Adobe: SaaSacre™ Victim or Don Draper's Nightmare?

The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 8 of 2026.

I am going to publish this 12 hours early. It was finished ahead of time and events in Iran have meant that you are all glued to your devices anyway. I hope this is a welcome change of topic from war in the Middle East.

I have also recorded the podcast early. Subscribers can access that now on browsers and the Substack app. Will be on Apple, Spotify etc. on Monday.

The header of every email you get from the 🐿️ encourages you to read BSM reports in a browser (for your maximum table and chart viewing pleasure). I can tell from the click through rates that most of you continue to stubbornly squint at your smartphones or tablets. Your call!

I doubt that very many of you print off my reports to read either. Sensible. A regular graphics-packed 2,500-3,000 word 🐿️ report would probably churn through 25 pages of your A4. In my pre-Substack days, I would write all reports in Word, formatting them to ensure that charts sat next to corresponding text and that tables would not break across a page leaving them divorced from explanatory headers. I would then create a PDF and email it out.

These days, I write directly into Substack’s editing software. I have looked many times into finding an “intelligent” HTML to PDF converter. I would love to add a PDF version of the note for subscribers. Nope! Apparently “intelligent formatting” is very hard. Surely if we were remotely close to AGI, this would not be rocket science!1

My PC pops up an invitation from Adobe to upgrade to the AI features of Acrobat Pro several times a day. Beyond irritating and classic monopolist behavior. Until Adobe fix this HTML to PDF challenge, I have no intention of paying them a cent for Acrobat Pro! (I do pay for other Adobe products)

It seems inevitable that the current meltdown in software stocks is going to throw out a few ‘babies with the bathwater’. My focus in late January - Refining the SaaS Long Short Opportunity - was more on avoiding dangerous shorts rather than identifying over-sold AI ‘winners’.

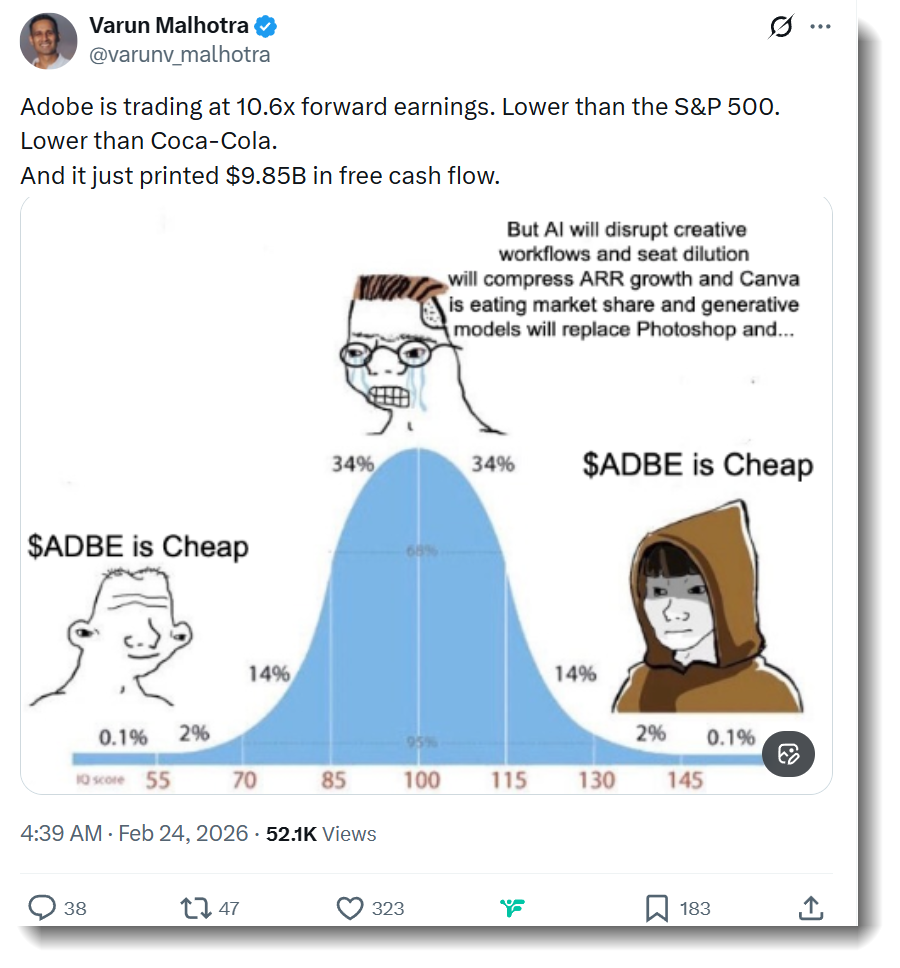

The other day, one of my members in The Drey asked, “what do people think about Adobe here? The stock seems to provoke as much passion as Bitcoin.” Adobe is a key ‘battleground stock’ in the ‘who thrives, who survives?’ AI / SaaS debate. It was not the first time I had had the question in recent weeks.

My ‘knee jerk’ response on Discord is below (link to full debate here):

“I have so many issues with ADBE. First and foremost it probably is the most invasive piece of software in terms of pop-ups shilling for subscriptions to Acrobat Pro on my PC. I pay for Premier Pro for video editing. I get that Photoshop is very sticky for design world but how big is that TAM? AI must have made it smaller. They kind of missed the boat on the whole DocuSign legal doc management game which also feels like a massive ‘own goal’. They should have OWNED that space yet I find myself asking professional services folk if I can ‘DocuSign’ (rather than print and scan) something every day. What is the path to a real return to growth? Consensus analyst estimates look like they want to ‘catch down’. Could certainly see it trade to a single digit PE. Almost 11% buyback yield in the past 12 months is not making a difference.”

As much passion as Bitcoin? That is 🐿️ bait! Then there is always a (borderline financially illiterate) tweet. They are the social media equivalent of catnip for this rodent.

A software-engineer-turned-Warren-Buffett citing comedy-adjusted (non-GAAP) valuation metric comparisons with a staples company. The 🐿️ decided that it was my moral obligation to defend the ‘mid-wit’ view. I think it was the Canva reference that did it for me. I have form when it comes to the Surry Hills unicorn👇

Adobe is a flagrant SBC offender. Fan boys champion the massive earnings properties of a ‘people business’ that somehow fails to acknowledge that the majority of ‘people’ cost is a (GAAP) income statement expense. More on that later. It was time for me to do some real work and pick my side.

A Value 🐿️’s Dilemma

Here in The Drey our favored stomping ground is cheap assets in unloved international markets and structural commodity deficits. Recently, the ‘SaaSacre’ (hat tip to Benny for that one - an improvement on ‘SaaSpocalypse’ I feel) has been a focus of our Acorn short book.

But with the market now pricing Adobe - a global software monopoly with nearly 90% gross margins - like a declining industrial ‘melting ice cube’ it behooves this rodent to pull up a few manhole covers and investigate.

Hearing out the AI Doomers

Adobe’s rap sheet reads as follows: