It's 'Line in the Sand' time, Dario!

The 🐿️ is Calling Time on Cap-Weighted Dominance in US Equities. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 24 of 2026.

A very early edition of the ‘Monday Morning’ Notes this week. Lots to chew on for the extended holiday weekend.

Quick reminder that the cost of annual subscriptions will be rising from $360 to $450 at the end of this month. Monthly subscriptions will remain at $45. As ever, all existing subscribers are grandfathered at their original rates.

The idea behind this note has been swirling around in the back of the 🐿️’s mind for several months. It is now time to put some flesh on the bone - especially now that my pal Dario (Perkins of TS Lombard, not the Anthropic one) decided to dunk on my pet thesis! This is a bit more subtle (than a golden BMW 😉) mate, I promise.

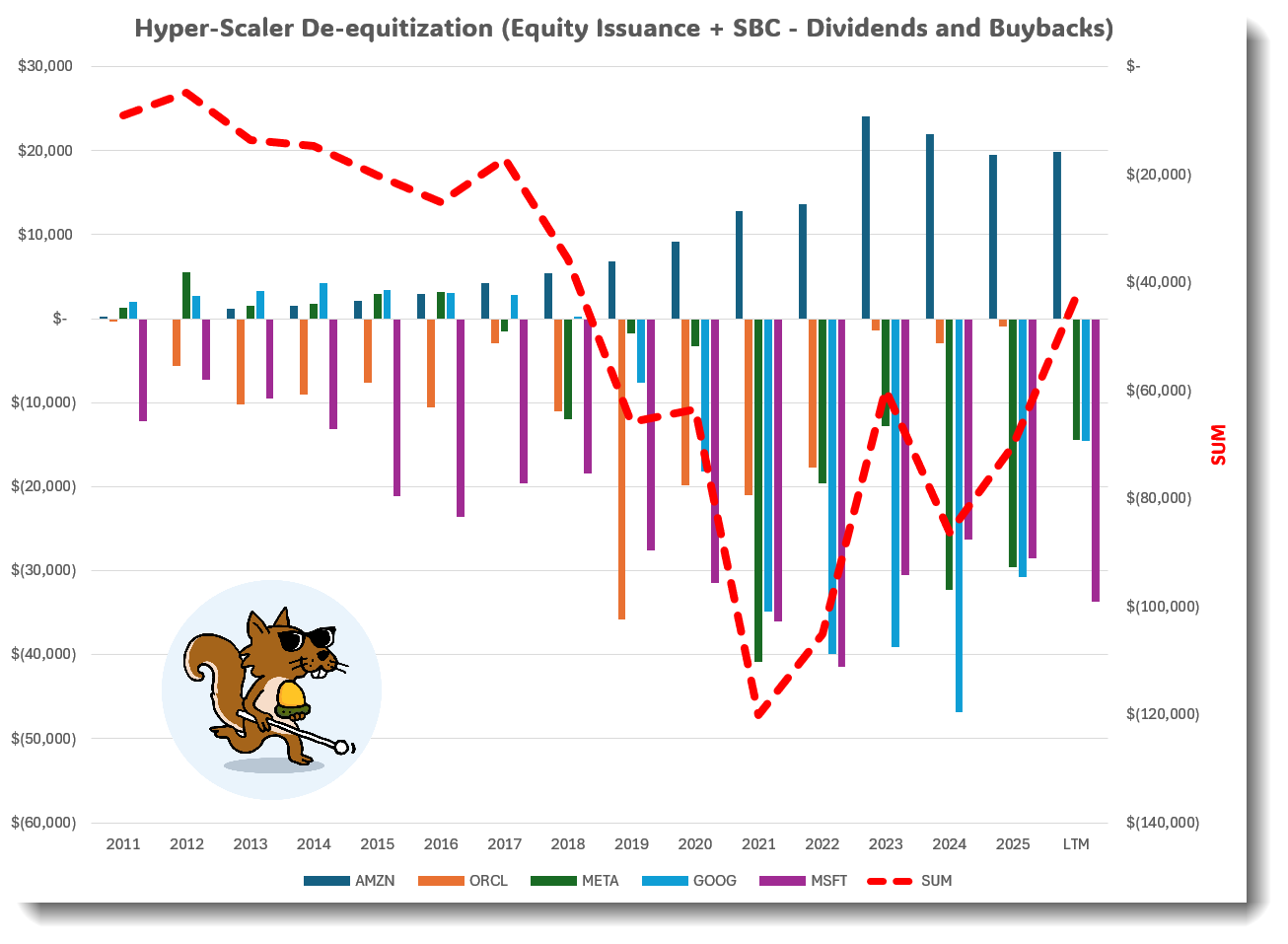

Flows matter in both directions. Equity buybacks are a discretionary contraction of free float that I believe to have been a dominant share price driver for the biggest issuers in the US equity market for over a decade.

