Gasoline Blues

The Blind Squirrel's Monday Morning Notes, 5th August 2024.

I get that Friday’s non-farm payroll number was below expectations and came hot on the heels of Thursday’s weak PMI print. However, the reaction in the bond market was extreme. Too much, too soon?

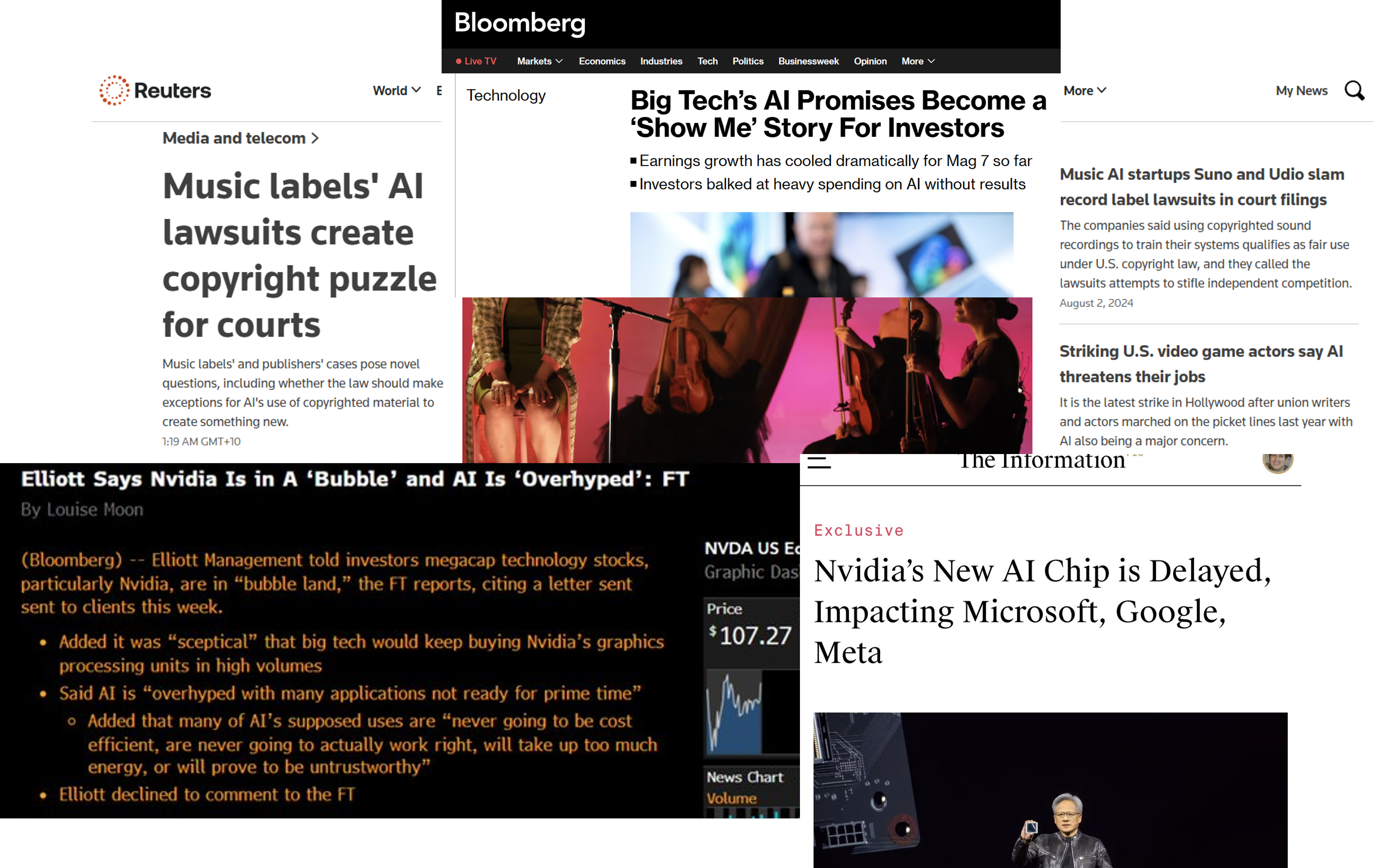

I suspect that real catalyst for market disruption has been the air coming out of the tires of the Generative AI momentum rally. What started as a blasphemous whisper at the start of Q2 earnings season has evolved into what appears to be a full-throated chorus of cynicism around the economic opportunity associated with AI’s large language models.

Are we finally hearing the sucking sound of asset repatriation by foreigners? Even a removal of the most recent (since Covid) net additions to equity and treasury positions would represent a massive removal of liquidity.

In Section Two this week, we build on a thesis that we sketched out last month, namely the role that long-dated crude oil futures contracts could play in portfolios as we potentially enter a period of inflation volatility (a partial explainer of the title!).

Gasoline Blues

This past week’s market action was a salutary reminder that market drawdowns will find a way of making themselves felt even when you think that you are well hedged and keeping your risk tight. Am glad we had them, but no amount of Japanese Yen calls, convex interest rate bets or SOXX 0.00%↑ put options can fully protect a portfolio containing too many ‘lazy longs’.

Friday was definitely the day for the 🐿️’s IBWOC Platinum Subscriber T-Shirt. Looks like everyone got Morris Sachs’ memo about the 2-Year Note! At the same time!

