Zombie Beta

The Blind Squirrel's Monday Morning Notes, 4th November 2024.

Small cap US equities have been a key feature of the ‘Trump Trade’. The Russell 2000 (both futures and tracking ETFs) are the ‘one stop shop’ for this factor. The 🐿️ is wary of this ‘zombie beta’.

Zombie Beta

Last week, Mrs. 🐿️’s dad invited me to join him at an ASX-listed microcap conference organized by some of his old friends and former colleagues. Many thanks to Chairman Craig Dunstan for including me.

Incidentally, the title of this week’s piece has absolutely nothing to do with 2 days well spent here in Melbourne’s CBD. We shall move on to the referenced zombies later on.

Regular readers will know that the 🐿️ does not spend much time thinking or writing about microcaps. However, an opportunity to listen to 24 CEOs set out their stalls should never be passed up. A fascinating microcosm of the (global) real economy.

The presentations covered everything from a pre-production copper miner and a house builder (mandatory down here!) to an emerging brand in the global infant milk formula market (Bubs) and a (tiny) intriguing cleantech business 20%-owned by legendary metals investor Robert Friedland and Fidelity (no recommendation yet but more work still to be done by the 🐿️!).

According to the Australasian Investor Relations Association (AIRA), the median annual maintenance cost for smaller companies to be listed (those outside the ASX200) surveyed at A$4.4m (almost US$3m). Am sure that many of the companies above have cut a cheaper deal on their audit fees, however even a fraction of this median cost represents a significant percentage of market cap for many of these issuers.

This rodent is not simply lobbying for the local accounting and legal firms here. I celebrate the fact that many of these companies are not sitting in the portfolios of private equity funds. The discipline and transparency created by public disclosure requirements significantly derisks these businesses for potential strategic acquirers and partners and a public (if illiquid) float gives these companies a ‘currency’ in M&A roll-up markets (many of them are fairly active on that front).

For individuals, participation in standalone private equity deals poses multiple risks beyond the business risks of the underlying company. I am sure that many readers have ended up ‘losing’ on those (very rare) private market winners when they have found that their minority protections were lacking in the event of dilutive ‘emergency’ capital raises or ‘non-negotiable’ squeeze-out provisions in the event of a sale to a strategic or private equity buyer.

Microcaps play an important role in the capital markets food chain. It would be a massive shame to see this market disappear. However, as the world of ‘Big Retirement’ continues its ‘pincer movement’ drift towards market-cap weighted passive indexation of its public equities and the full embrace of ‘volatility laundered’ private asset markets, the world of active mid and small cap investing has become more fraught.

The ‘reach for small caps’ has become one of the major factors in the ‘Trump Trade’ thematic of recent weeks. The performance of the Russell 2000 small cap index (albeit still below the pre-Biden withdrawal peak in late July) has correlated closely with Trump’s election odds.

Back in July, the 🐿️ was certainly guilty of celebrating (while not fully embracing) the ‘great rotation’ out of large cap tech stocks into value / midcaps. However, even the strong recovery of the Russell 2000 (‘R2K’) in recent weeks has been unimpressive when compared with the tech behemoths.

Nevertheless, the promise of extended corporate tax cuts, deregulation, ‘America First’ trade policies and other promises of the Trump campaign seen as pro-growth has seen increased investor interest in small cap exposure (although momentum does appear to have stalled somewhat in the past 2 weeks).

Better technicians than this rodent such as my pal ‘MC’ over at MacroCharts are sensing all the hallmarks of a bull trap in the Russell. Crayons aside, the 🐿️ has, over the past few years, been coming to the conclusion that the Russell is a curious instrument for investors to trade.

The 🐿️’s forensic critique of the index may not matter. Politics aside, we are of course entering the strongest absolute and relative season of the year for small caps.

There are many ways in which the R2K and the ETFs and futures that track it could be viewed as ‘Zombie Beta’. And here the 🐿️ finally gets to the point where he justifies the Halloween-ish theme for this week’s note!

