Who Buys All that IPO Paper?

The 🐿️'s 'Start the Week' note! Elon and 'Scam' have a lot of stock to sell and they are getting the rules changed. Plus our weekly review of BUSHY™ and live Acorn trade ideas. 2026, Week 8.

In case you missed it, the weekend note grappled with a key ‘battleground stock’ in the current SaaSacre™ - Adobe. The 🐿️ probably managed to upset everyone! Check it out.

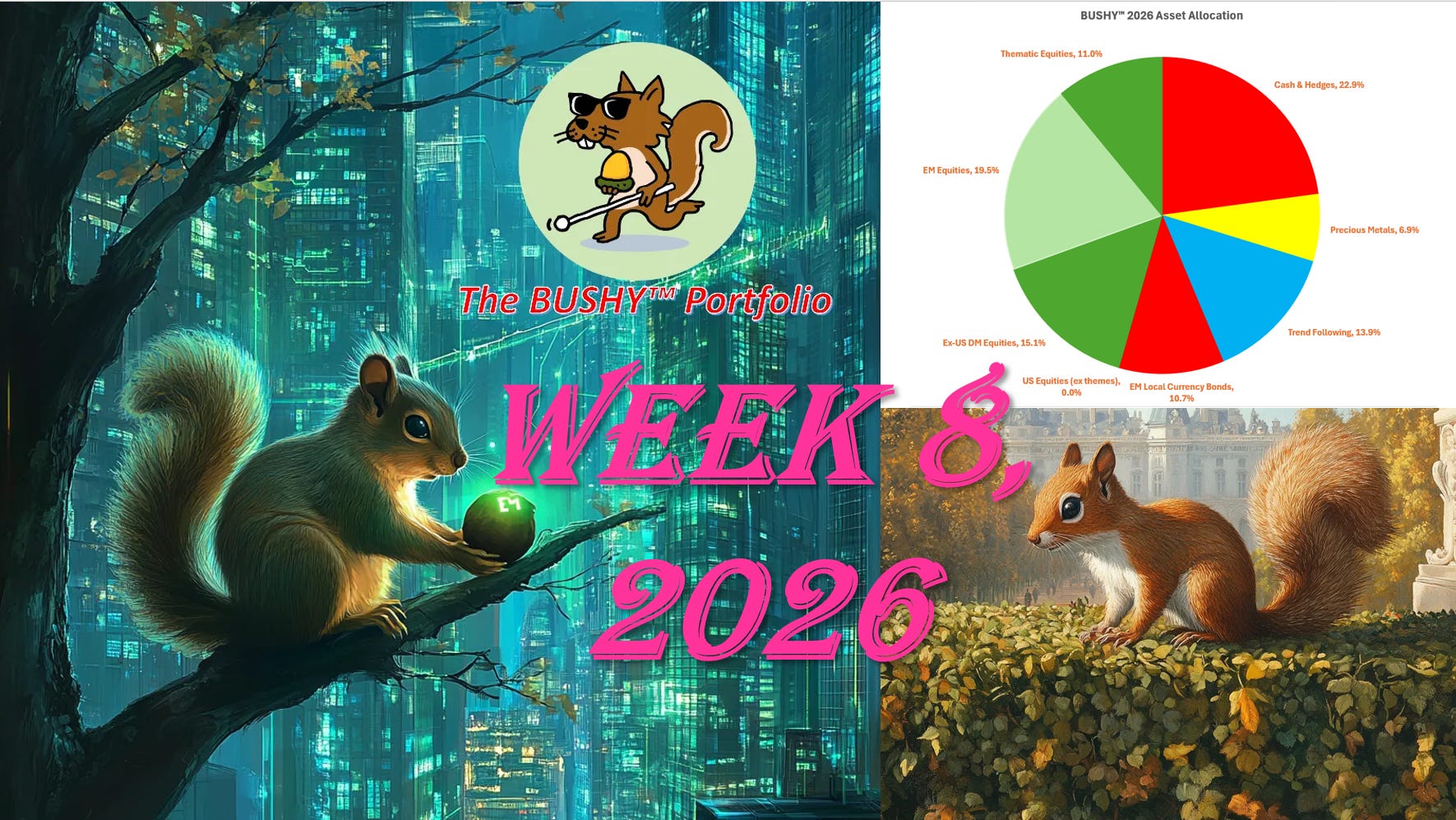

The BUSHY™ beta portfolio closed the month +11.95%1 on the year. I am going to refrain from making any commentary on the weekend activity in Iran or guess as to the likely impact on the portfolio.

