The Monday Note:

The Visuals and Links:

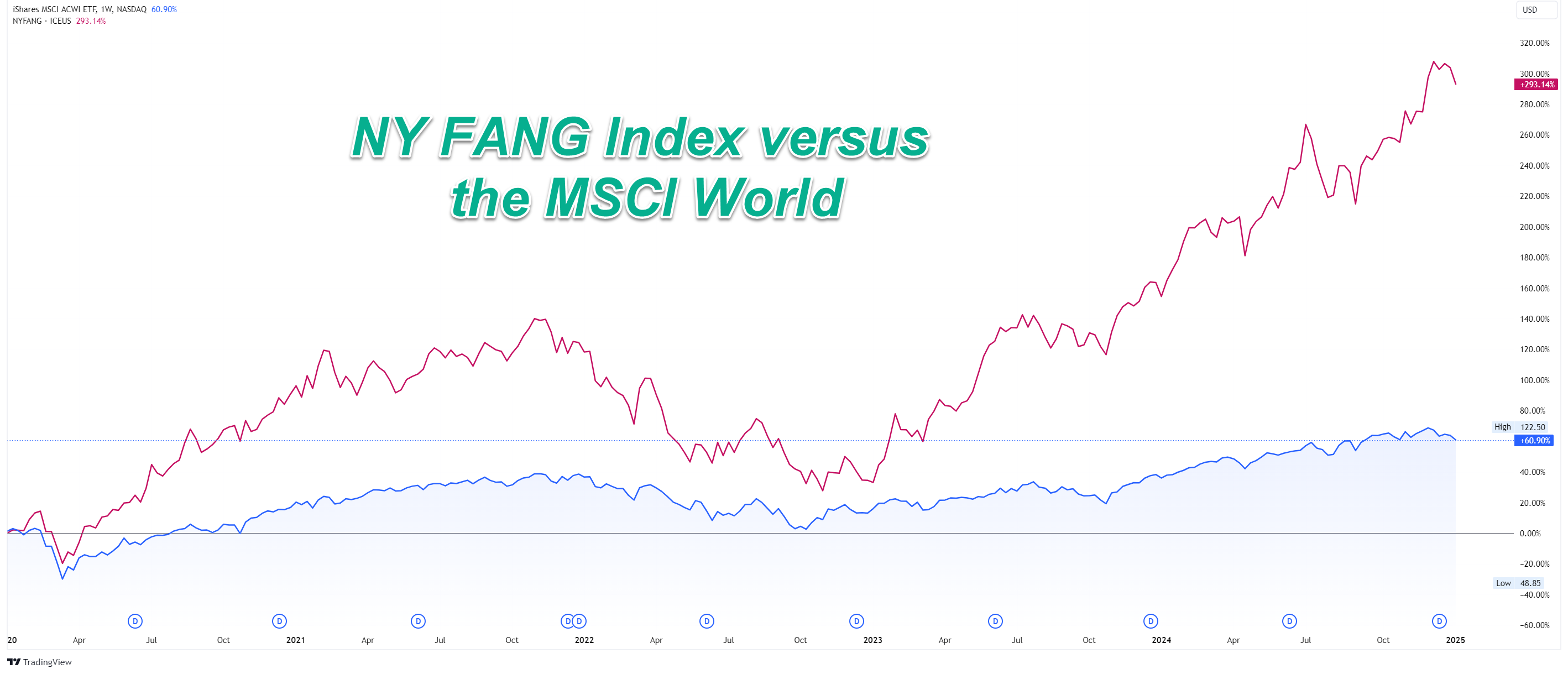

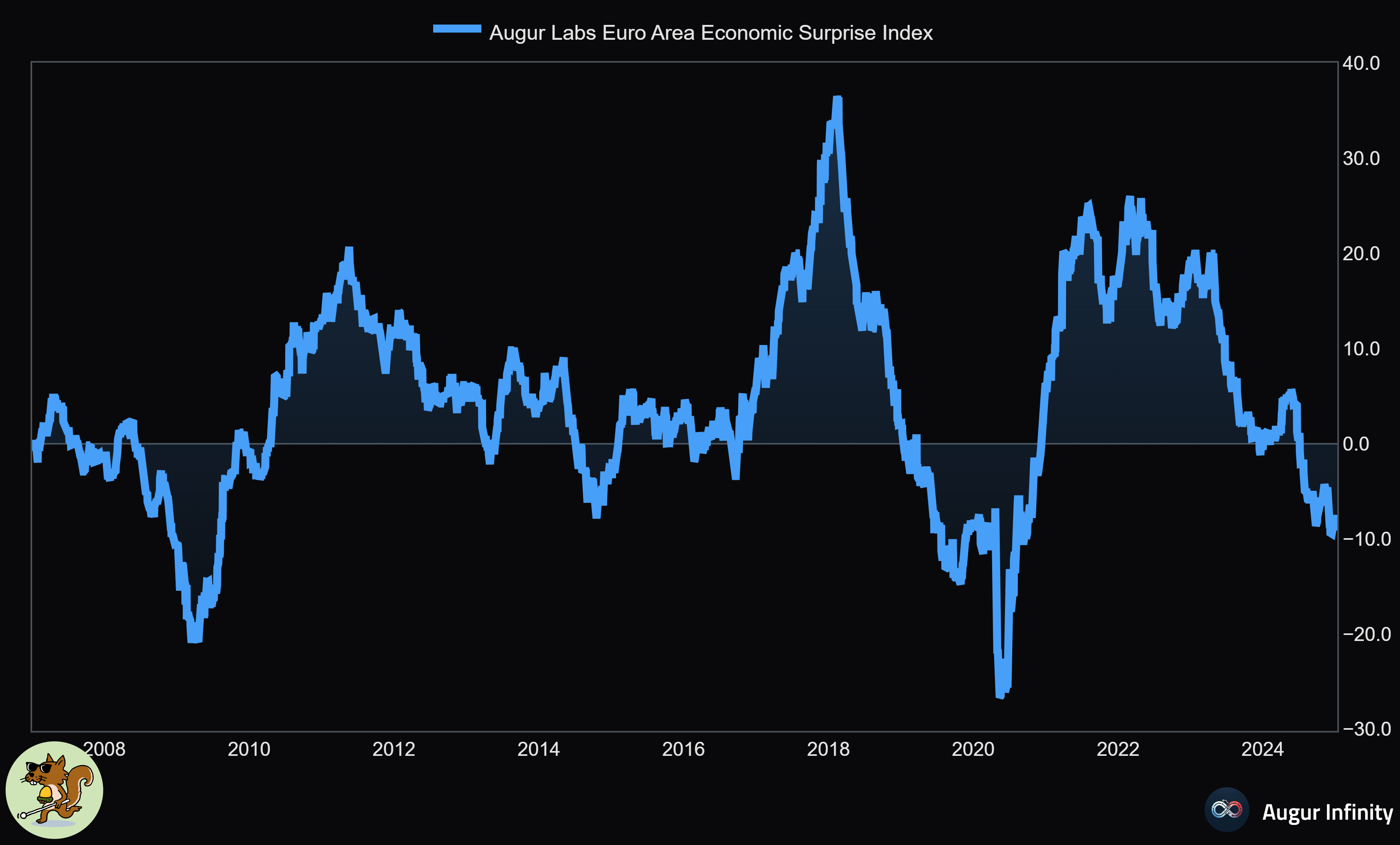

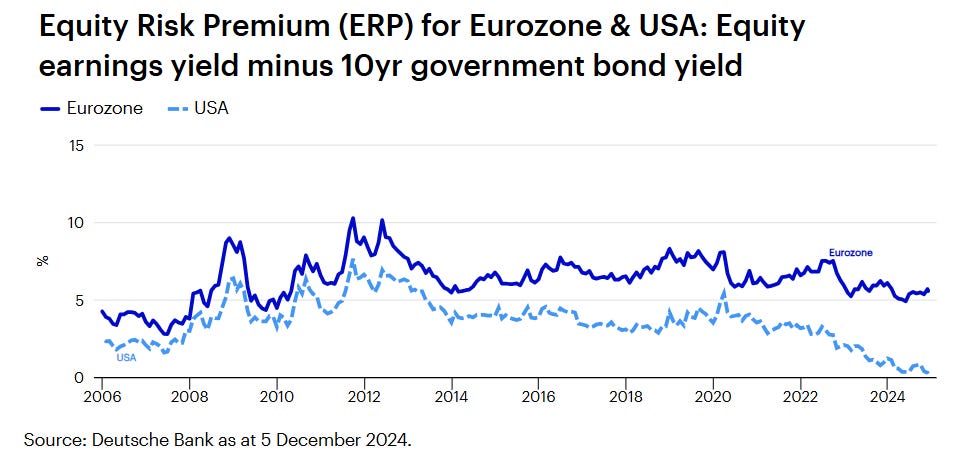

Let’s take a quick look at the charts:

Music from Max Slorach. Find him at:

email: maxonsaxentertainment@gmail.com / web: maxonsax.com.au

Thanks for listening!

Squirrel Out!

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.