Revenge of the Malthusians

Why the Hormuz crisis is about to break global grain (and activewear!) markets and what to do about it. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 10 of 2026.

There is no paywall on this week’s edition. Please feel free to share liberally with friends and colleagues. If you are interested in getting more 🐿️ - get in touch with me for a trial.

Revenge of the Malthusians

Here at Blind Squirrel Macro, the 🐿️ is always on the lookout for opportunities for personal growth. This rodent is also firmly on ‘Team Expertise’. The other day - when we introduced ShinyAcorns™ (our curated gold miner basket) - I confessed that there were a couple of exceptions:

“…as with biotech, I have always tended to outsource my investing in the mining sector to specialists in the field. The 🐿️ is not a geologist and would not know one end of a drug lab from the other. Somehow, not being a meteorologist does not prevent me from regularly losing money trading natural gas and agricultural commodities. A personal growth opportunity?”

Let me explain. Until the summer of 2020 I had never traded an agricultural commodity futures contract in my life. I was then unfortunate enough to catch a monster bull run in corn and soybean prices. Early fortune bred over-confidence. Catching the 2022 Russia / Ukraine squeeze in grains did not help on that front either. A complete and utter monster was created - Farmer Squirrel!

I have been guilty of bleeding P&L way too often in the pursuit of “the next dust bowl”, “failed Safrinha crops”, “Gleissberg Cycle”, “La Nina Modoki”, “the USDA are jUsT wRoNG on yields!” and “winter wheat kill” trades over the past 4 years. Fortunately (from an overall portfolio perspective), the trend-following CTAs I invest in were typically on ‘the other side’ of every one of those trades.

False confidence driven by early luck is a well-established problem for traders and investors. So much so that I have resisted the urge to publish a note on grain prices since 2023 (writing about grain traders like Bunge and ADM does not count!). Until now.

But wait! Before you delete this email, this time I have back up! Let me introduce you to Nico - my pal and collaborator on this note.

Nico x 🐿️ collab!

Nico Hoyt brings decades of global trading experience, from clerking in the CME pits to managing capital for family offices and directing institutional grain operations for one of the ABCDs. An American now based in Uruguay, Nico founded ArchaiQ, an end-to-end sovereign tech stack specifically for Ag traders. He is also about to launch PAiQ, a JV with PiQ, a new Ag news and analytics platform.

Indeed, ‘Farmer Squirrel’ has some proper air cover this time! Nico will also be the guest on Benny & The Squirrel this coming Thursday (remember that paid 🐿️ subscribers get access to the show’s ‘goodie bag’: detailed notes, copy of slide deck, audio only edition and other goodies like guest research notes).

This rodent celebrates the fact that the success of mechanized agriculture and the ‘Green Revolution’ put the Malthusians firmly back in their box.

The lifesaving role of synthetic fertilizer and AgTech dwarfs the roles of blood transfusion, vaccines and antibiotics in supporting the expanded population mankind on earth. I have covered this before:

Before we dive into this week’s fertilizer-adjacent theme a repeat PSA for paid subscribers: a lot is happening intra-week at the moment since acts of war no longer uniquely occur between Friday’s Globex close and the Sunday evening futures session.

I am updating members of The Drey in real time on portfolio changes - including time sensitive trade ideas such as the one I am covering this week. Nico and I are already in there debating strikes on September corn options!

Easy joining instructions (for paid subscribers only): 1. Hit the button below (which takes you to the The Drey’s waiting room on Discord); 2. Reply to this email or DM me with your Discord username / handle. Easy!