We have plenty of energy and gold exposure at the moment. We are also very defensively positioned currently, with a high cash balance and plenty of hedges. More on that later.

In Benny and my conversation with Louis Vincent Gave a couple of weeks ago, we discussed how equity supply (in the form of ECM placements and IPOs) was typically the reason that bull markets in Chinese equities come to an end. Bankers get blamed for everything these days…

A surge of IPO activity in the US is typically a signal that we are getting close to a local top in markets. 2021 worked a treat on that front. However, this is more of a sentiment signal than a law of physics.

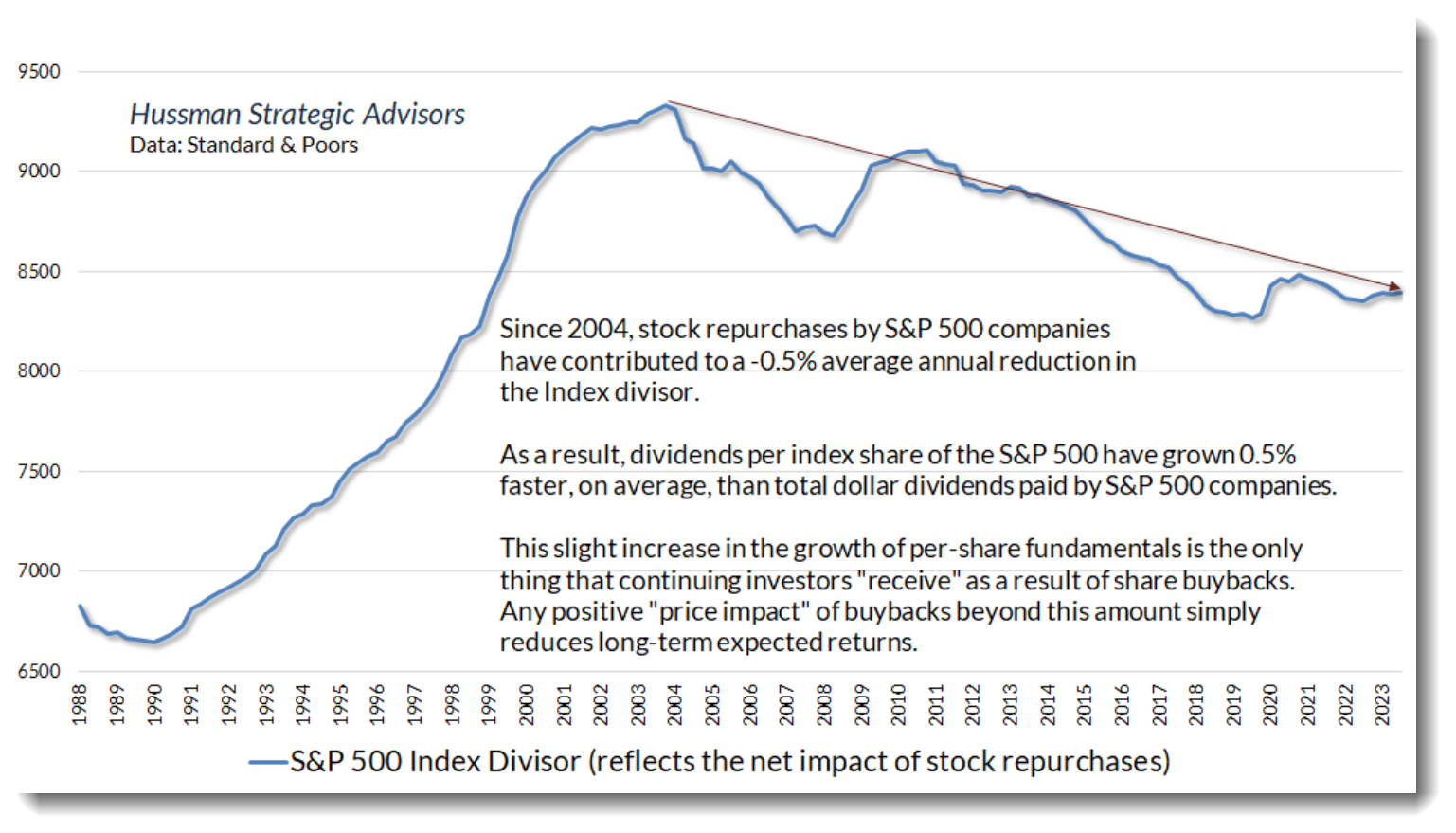

The reason for this is that the impact of share buybacks and companies being taken private (corporate and PW M&A) reduces the supply of equity by a much greater number than can be replenished by bunch of ECM bankers in New York.

I think that is all about to switch in to reverse gear.

In the weekend note on Adobe we touched on the fact that a great deal of buyback activity in the SaaS sector was necessary to ‘sterilize’ the dilution resulting from large scale issuance of stock-based compensation (a traditional 🐿️ pet peeve).

Traditionally, buybacks overall remove a large chunk of stock supply from the market every single quarter once those blackout periods close.

Block’s announcement last week that they will be firing 40% of their employees has implications for share supply. Yes, fewer shares will be issued as SBC in the future but I would hazard that (i) this will not be the last of this type of restructuring; and (ii) the volume of shares from departing employees (from Block and elsewhere) hitting the market to pay back student loans, mortgages and school fees is about to rise sharply.

Of course, ‘white collar’ job losses also slow the pace of 401(k) savings hitting those index funds every month.

Plenty of ink has been spilled on the topic of AI data center capex by the hyper-scalers. In addition to crowding out credit markets to fund this spend, budgets for share buybacks will have to be shrunk aggressively.

On a related matter, and with what seems to be impeccably poor timing, those NY ECM bankers are lining up one of the largest cohorts of jumbo IPOs seen in history.

