Red Markets in Red Wine

The Blind Squirrel's Monday Morning Notes, 24th June 2024.

I think we are now seeing increasing evidence of that the squeeze of higher interest rates is hitting the more affluent.

We start with fine wine before looking at Rolexes, Birkin bags and Ferraris.

In the world of luxury, there is a big difference between UberLux and AlsoLux.

Basically, it is now pretty much only those on the waiting list for a Birkin bag or a Ferrari electric supercar that are not feeling a roll over in the economy. The impact of fiscal spending over the past 4 years has created a mirage of economic prosperity in the official data. The reality is very different.

Don’t miss out! Please consider becoming a paid subscriber to receive the other 60% of the content and plenty of other good stuff!

Red Markets in Red Wine

There has been plenty of column inches dedicated to the economic squeeze on the lower income consumer. I think we are now seeing increasing evidence of that squeeze hitting the more affluent.

We start with red wine. Over the years, the 🐿️ has had a tradition of gifting a case of fine wine to nephews, nieces and godchildren when they are born.

Like many collectibles, fine wine bought en primeur and stored in the bonded warehouses of the major wine merchants has enjoyed terrific price performance. This alternative asset class has attracted a growing universe of investors over the past 20 years. Up until the beginning of 2023, the value of collectible wine had been compounding at over 9%. A tax-free capital gain in many jurisdictions.

Most of the above-mentioned cohort of nephews and godchildren is now reaching adulthood. They are not (nor should they be!) in the business of drinking wine that is now worth more than $150 per bottle. Most are looking to go travelling around the world before starting university and it is not unusual for ‘Uncle 🐿️’ to get a call asking if they can sell their wine to raise funds.

This was typically a friction free process until recently when my nephew Freddie emailed me to ask if he could sell his wine. I was aware that prices had been softening in fine wine markets since the end of last year, but it appears that, in the past couple of months, the market has gone ‘bid less’. Literally crickets.

Pricing of wine at the index level has seen depreciation of about 14% in the past 12 months. However, similar to the dispersion that we have seen in equity markets, there is a lot more going on ‘under the hood’.

Most of the major winer merchants now run online resale platforms for their collector clients. Selling Freddie’s Bordeaux would normally be a simple process of leaving an offer on the platform at a small discount to the guide price and waiting for a buyer to show up. Small problem. The bids have evaporated.

One of my favorite stories from Jack Schwager’s Market Wizards book series is the story of Bluecrest’s Michael Platt’s hiring practices for his family office:

"I look for the guy in London waking up at 7 a.m. to log into a poker site so he can pick off U.S. drunks coming home on Saturday night."

Most online wine platforms are often set up in a way that allows participants to submit unsolicited bids for wines that are held in bond on behalf of other clients of the platform. Historically when I have been emailed one of these bids, I am reminded of that Platt story. Some cursory research usually determines pretty quickly that these are stink bids, way below the current ‘market price’ and designed to pick off an inattentive collector.