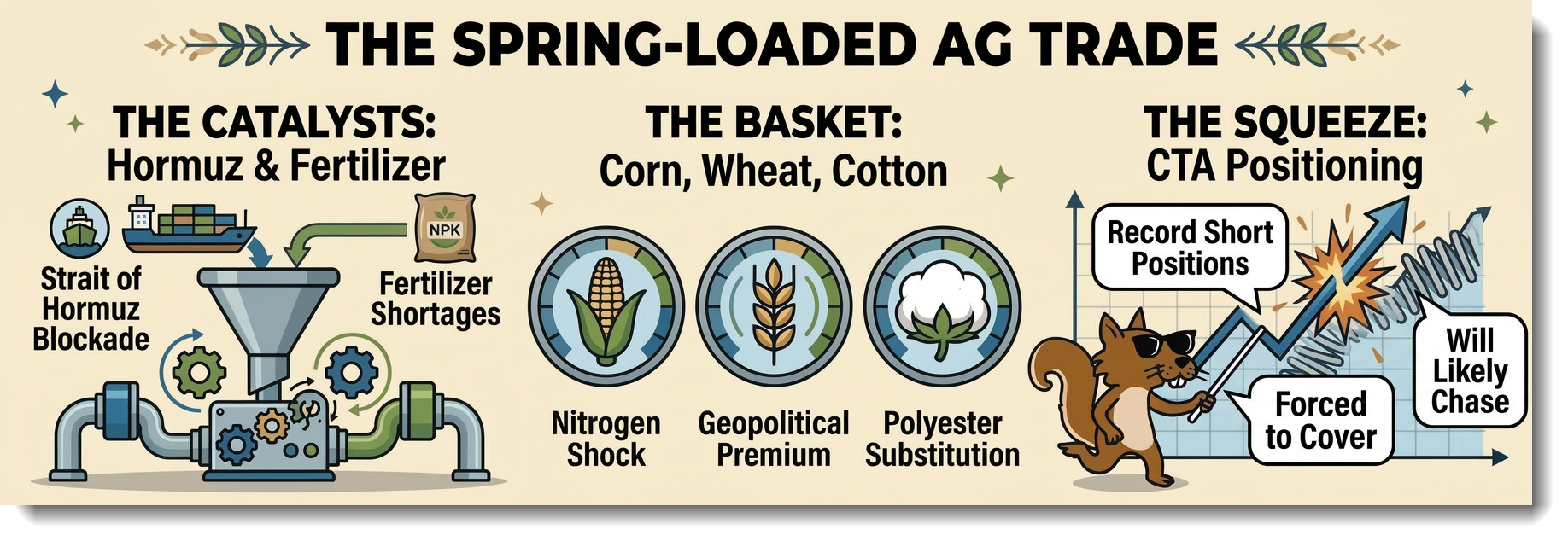

This week’s theme comes in 3 related parts:

Do Not Sleep on Corn

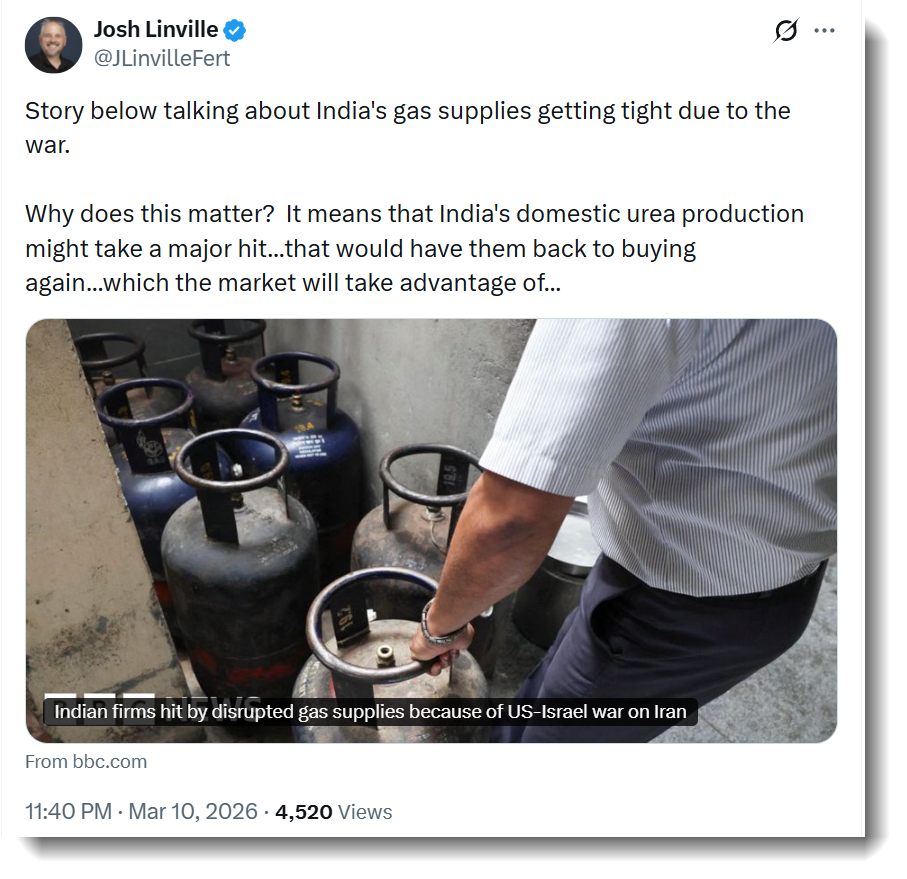

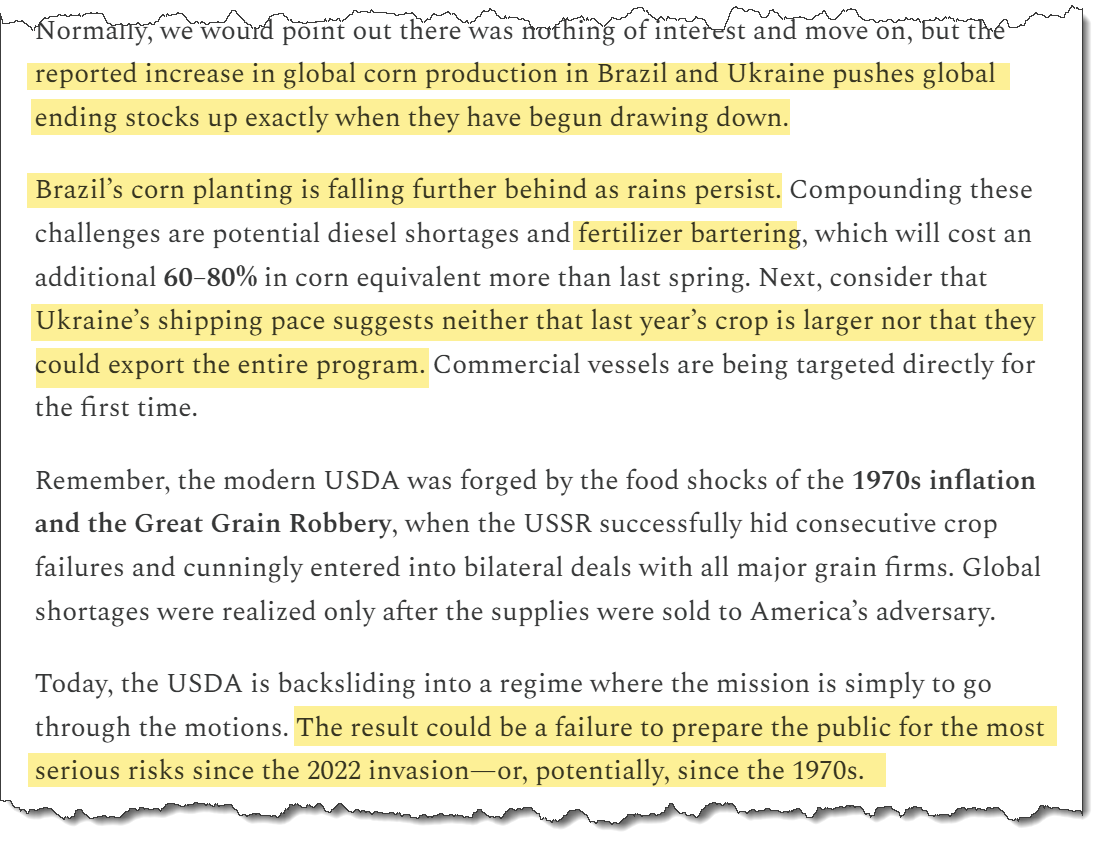

The effective closure of the Strait of Hormuz is in the process of kicking off a severe supply shock. The current conflict is choking off up to a third of the world's fertilizer trade. Given that nearly 50% of global urea and sulfur, as well as 20% of natural gas (feedstock for nitrogen fertilizers) rely on this route, the impact on pricing and availability is immediate.

Importers of nitrogen-based fertilizer in emerging markets face immediate shortages - Nico reports that producers in Brazil are already seeing barter costs surge by 60-80%. A diesel shortage - that could potentially trap ag crops inland - also looms. But the real impact will be felt down the line. Northern Hemisphere spring grain planting season is peak demand time for nitrogen fertilizers.