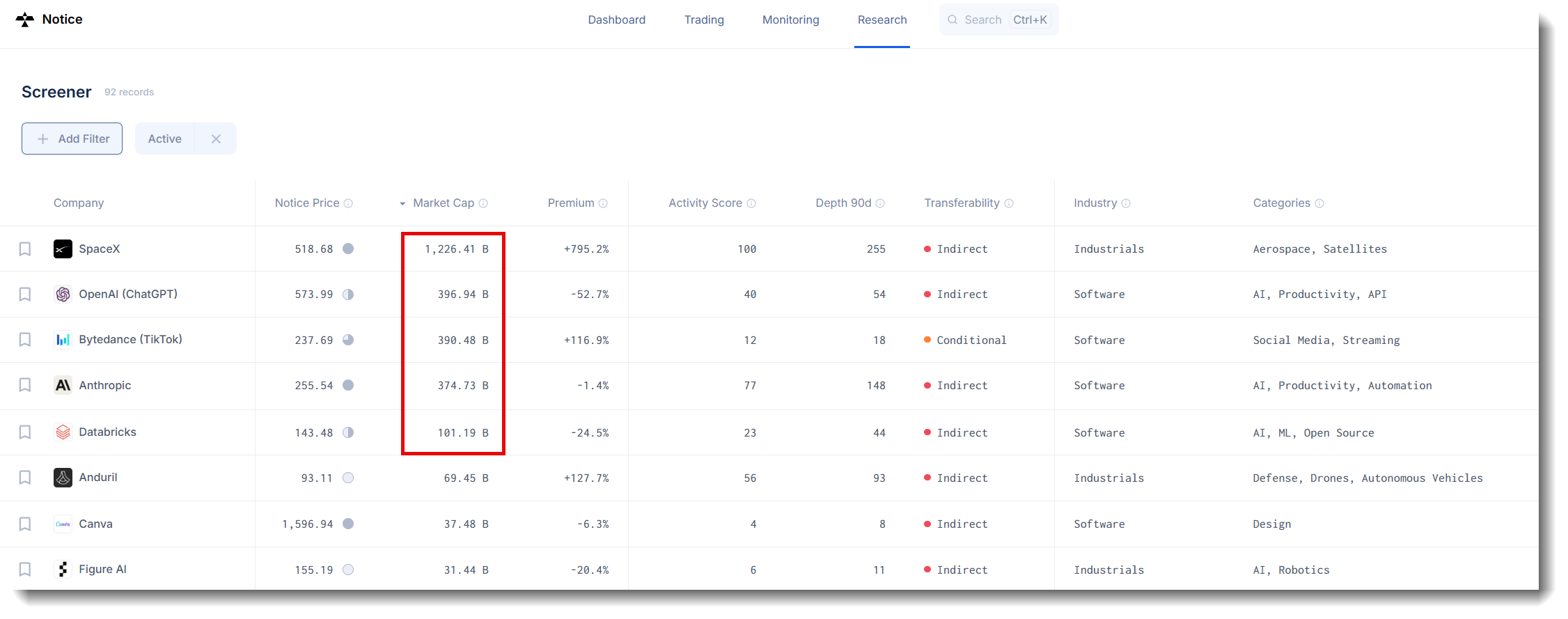

By the way, if you want a framework for how to value the space part of SpaceX (xAI is probably a liability!), I had a go in October 2024 (when the insatiably bullish Adam Jonas was estimating the entire space revenue TAM at $1 trillion by 2030):

Even if SpaceX only floats 5% of its equity at Elon Musk’s bogey / fantasy / ‘whatevs’ valuation of $1.5 trillion (only 150% of 2030 space revenue TAM!), that $75 billion deal will be 3 times the size of the Saudi Aramco IPO in 2019 that required the significant support of pretty much every sovereign wealth fund on the planet (as well as some significant ‘national service’ by local princes in Saudi) to get over the line.

SpaceX / Anthropic / Open AI and their advisers are clearly already sweating about sources of demand for all that paper. And they are pulling strings. The Nasdaq 100 index committee recently issued a consultation document proposing rule changes that would get these deals fast-tracked (with generous treatment around free float inclusion factors) for these jumbo new arrivals.

This would effectively allow these companies to sell vast quantities of unseasoned shares directly to the passive owners of the $400bn QQQ 0.00%↑ and any ETF or structured product (a lot!) benchmarked to the Nasdaq 100 index.

Thanks again to “Captain Passive” himself, Michael W. Green, for highlighting the issue last week just in time for me to be able to comment ahead of the 27th February deadline. You can find a copy of my letter via the linked tweet below.

I stirred up a few former ECM luminaries to do the same including Jim Miller who took Amazon public almost 30 years ago. A great story that he shared with me last May.

And my pal Craig Coben with whom I picked apart the impending Coreweave IPO a year ago.