I get that Friday’s non-farm payroll number was below expectations and came hot on the heels of Thursday’s weak PMI print. However, the reaction in the bond market was extreme. To put it in perspective, Friday’s ‘flight to quality’ triggered a 1-day move in US 2-Year Note futures greater than the day that the world woke up to the reality of Covid-19 in February 2020.

I have certainly been in the camp that the median consumer is suffering and that the state of the economy is weaker than what has been suggested by recent hard data on growth and inflation. However, a cursory look ‘under the hood’ of Friday’s payrolls number would seem inconsistent with the reality of an imminent ‘bone-crushing’ recession. The jump in the unemployment rate seems to have been largely a function of labor supply from immigration.

The market finds itself (once again) reaching for narratives to justify price action when the more prosaic reality is that we are simply seeing the start of a normalization in positioning. The unwinding of the Japanese Yen funded carry trade has been the ‘dog that did not bark’ for the best part of the last 2 years. We have covered the risk extensively in these notes.

The Bank of Japan’s 1st interest rate hike in 17 years coming in the same week that Jerome Powell all but promised a rate cut in September was clearly capturing all the headlines. However, it is tough to believe that this miniscule adjustment to interest rate differentials is solely to blame for the rout in multiple asset markets. We enjoyed the win on our Yen calls, but it felt like a Pyrrhic victory!

I suspect that real catalyst for market disruption has been the air coming out of the tires of the Generative AI momentum rally. What started as a blasphemous whisper at the start of Q2 earnings season has evolved into what appears to be a full-throated chorus of cynicism around the economic opportunity associated with AI’s large language models.

When the biggest trade in the market starts to fail, risk managers start to get nervous. The violent sector / factor rotation that we saw in equity markets from mid-July as long/short books de-grossed has now given way to across the board selling and rising correlations.

Rising correlations place the spotlight on the crowded index dispersion trade. Our hedge against a ‘Dispersion Bust’ via an actively managed index straddle was one of the strategies that kept us out of trouble at the end of last week.

Another strategy that compensated for losses in the 🐿️’s long book last week was our tail hedge against interest rate cuts being priced (rapidly) back into the market via a call option in December SOFR futures.

Regular readers will know that this rodent has been dubious about the role of US Treasuries in investment portfolios. However, since early May, we have been employing a ‘bar bell’ risk management approach to fixed income. I originally set this strategy out in Losing My Religion (paid section on this SOFR hedge has been taken out from behind the paywall).

Obviously on the flip side of this, the other side of our bond risk management bar bell strategy - a hedge against much higher long-dated yields - was down sharply on the week.

Our Fading the Utes bet against XLU 0.00%↑ (US utilities) also got crushed as investors rushed to the ‘safety’ of ‘bond proxy’ equity sectors (staples and healthcare in addition to the Utes). The market needs to decide whether these power companies are second derivative Generative AI growth plays or safe haven assets. I really don’t think they can be both!

My sense is that the rush into bonds at the end of last week has been overdone. The market has consistently overshot on both rate cut and rate hike expectations in the past year. Has it just done it once again? My instinct is to take the money and run on the SOFR calls and stay firm on the XLU 0.00%↑ and TLT 0.00%↑ ‘short’ positions.

One thing that will ensure I do not rush this decision was Friday’s significant weakness in the US dollar. In recent years, major ‘risk off’ events have been accompanied by a sharp appreciation in the US dollar (USD cash being the ultimate safe haven asset). Not this time.

Are we finally hearing the sucking sound of asset repatriation by foreigners? Even a removal of the most recent (since Covid) net additions to equity and treasury positions would represent a massive removal of liquidity.

Last week, I suggested that a negative wealth effect (from falling equities) could start to impact the broader economy: “lately it is strong equity markets that appear to have been a key forward indicator of economic activity and growth. It is not hard to paint a picture in which a popping (or even gentle deflation) of the AI hype bubble is actually what pushes the soft landing currently being priced by the market out of reach.”

If foreigners are indeed starting to sell US assets in earnest, then the economic case for those recently repriced rate cuts might begin to find a firmer footing. To be clear, this does not turn this rodent into a buyer of bonds. Regular readers will be aware of my ongoing quest to seek out alternative portfolio diversifiers to fixed income.

We have already made a strategic portfolio allocation to managed futures / trend (see ‘Handing some cash to the robots’). The next leg of our portfolio diversification exercise will finally make some sense of the fossil fuel related title of this week’s note.

In Section Two this week, we build on a thesis that we sketched out in ‘Stock Take: Part 1’, namely the role that long-dated crude oil futures contracts could play in portfolios as we potentially enter a period of inflation volatility.

‘Gasoline Blues’ is one of my favorite tracks from British blues legend John Mayall. The lyrics were inspired by the OPEC crisis of the early 1970s…

Mayall, who died 2 weeks ago at the age of 90, led an extraordinary career. He was still headlining gigs in his eighties! Although he never really became a household name (less than 9,000 Instagram followers as if blues legends care about those sorts of things!), Mayall’s original band, The Bluesbreakers was the incubator for some of the greats in the music business, including Eric Clapton, Peter Green, Mick Taylor, Mick Fleetwood and John McVie. Complete legend. Enjoy!

Don't miss out! Consider becoming a paid subscriber to support my work, gain access to an additional 60% of content, join our Discord community, and even receive merch!

Some feedback below from happy readers that have already taken the leap.

Keep reading with a 7-day free trial

Subscribe to Blind Squirrel Macro to keep reading this post and get 7 days of free access to the full post archives.