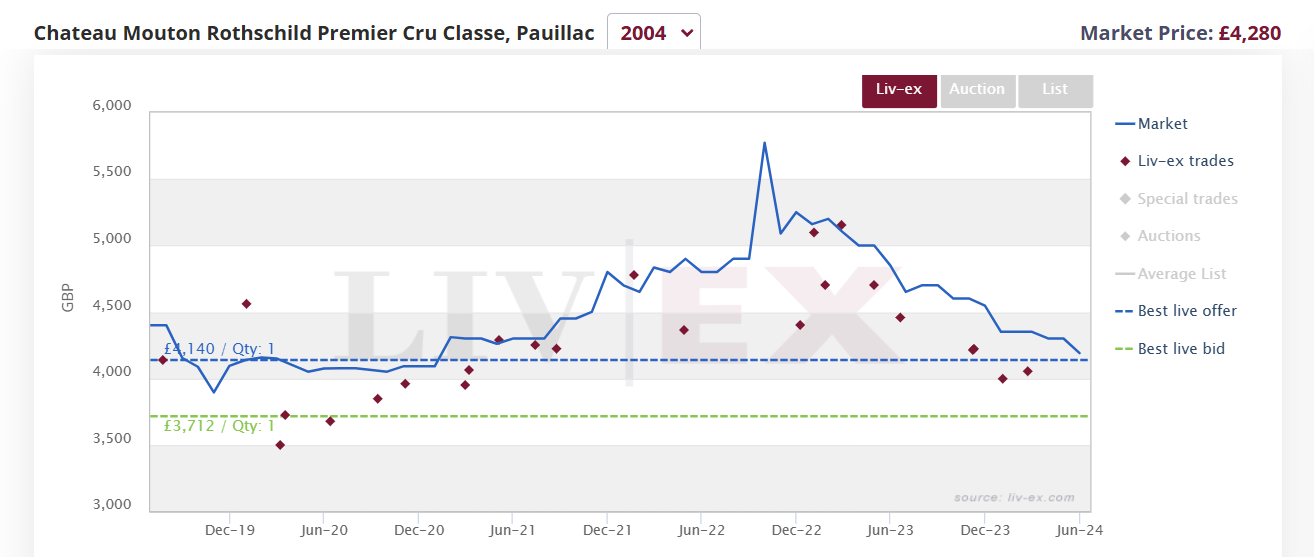

After several weeks of Freddie’s case of Bordeaux not finding a bidder, I decided to do some proper digging. The wine scores highly with the critics but it is certainly not among the big brand Bordeaux titans like Chateau Margaux or Mouton-Rothschild. Uncle 🐿️ is value investor! Nevertheless, the best bid for the wine is currently 15-20% below ‘market’.

In fact, for the claret elite the picture is even more bleak. The best bid for a case of 2004 Mouton Rothschild is well below 2019 pricing levels. It would appear that the bottom has truly dropped out of the fine wine market for the time being.

Interesting. Your curious rodent decided to have a sniff around elsewhere in the luxury collectibles market. Next stop, watches. The price chart of the secondhand Rolexes, a brand which has traditionally held its resale values very well, looks remarkably similar to that Burgundy chart above. I suspect that the real bid is also significantly below the line of that index.

According to BCG, “From August 2018 to January 2023, average prices in the secondhand market for top models from the three largest luxury brands—Rolex, Patek Philippe, and Audemars Piguet—rose at an annual rate of 20%”. Prices are now lower by almost 20% from the time of that report. A quick scan of the luxury watch auction sites confirmed my suspicion that a tradeable price for used Rolex is a full 15-20% lower than that. It feels that a seller would be lucky to obtain 2018 pricing levels on most models.

The 🐿️ is no fashionista but knows enough to know that Hermès’ (Jane) Birkin and (Grace) Kelly bags are the ultimate leatherware collectibles in the fashion world. Hermès’ long term strategy of extreme restriction of supply has kept secondhand Kelly and Birkin prices exceptionally firm. Until recently.

In 20 years, prices of luxury handbags have compounded at a lower rate than fine wine. At just over 4.5% of annual growth, this is lower than the 6.5% level of annual price increase set by the Hermès atelier. At the very top end of luxury, it would appear that brands with a strategy of extreme scarcity are the ones winning the day. The resale market for their products is almost irrelevant when they can retain their margins and some acceptable growth with this approach.

The legendary Ferrari falls into very a similar camp. Ferrari, as we have discussed before, is the only global auto company that has managed to break out of the valuation straitjacket that hampered the shares of other OEMs. The story, like Hermès, is one of restricted supply.

Limited production ensures that most vehicles are mostly purchased by those who ‘do not need to ask the price’. The less well (financially) endowed will have to content themselves with key rings and branded sneakers. We read last week that Ferrari’s first pure EV passenger vehicle will come with a $500k sticker price. This 🐿️ is pretty sure that the waiting list will be more than long enough to cover the planned production run.

But how has all of this consumer behavior impacted stocks, and what is the read across into the real economy?