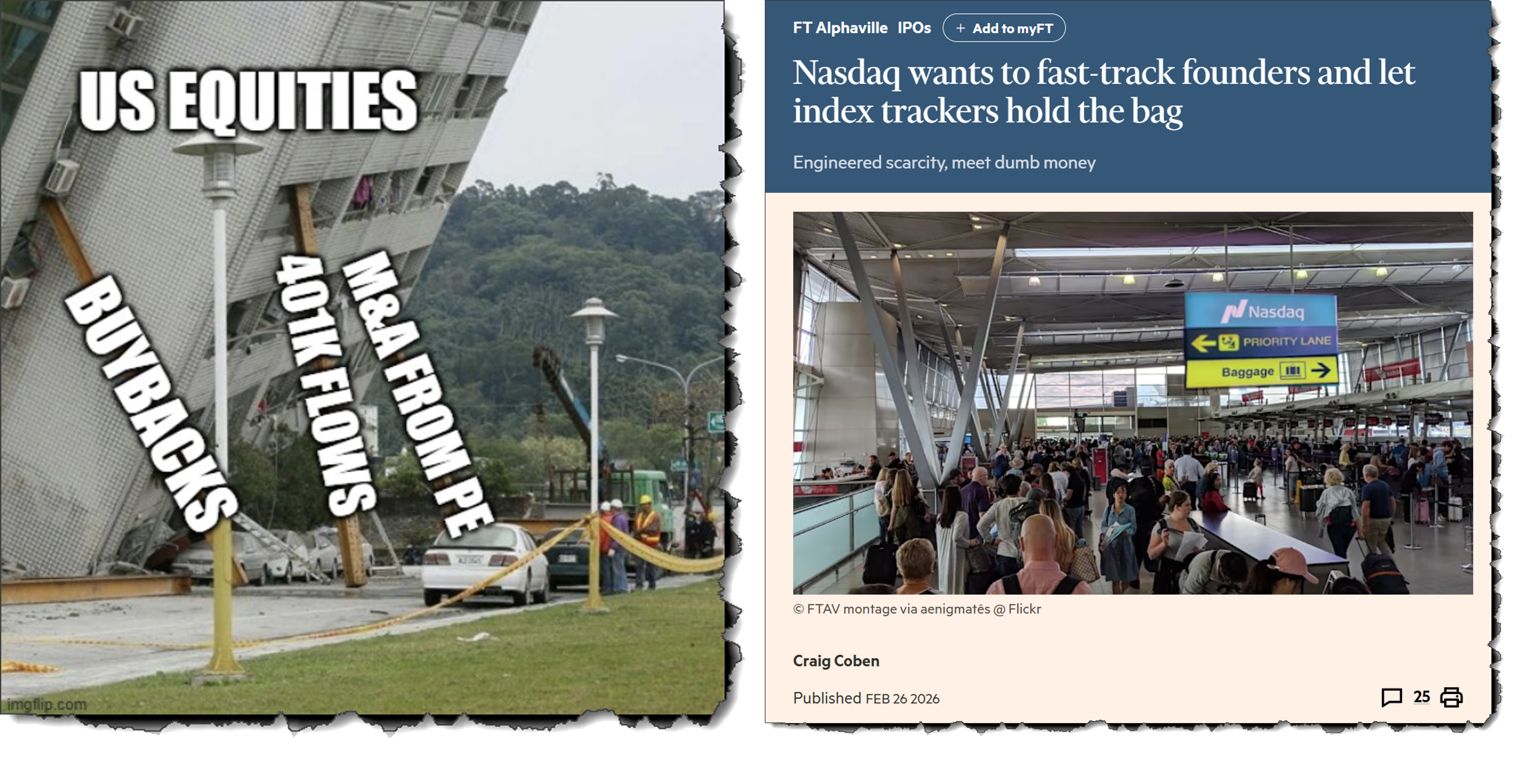

Craig went one better than my letter and penned this excellent column for the Financial Times. Flex! It is an FT Alphaville piece so free to read for non FT subscribers (link via image below).

Craig makes a couple of brilliant points that I did not cover in my letter. The FT’s picture editor deserves the picture editor equivalent of an Oscar for that cover image!

Retired senior bankers ranting about fairness in markets is one thing. Let’s get back to the physics. Assuming even just a handful of these jumbo gets out, US markets have never been tested with such extreme supply.