I am not disinterested in the idea of small cap and value equities having a decent ‘Santa Rally’ end to 2024 but please do not ever forget that the R2K/IWM is a deeply flawed ‘trading sardine’.

Nevertheless, in Section Two this week, we crunch the numbers and explain why the Russell could be a very unsuitable can of (preserved) oily fish.

Section Two

So let me explain why the 🐿️ struggles with the Russell 2000 index as an investment vehicle. It’s time to ‘lift the hood’.

You are ‘short calls’ on your winners. It may sound obvious, but a market-cap weighted small and mid-cap equity index suffers from a major compilation handicap. While the giant trees of the S&P 500 can continue to ‘grow to the skies’, the Russell 2000 consistently evicts its winners, replacing them with untested new entrants with every June rebalancing of the index.

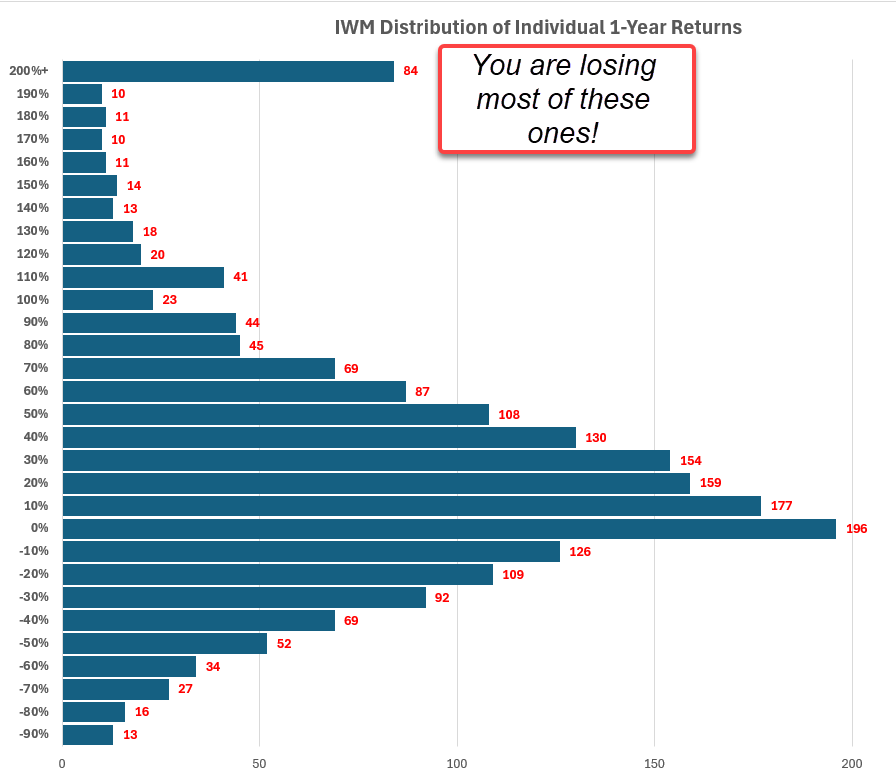

1-year total returns (dividends included) for the current R2K / IWM constituents. Source: Koyfin, 🐿️. In the past 12 months, 94 of the 1962 Russell constituents saw their share prices fall by more than 50%. The good news is that 253 names were up by more than 100%. Most of those winners, however, will go on to compound returns (unless they turn out to be fraudulent like SMCI 0.00%↑) in the larger cap indices.

Not properly exposed to the real economy. Here I will borrow another of Torsten Slok’s charts to illustrate the extent to which the ‘engine room’ of ‘SME’ corporate America is not properly represented by the public equity indices. Over 80% of these small and medium sized enterprises are in private hands!