These issuers have now chosen instead to spend the money on an AGI Holy Grail quest that risks slowing the 401k flows (as the machines eliminate white collar jobs) that have been another important supporting factor for the market.

Unlike bonds, equities carry no maturity date - there is no par value floor and no coupon schedule to anchor price. Furthermore, stocks do not benefit from the almost infinite low cost warehousing capacity (bank balance sheets, basis traders) that bonds enjoy. Supply matters so much more for stonks.

To recap, since early this year, I have been increasingly concerned that the tailwinds that have supported US equities in the past 15 years - namely share buybacks, LBOs and 401k flows - could be about to move into reverse just as the market has to handle a wall of AI-related IPO equity supply.

On this theme, Google’s recent equity raise may - with hindsight - mark an even more important turning point in structural trends in US equities than that headline-grabbing SpaceX IPO. That was the topic I really wanted to talk about the other day on CNBC.

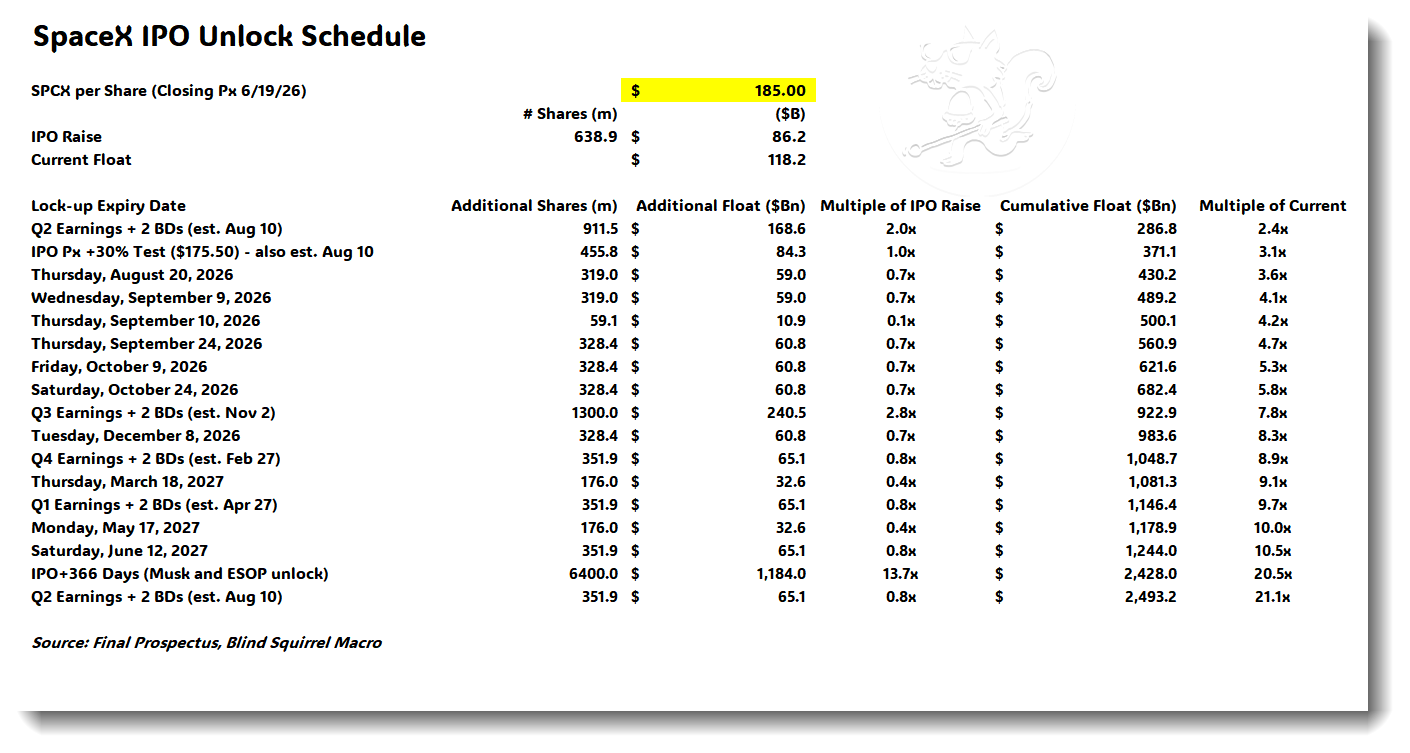