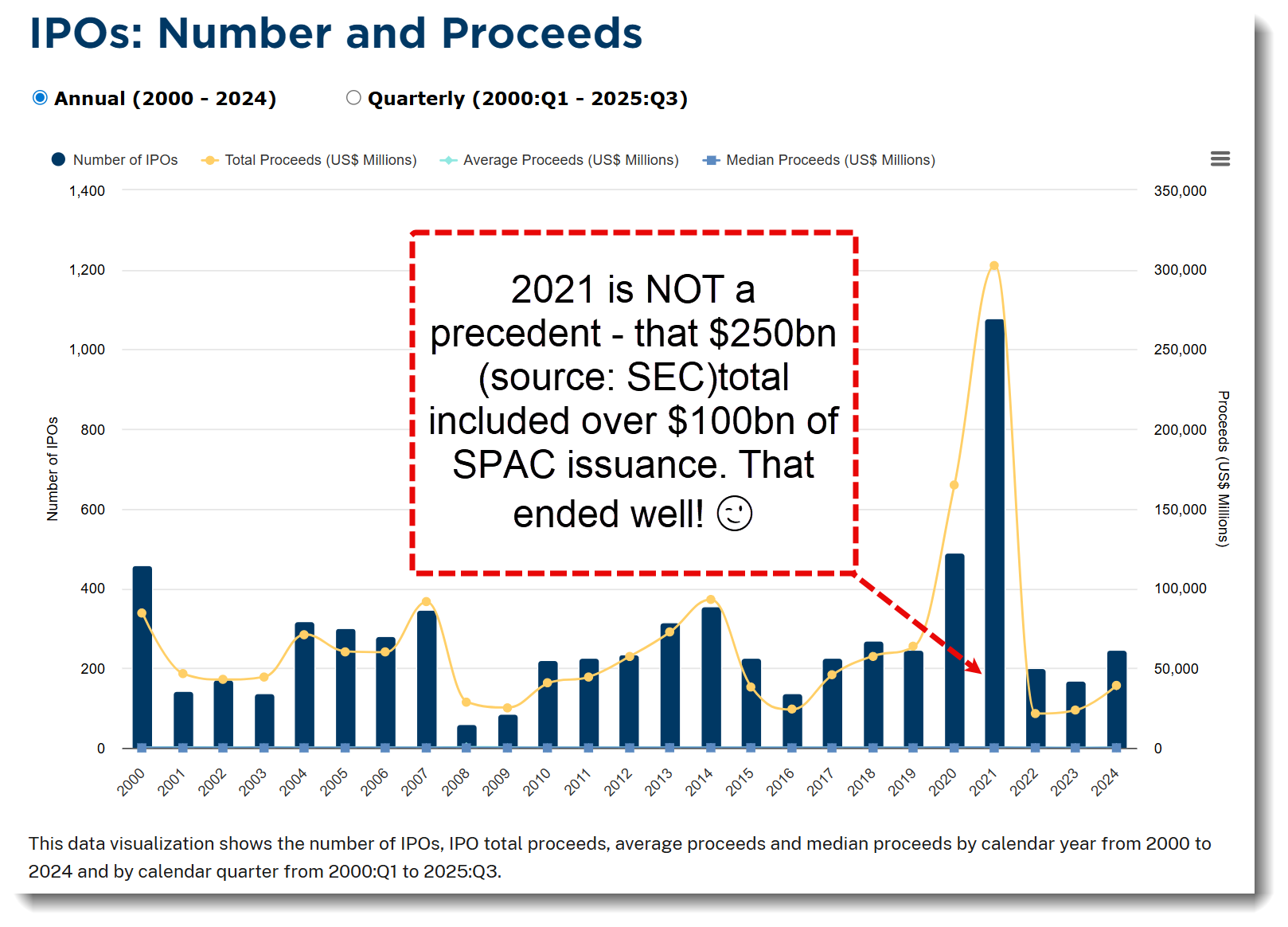

An average large year for US IPOs of operating companies (ignore the SPACs and funds) is $50-60 billion of proceeds (apart from that brief moment of lunacy in 2021 when the ‘wisdom of the crowd’ dictated that Rivian was worth $100 billion - fully diluted market cap post its day 1 ‘pop’).

Stuffing the passive funds (via deal focused hedge funds warehousing allocations) will help those ECM Syndicate but I am not sure that it is going enough. The full suite of retail brokers will be lined up to help. Your phones will be peppered with texts from Robinhood, SoFi et al offering “exclusive” access to IPO stock.

I am old enough to remember when it was considered ludicrously irresponsible to put more than 5% of available shares in a US IPO down retail channels. Heigh ho.

Most of my smart readers will either studiously avoid those texts from Robinhood or play the ‘flip to passive’ trade. Word of warning - if everyone thinks there is an arbitrage, that arb tends to close fast!

More worrying for me is that these deals are launching just as the de-equitization props of share buybacks, 401(k) inflows and M&A bids from cashed-up PE funds are being removed from the market (they cannot raise funds after torching too much capital on SaaS LBOs).

The rodent would contend that the result of dropping $75 billion of SpaceX paper (plus the rest from OpenAI, Anthropic etc. etc.) at a concept valuation on top of that building above could have some fairly unpleasant consequences. What’s more none of those newly public companies are buying back stock any time soon.

Another reason to favour ex-US equity allocations. Go where the paper is in shorter supply! Not rocket science (sorry).

BUSHY™ and Acorn Review

Back to regular scheduling. Last week was kind on BUSHY™ but we brace for how markets to react to weekend’s Iran news when they open on Monday.