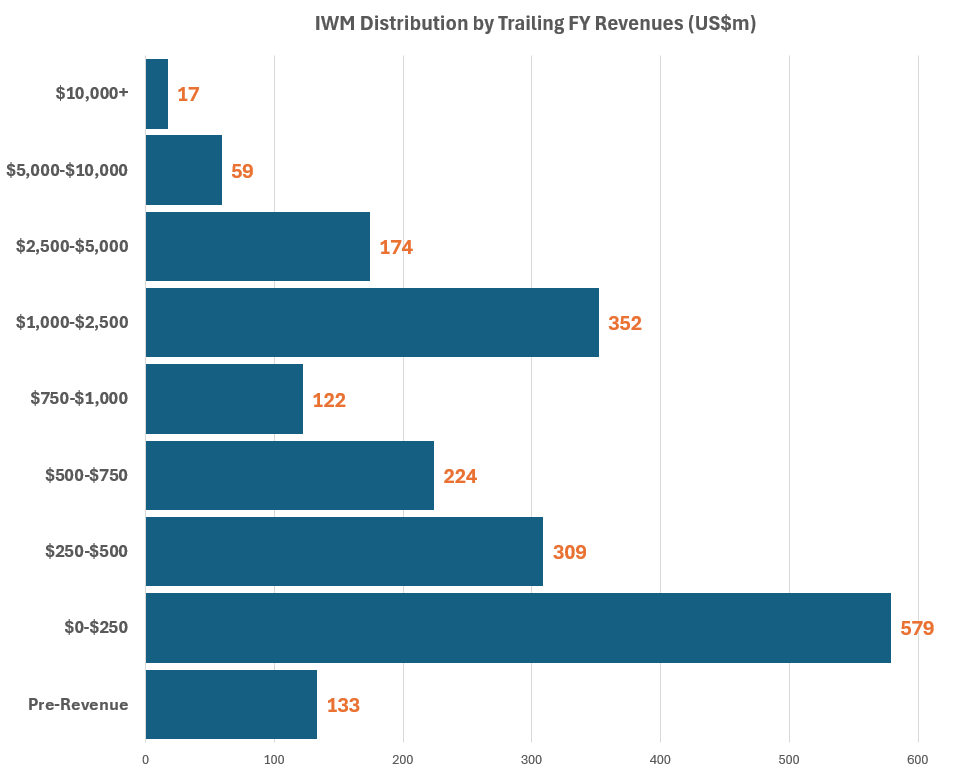

When it comes to revenues for Russell constituents, over 50% of the index booked revenues of $500m or less during the past financial year.

Source: Koyfin, 🐿️. Size is all that matters. While there may be some technical eligibility constraints, market cap is basically the only meaningful driver of R2K inclusion. In the current world in which narratives trump fundamentals when it comes to equity valuation, some potentially negative outcomes are inevitable. As of today, 43% (852 companies) of current Russell constituents had negative GAAP EPS for the last financial year.

Thanks to Apollo again for this one. It gets worse, 57% of constituents have an Altman Z-Score of below 1.8 (indicating an elevated risk of bankruptcy). While a larger share (64%) of the constituents was free cash flow positive, sadly stock-based compensation exceeded 50% of free cash flow among 45% of those issuers (naturally!). Only 14% of companies paid a dividend yield in excess of the 3.68% weighted average indicated dividend yield for the index.

Small does not equal cheap. On a forward PE basis, the R2K IWM 0.00%↑is actually more expensive than all of the other broad-based US equity indices. The Russell is not exactly a deep value play.

Diversification, but with a catch. At a superficial level, the R2K would appear to be better diversified than the tech-dominated S&P500 or Nasdaq 100 indices. However, this diversification also burdens you with 426 (largely pre-revenue biotech) healthcare stocks selected on the basis of market cap alone and 348 financial (mainly small regional bank) stocks with an average market cap of $1.6bn. Do you really know what you own?!

So, the Russell is basically a random ‘rag bag’ of economically unrepresentative, SBC-incinerating ‘sh#tcos’ with an ‘inverse Darwinian’ selection bias. R2K / IWM is clearly not a suitable long-term ‘buy and hold’ diversifier for your equity portfolio.