In Ukraine, severe February frosts in areas with poor snow cover created an estimated 5% national winter kill loss for the wheat crop. The standard farmer response would be to replant those damaged acres with corn. Frozen soil is already delaying this process but a fertilizer price and availability shock completely breaks the cost input math and may force complete abandonment of spring corn planting.

Globally, higher prices and supply shortages (there are no meaningful strategic reserves in fertilizers) mean that farmers will be forced to use less nutrient. Weaker crop yields this summer seem inevitable and marginal acreage will not get planted. Surprisingly, the USDA’s most recent (March) WASDE report did not appear fussed. Nico was not surprised.

Cue his post-match report:

The Case for Wheat

Wheat is the classic geopolitical risk premium trade. We have seen multiple false dawns in wheat markets in the past few years. Most have cost the 🐿️ money… I am of course at risk of “this time is different” accusations. However, the Black Sea yield loss and institutional complacency around wheat balances generally mirrors the 1970s grain shocks that Nico refers to above.

Wheat also faces similar fertilizer challenges even if in the back of my mind the wise words of the late, great Morris Sachs still ring. “Wheat grows if you piss on it” would come the prompt retort from him every time I ventured a bullish $ZW idea. He was invariably correct (one of his daughters is married to a Canadian arable farmer). RIP ‘Old Chestnut’ - I cannot believe it has been almost a year.

MB might disapprove - even if one of his early trading wins involved calls on wheat futures at the time of Chernobyl - but I do believe we have a rare set up here that justifies a small “wingy” position.

Your Activewear is Going to Get more Expensive!

Nico has been pounding the table on cotton valuation for a while. I have been listening but have fallen for cotton optimism a couple of times unsuccessfully in recent years. Cotton has been in a bear market since the unwind of the great cotton short squeeze (inflicted on the textile mills) of 2020 to 2022.

Brazil’s importance to global cotton balances has been accelerating since the mid-2010s. These days, estimating cotton yields in Texas plays second fiddle to eyeing rainfall estimates in Brazil, where cotton is now often favored over corn for second-crop (Safrinha) acreage in the Mato Grosso and Bahia provinces.

Nico reckons that wet weather in these regions may impact volumes - “It’s not problematic yet, but it’s not the ideal setup the USDA keeps reflecting as they hike production each report.”

However, up in Texas (and it’s not just there!) the risk of acreage loss (most likely in favor of soybeans) is significant - “the marginal cotton farmer may finally throw in the towel”. Nico reckons that U.S. cotton acreage is at risk of falling below that ‘sticker shock’ 9m acre threshold, the lowest in a decade. Marginal acres look more likely to favor soybeans or sorghum - last year’s crop was great and if China is buying, that (sorghum) will be preferred.