By the way, I am seeing an awful lot of bad math / failure to read the prospectus as relates to the SpaceX IPO shareholder unlock schedule. Let me spell this out. While the SPCX 0.00%↑ micro free float will be a plaything of degenerate gamblers and gamma traders in the near term, we are less than a quarter away from the SpaceX free float quadrupling. That float then doubles again by early November. See table below.

And this is just the secondary shares. At current rate of SPCX 0.00%↑ cash burn, how soon before the rocket ship / Enterprise AI / neocloud company has to come back to the market for primary equity?

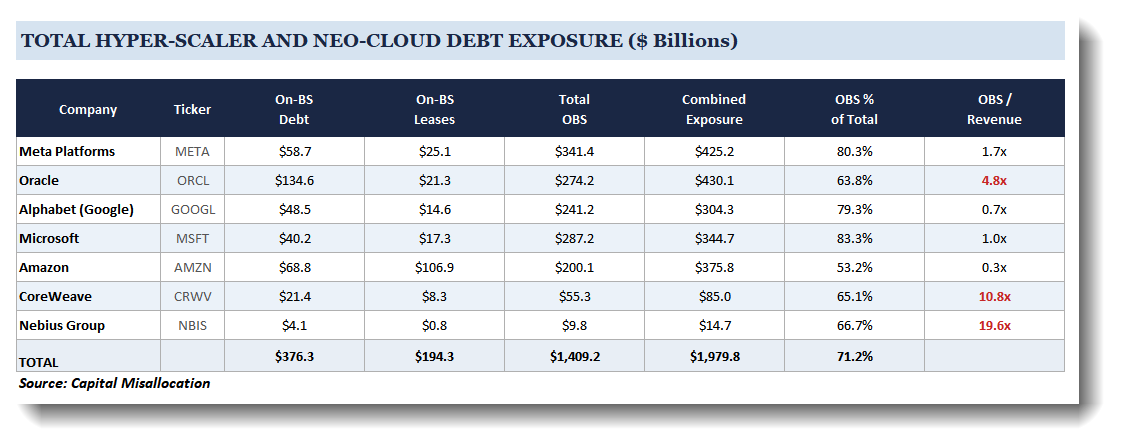

My podcasting partner Ben Brey (Capital Misallocation) put together the table below aggregating the current on and off-balance sheet commitments to AI capex of the hyper-scalers (as well as the 2 largest neo-clouds). These consolidated numbers are already massive - and growing fast. We have more to say on this topic - watch this space!

Back in February, I naively felt that a combination of free cash flow and the public/private debt markets would take care of the capex ambitions of the hyper-scalers. The numbers above already look staggering and one has to call into question for debt funding markets to absorb more paper.

Google (and Meta, Oracle and now possibly even Amazon) appear to be confirming that assumption as they announce equity fundraising plans.

