Momentum is clearly stalling on the great Generative AI trade of 2023 and 2024. The question to get right is whether or not it continues to unwind, potentially taking the broader market and an economic soft landing with it.

Peering through the fog

A younger 🐿️ never used to suffer too greatly from jet lag. Alas, not this time! The fog of sleep deprivation is certainly making it harder for this rodent to parse this past fortnight’s market moves and economic data. Data which also seems to be suffering from its own form of extreme desynchronosis (the posh word for jet lag!).

The real time economic data is delivering a barrage of mixed signals. The latest upward revision to the GDP Nowcast from the Atlanta Fed sits uneasily with a 12-year high in credit card delinquencies. A deceleration in the reduction of core PCE inflation still well above the Fed’s 2% goal sits at odds with a fully priced interest rate cut for September.

A mixed buffet of high frequency data from Apollo’s Torsten Slok would appear to back up the Atlanta Fed’s buoyant GDP nowcast.

Is this really the backdrop against which the futures markets, economist community and Fed Chair Powell(!) would appear to be desperate to start pricing cuts?

Regular readers will know that the 🐿️ leans towards a view that the underlying economy is weaker than the headlines (and some of the high frequency hard data) suggest. Most consumers - even those more fortunate AlsoLux™ consumers - are already feeling the pinch. Prosperity would appear to be limited to those that are either a direct beneficiary of direct government spending or those with significant exposure to appreciating financial assets.

The former group, largely the direct and indirect recipients of the (now, let’s face it, hilariously named) Inflation Reduction Act funding, are crushing it! Contrast this with the contents of the excellent Treppwire podcast (part of the 🐿️’s essential weekly listening diet) where the agonies in the world of commercial real estate are listed out in a way that reminds one of war time casualty lists…

The happy owners of (until recently) rapidly appreciating financial assets are faced with a different dilemma. The 🐿️ is a huge fan of Julian Brigden’s ‘Hyper Financialization’ thesis around US equity markets. Julian posits that in a world where the central bankers are more focused on the ‘full employment’ element of their mandate, stock prices and the real economy are wholly interlinked.

Herein lies the problem. CEOs prioritize cost-cutting (via headcount and capex reduction - the only tools truly within their control) when their stock prices decline. We all remember just how effective that can be. The markets were quick to celebrate Zuckerberg’s newfound religion with regard to headcount and capex discipline in Q4 2022.

The tech giants have a different problem to deal with this time - the generative AI hype machine. Wild extrapolation as to the economic possibilities associated with AI’s large language models has led to what this rodent is beginning to view as a giant malinvestment boom among the hyper-scalers.

Back in early June in ‘It 'AI'-n't Necessarily So!’, we wrote “For now, picks and shovels to the AI gold rush are selling briskly, but this is no 19th Century California. Some nuggets are going to need to come out of the riverbed pretty soon or there is going to be a Metaverse-style investor rebellion and capex budgets will need to be curtailed rapidly. The froth of hype and excitement could recede as rapidly as it emerged in late 2022.”

More recently, a reasonably better-known sell side shop called Goldman Sachs has dared to say that quiet bit (about AI capex) out loud. The market shares similar attributes to the school playground and one of the big lads on the football team just spoke out. Talking down the latest hype cycle may have just become normalized. We may be closer to that investor rebellion than I previously thought.

Is it really possible that a retreat from the AI-related capex plans by the tech overlords could be pulled off without reversing the trillions of dollars of market capitalization that have been added to their businesses over the past 18 months? To do so would require a truly Olympic narrative shift! Those ‘secondhand datacenter use cases’ are going to need to be spectacular…

With this I want to take Brigden’s hyper-financialization theory one step further. Julian highlights the direct link between equity markets and unemployment. I believe that the past 2 years have clearly demonstrated that this financialization extends directly to economic growth.

Boomers earning 5% interest in money market accounts may drive economic activity at the margin, but lately it is strong equity markets that appear to have been a key forward indicator of economic activity and growth. It is not hard to paint a picture in which a popping (or even gentle deflation) of the AI hype bubble is actually what pushes the soft landing currently being priced by the market out of reach.

2 weeks ago, your 🐿️ was musing at how a failure of the ‘Great Rotation’ (from big tech to small caps) could be heartbreaking for many value investors.

Heartbreak has been spared (save for the uranium bulls among us!). The rotation into (the very narrow door that is) small caps has continued. For the 🐿️, this is more likely to be a function of physics (it does not take much of a shift in fund flows to move those small caps) than fundamentals (I am dubious that this move signifies a ringing of the ‘mission accomplished’ bell for that soft-landing).

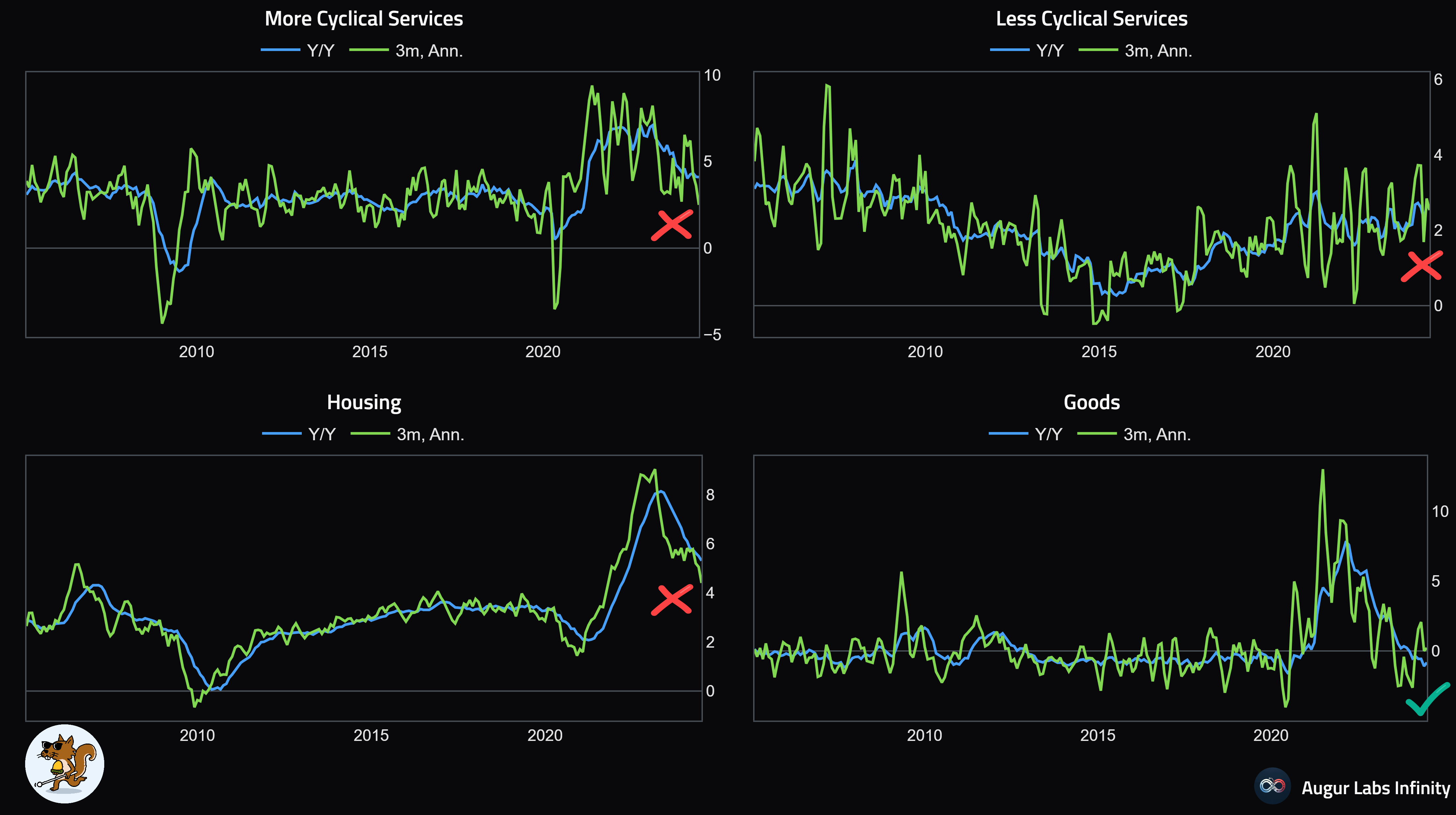

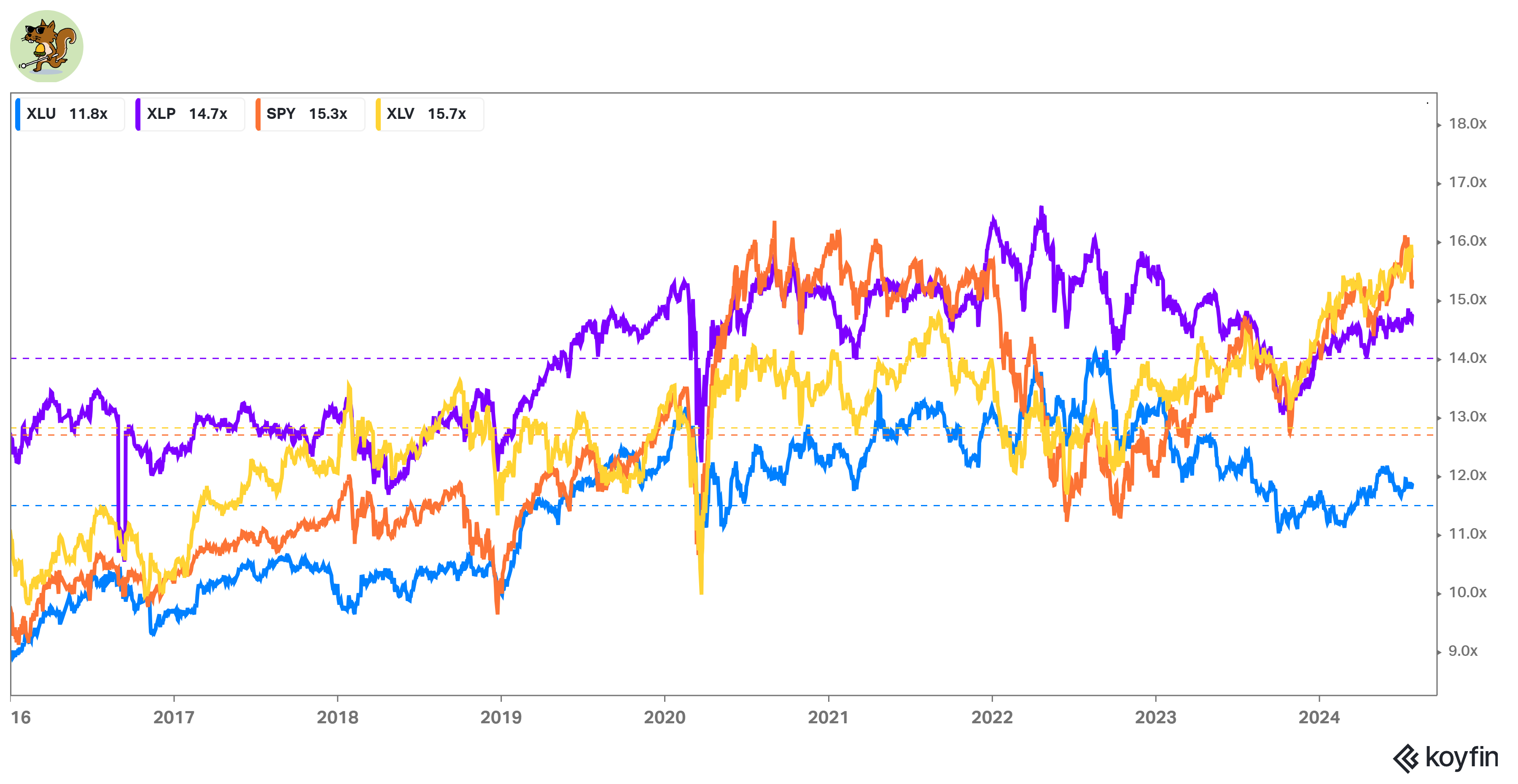

The table below plots performance for the Russell 3000 over the past week. The money is clearly running (for now) to ‘Grandpa’s defensives’ (healthcare (except for ‘mo-mo’ stock Eli Lilly), consumer staples and utilities) rather than getting into an earnest hunt for value exposure.

However (and as usual!), we have plenty of choices for a supporting narrative. It is of course possible that the market is deciding now to ‘reprice’ the Generative AI opportunity. Or are we just dealing with an ordinary course cooling off of what has been one of the great momentum trades of the past couple of decades?