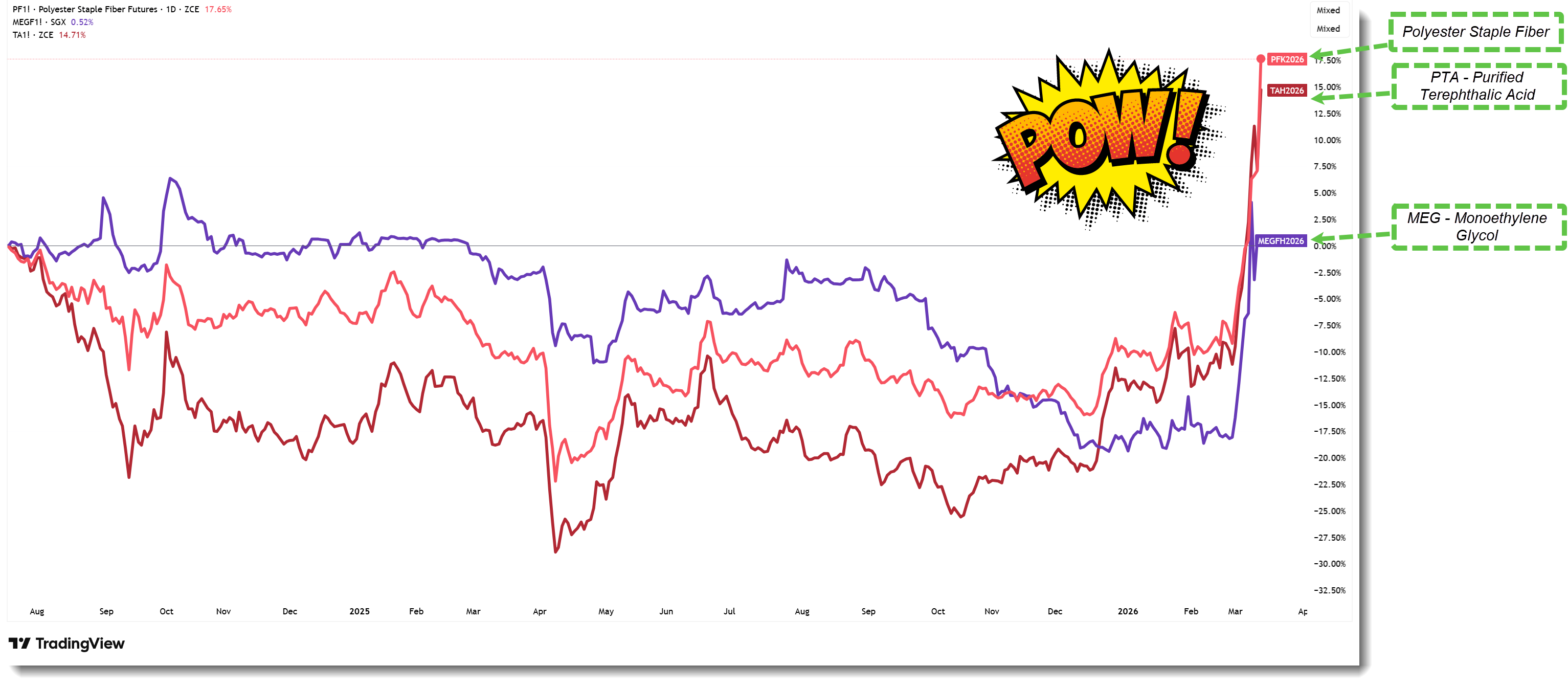

However, the Hormuz crisis creates some urgency around the opportunity. According to Nico, the “synthetic” share of our wardrobes is about 70% (polyester is 55% of global fiber production). That number is probably closer to 5% for this ‘Gen X’ 🐿️ but probably 98% for my ‘footie’-obsessed stepson.

As the Hormuz blockade severely restricts refinery feedstocks, prices for polyester and core inputs like PTA and MEG have climbed over 40% in a matter of days.

All of a sudden cotton starts to look competitively priced versus polyester just as cotton potentially comes into short supply. I grant that the Brazil situation is somewhat weather dependent (friends don’t let friends trade the weather). However, the US marginal acreage argument does feel solid.

The valid question to ask is whether higher polyester costs will be passed on to consumers (time to make a rushed bulk buy at Lululemon!) or whether we will see a switch over to cotton.

These days, cross-price elasticity between cotton and polyester is heavily restricted by modern consumer preferences (i.e. breathable / wicking activewear will not be replaced with cotton). However, the impact on cotton balances simply cannot be zero.

What Breaks The Cotton Thesis?

Brazil and China have exceptional crops.

China: Nico remains skeptical of cotton stocks in China. The USDA quietly hiked China’s production by 500,000 bales in this last report. Weather in Xinjiang, which produces 90% of China’s cotton, was average at best according to his AiQ model. Yet, this production figure is more than 10% above a year ago and 25% above two years ago.

Brazil: Rains are near a tipping point where total precipitation could flip from very good to way too much. The next few weeks will be critical. In an ideal year, cotton gets a lot of heat and timely rains. Brazil’s monsoonal rains continue to outperform, which is a bigger risk to corn planting than anything else.

A major recession is always the #1 risk.

Cotton trades with a multiplier to crude oil. If there is a large recession and crude sells off, cotton tends to overshoot to the downside. The demand aspect is far more elastic than other agricultural products (food is non-discretionary!).

If the world experiences a recession, people will be loath to pay more for fibers over synthetics. If you are already long a bunch of Brent call options you probably do not need to double up with cotton!

What to watch in the coming months: Brazil weather, China weather, early indications that USA acres are lower, USA export sales (specifically a pickup post the Trump-Xi summit), Australia’s El Niño status and indications of more direct payments to farmers.

Broader Portfolio Context

Before we go through the gameplan, a quick word on why this trade works in combination with the broader BUSHY™ and Acorn portfolios.

As mentioned earlier, the CTAs have spent most of the past 4 years short the grain complex (often fading Farmer Squirrel!). The downward trending weekly charts make it understandable why the trend-followers would be positioned that way. It does not look like I am fading the robots completely here.

There are some interesting observations to be made from the most recent Commitment of Traders data (lower panel of the charts above):

In corn, it looks like the CTAs are sniffing out a turn…

Large specs (blue) recently flipped long as the continuous contract broke above the 200-week SMA. The last time they did this in late 2024 / early 2025 they put on length very quickly. Small specs (green) are still short.

Among the 2 more Ag-focused CTAs that I own (and where I track the changes in position over time via dbmfwatch), KMLM 0.00%↑ remains short (c.6% of NAV) while CTA 0.00%↑ now has a small long (3.6% of NAV) having been flat or short for most of the past year.

Another smart observation on the corn curve from Nico - specs bought probably 250K contracts the last 8 sessions. Historically, that is a huge amount of buying, but it also suggests that farmers sold corn across the curve especially at the front. This implies that the December contract is ‘leading’, which indicates the market is not as comfortable with acreage estimates from the experts / USDA.

Some nervousness (from the shorts) in evidence in wheat?

Large specs (in aggregate) started the year with a significant short position in Chicago wheat but this has shrunk a lot since mid-February. Interestingly the specs have tended not to chase big wheat spikes of the past (they were almost indifferent to the price move following the Russian invasion of Ukraine in 2022 - but back then the grains were actually moving).

KMLM 0.00%↑ recently flipped (very) small long having had a 6.5% short position as recently as mid-February. Similar story at CTA 0.00%↑ which now has a near 3% long relative to a small short a month ago.

In cotton I see less sign of nervousness (yet still a touch)

Large specs (in aggregate) are short in a size consistent with most of the past 14-15 months. Small specs are long (but they have been long and wrong for most of the past year).

KMLM 0.00%↑ does not have a position but CTA 0.00%↑ has a small short position that has been reduced significantly in the past year.

This overall positioning leaves me with the impression that those quant crystal balls may be seeing a bit of what Nico and I are seeing. Based on the long term moving averages alone, I had expected them to be much shorter in the grain complex than they are.

While this means less potential ‘rocket fuel’ from short covering, there is a decent chance that the CTAs follow us in size (particularly in corn) if the trade starts to work in our favor.

The next thing in the back of my mind is the acorn position in WH Group (288.HK - Flying Pigs?). Higher grain prices is a margin killer for pork producers. The 2012 and 2022 corn rallies did major income statement damage. Declining feed costs is cited as a primary driver of (subsidiary) Smithfield's recently raised 2025/2026 guidance.

While I reduced the WH position as part of the recent portfolio de-grossing, it will be nice to have some corn length on the other side of this position.

How to play

We are going to make this very simple as the core idea will also be represented within BUSHY™. Nico and I will happily debate structured ideas in The Drey - for example, he has some interesting thoughts around the setup in September corn. Check it out - Nico has lifted the paywall.