#TheAgeOfReverseDe-EquitizationIsUponUs

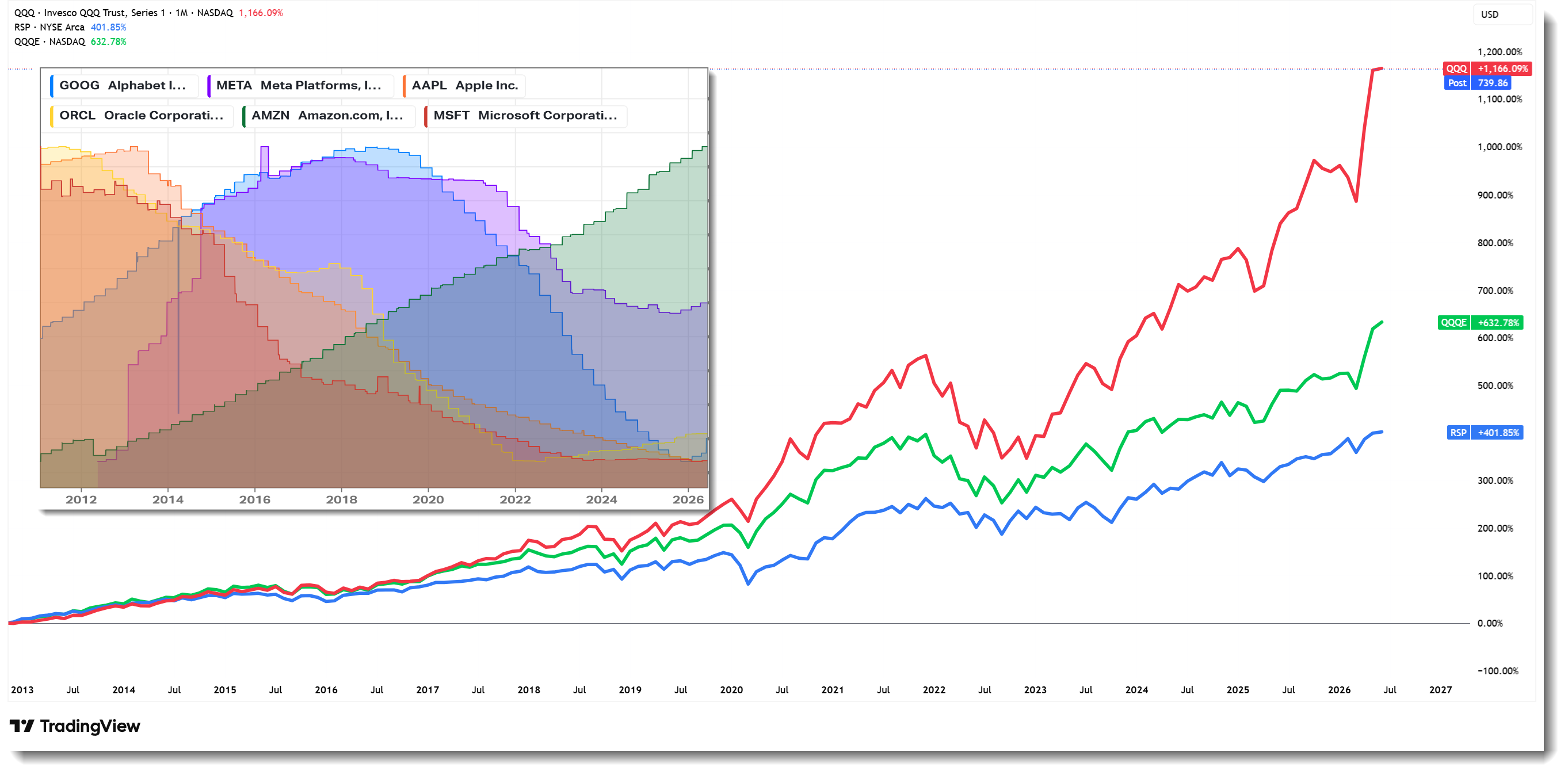

In early 2013, the combined market cap for Apple, Microsoft, and Google stood at shade under $1 trillion (Apple at $500bn and Microsoft and Google combining for c.$467bn). At that time, Facebook (Meta) was still relatively new to the public markets and much smaller.

Back in August 2023 I wrote a note about a decade of de-equitization at Apple (linked below).

‘Tim Apple’ was not the only tech CEO aggressively shrinking his share count. Between FY2013 and 2025 the tech giants spent well over $2 trillion on buybacks - a number that accelerated between 2020 and early 2024.

The notable exception from the group has been Amazon which, apart from a brief experiment with buybacks in 2022, has been a net equity issuer for most of its life (almost all via stock-based compensation - a staggering c.$100bn since 2020!).

Almost 40% of the total aggregate dollar value created by the Nasdaq 100 since 2013 can be directly attributed to the growth of Apple, Microsoft, Alphabet, and Meta - in no small part due to those repurchases.

Then came the capital demands of AI infrastructure. The last 12 months has just seen equity issuance turn net position for the first time since 2018.