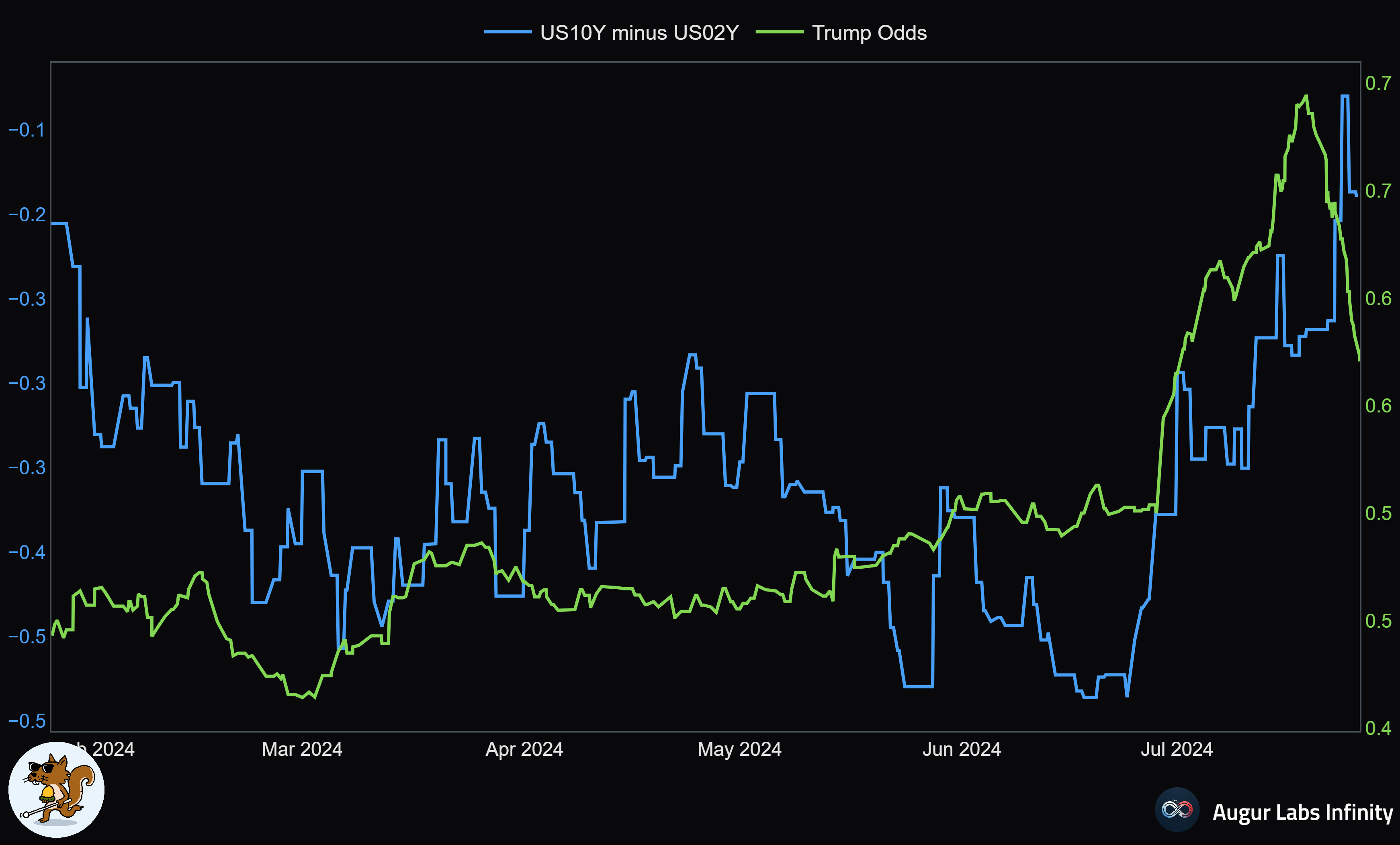

Many pundits are desperate to attribute the shifts in asset prices to the change in the ‘runners and riders’ for November’s presidential election. In You can't face it, but bonds are watching, I was certainly guilty of musing that the Biden / Trump debate had fired the starting gun on a ‘bear steepener’ in US Treasury markets.

The yield curve inversion has continued to retreat even with Biden stepping out of the race. The bond market is perhaps not yet prepared to accept that Trump’s winning odds moving from 69% to just over 55% justify any reduced concern about long duration yields.

What if the bonds are looking at the recent weakness in equities and seeing what the 🐿️ sees about this potentially leading to economic weakness. Yield curve un-inversion has a near flawless track record as a harbinger of recessions:

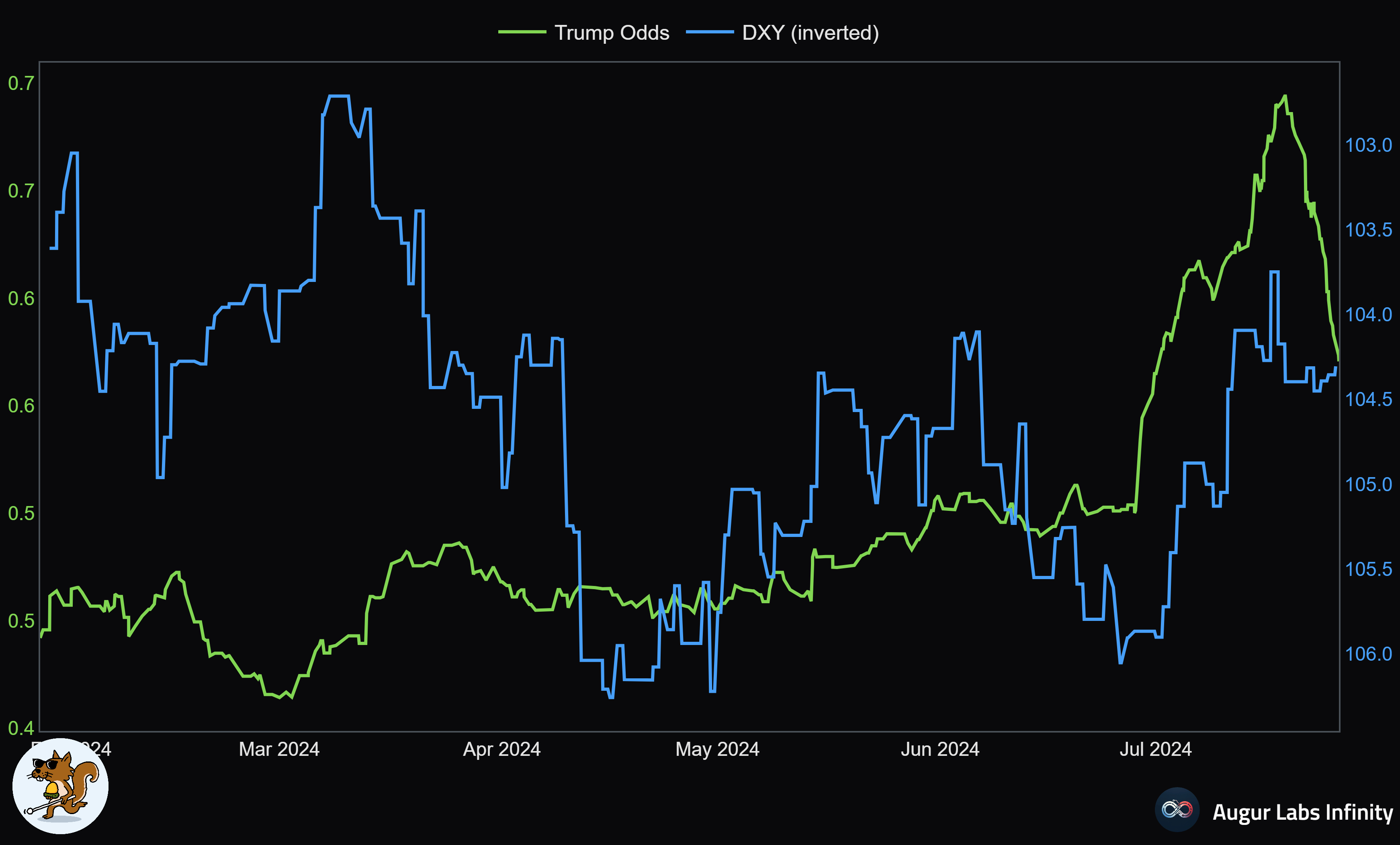

There has been much discussion of a second Trump administration taking steps to improve US manufacturing competitiveness via a weaker dollar. I do not believe that FX markets are taking this risk too seriously for now.

Many are trying to link the recent Yen strength to this narrative. The 🐿️ (while thinking that the Yen is massively undervalued) is firmly in the camp that the move is merely (for now) a function of the unwind of a very crowded carry/ momentum short position in the currency.

Who knows if the Bank of Japan will hike rates next week (I agree with FX Poet Andy Fately that softer Tokyo CPI probably does not support such a move)? The CTAs (judging by DBMF 0.00%↑, Andrew Beer’s CTA replicator ETF) are not waiting to find out. I joke of course - CTAs do not care what central bankers do or have to say! But the machines know that the trend is no longer their friend.

The best correlation between financial assets and Trump’s odds is with the large cap tech giants of the Nasdaq. Even better than with DJT 0.00%↑, The Donald’s very own meme coin!

I could develop a narrative around the FTC’s ‘Big Tech’ trust-buster Lina Khan now having bi-partisan support (JD Vance is apparently a fan) but I think the reality is more prosaic. Momentum is stalling on the great Generative AI trade of 2023 and 2024. The question to get right is whether or not it continues to unwind, potentially taking the broader market and an economic soft landing with it.

In Section Two this week, we figure out what this means for the portfolio. The 🐿️ has a funny feeling that it does not mean we need to be loading up on small cap value!

Don’t miss out! Please consider becoming a paid subscriber to receive the other 60% of the content we produce, Discord access and even merch!

Some feedback below from happy readers that have already taken the leap.