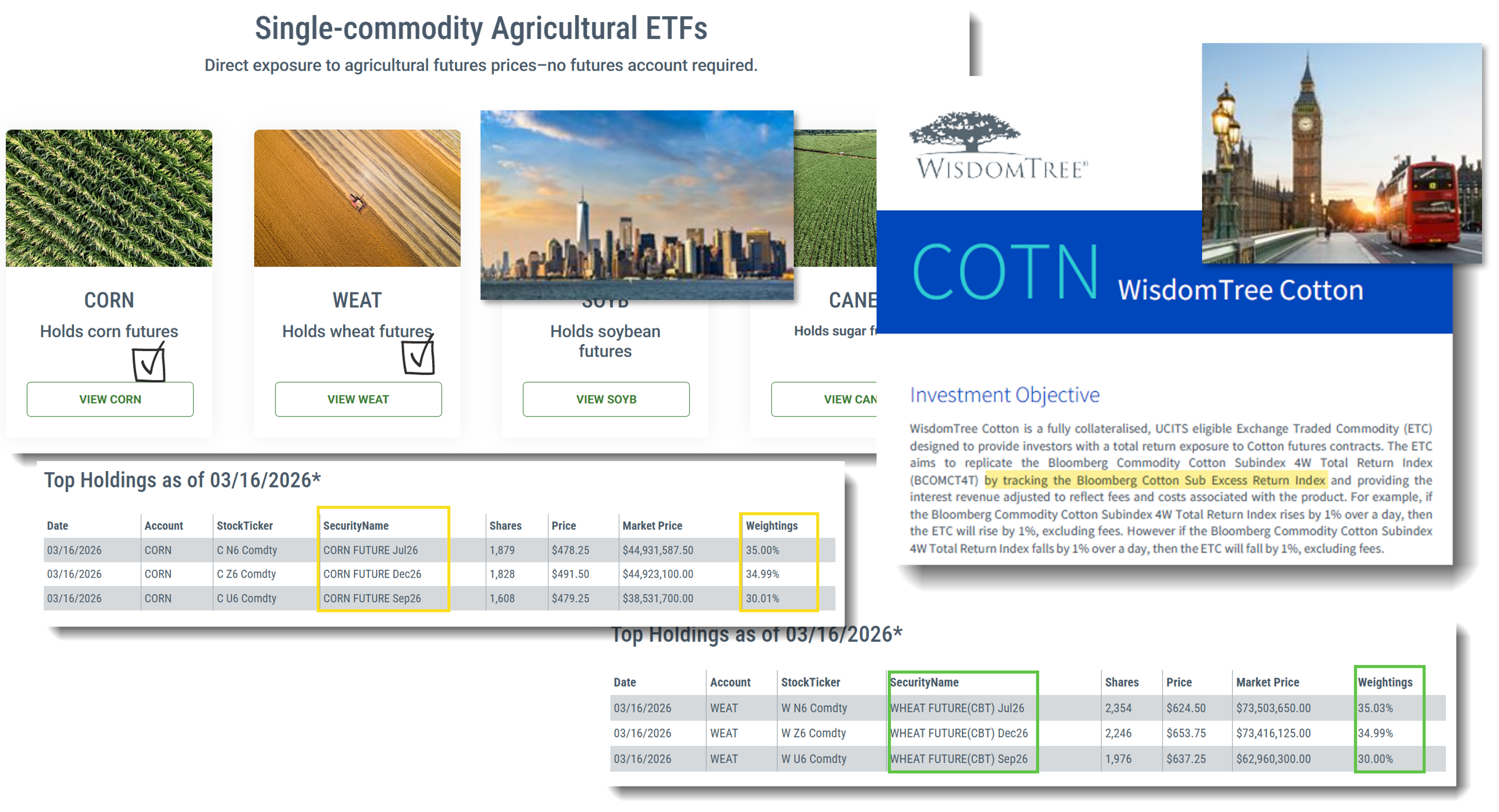

Long term 🐿️ readers will be familiar with the suite of single Ag-futures backed ETFs from Teucrium. They offer products for exposure to a blend of 3 futures contracts across the curve on both corn CORN 0.00%↑ and wheat WEAT 0.00%↑ (contract splits below).

Unfortunately, Barclays closed its US-listed ETN (“BAL”) in mid-2023. We also lost their cocoa ETN (“NIB”) just ahead of that epic bull run (often a sign - see also single country ETFs!). As such, for the cotton exposure, we will use COTN, WisdomTree’s London-listed ETN that rolls the front month CT (“Cotton No.2”) futures contract.

Some readers (especially US-based ones) will not be able to buy COTN and will need to get exposure via the futures directly (my pick would be the December 2026 CT contract).

I am going to put the splits, sizing and risk management plan (and BUSHY™ allocation) as well as futures alternatives for corn and wheat in tomorrow’s ‘Start the Week’ note for paid subscribers. Will also add some ‘fire and forget’ futures options ideas that have a bit more convexity.

Free subscribers can message me if they want to go on a trial via button below or by emailing acorn@blindsquirrelmacro.com.

or simply 👇:

As ever, please get in touch if you have any questions - via comments below, in The Drey or privately via DM.

Squirrel out!

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.

| A guest post by

|

Hurray for @nico and the 🐿️. Birds of the same feathers flock together.