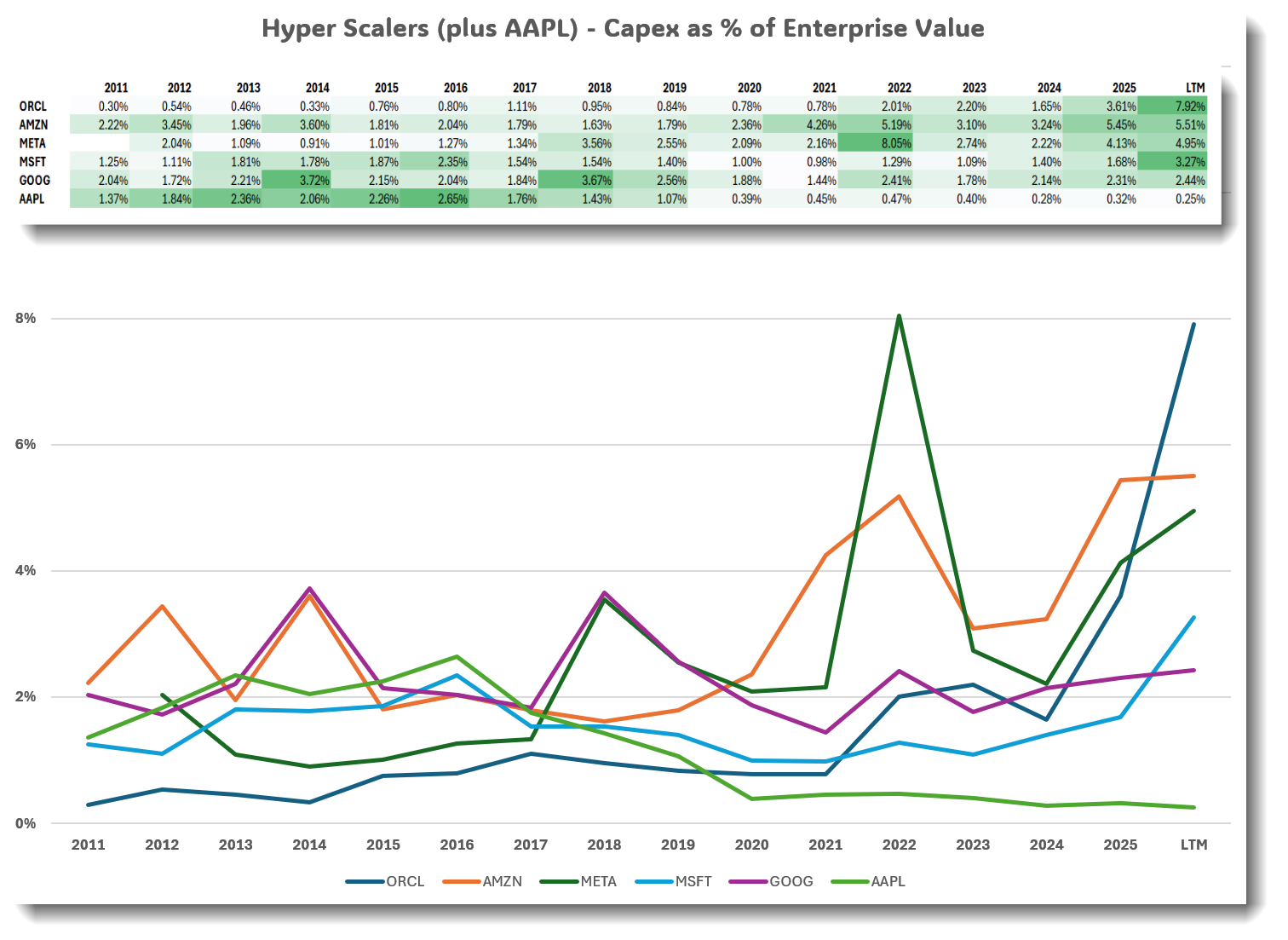

Capex as a percentage of EV has made a marked trend shift in the age of AI.

TLDR (for the rest of the note):

Supply is coming and the 🐿️ has a strong hunch that it will finally correct a market anomaly that has now prevailed for so long that most market participants have forgotten “the science”.

The Nasdaq has outperformed the equal-weight S&P500 by a factor of 4x in the past 13 years - a momentum trade for the ages supported in no small part by the de-equitization of the giants of large cap tech.

An era of net equity supply by these jumbo issuers (plus a potential slow down in 401k flows as AI removes white collar jobs) has the potential to trigger an overdue mean reversion (whereby RSP outperforms QQQ).

The 🐿️ has structured a convex trade idea to capitalize this view and is not betting the house to take it. At times this will get nerdy - but stick with me!

Settled Science (over full cycles, though not immune to extended momentum regimes…)

This is not going to be a Mike Green style treatise on the systemic risks created by the dominance of passive investing in modern markets (even if I agree with much of his work on the topic).