I wonder just how many 401(k) portfolios have a lazy IWM 0.00%↑ allocation in them. If you roll up the current IWM 0.00%↑ ETF (the largest but certainly not the only Russell tracker) assets under management as well as the E-Mini Russell 2000 Index futures open interest, you are looking at $80bn of capital engaged with that one ‘US small cap’ investment factor.

The world of factor-based investing has exploded in recent years. ‘Pods’ within the multi-strategy hedge funds have set up a myriad of quantitative trading systems that aim to exploit idiosyncrasies in how equities trade based on different fundamental and economic variables.

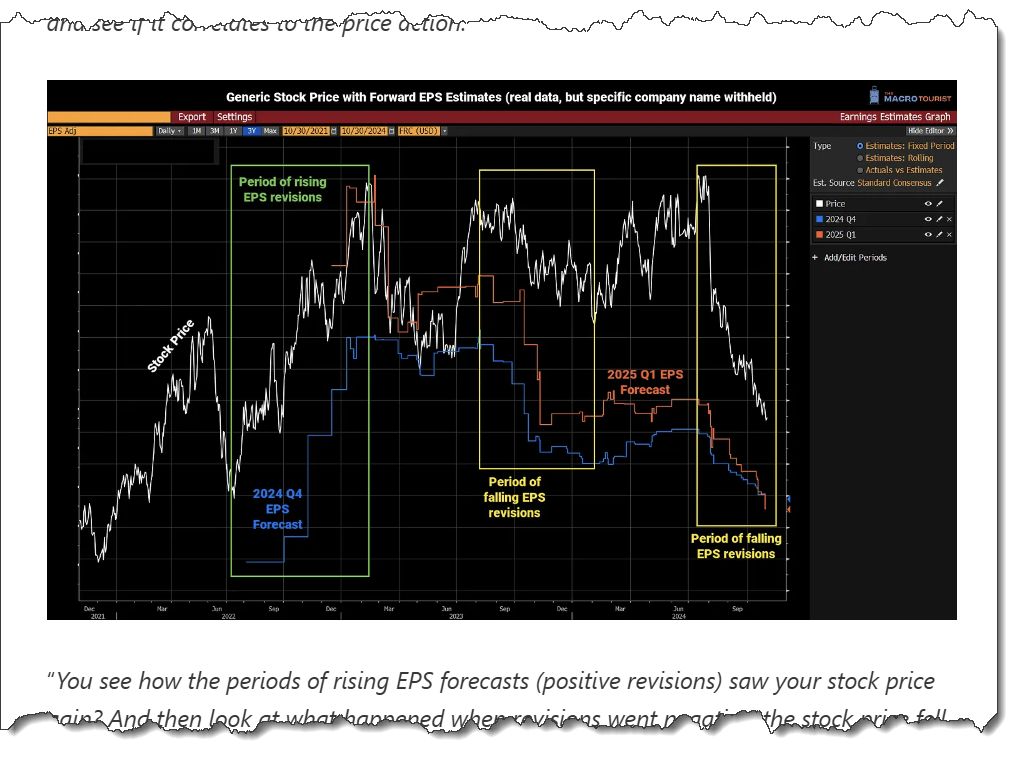

On that note, my good friend Kevin Muir wrote an excellent piece on how the EPS revision factor is increasingly at the root of stock moves. As if active investing in the value and midcap space was not hard enough! The (anonymized) stock that Kevin selected was particularly close to heart.

As mentioned above, the 🐿️ is not averse to the idea of a rally in risk assets once the election is out of the way. As I write (Sunday morning, Australia time), the Polymarket (yes, am aware of the potential bias issues with this measure) odds of a Republican sweep do not appear to be recovering from their precipitous drop that started mid-week. For now, outrage over the fate of the late Peanut the Squirrel do not appear to have impacted market pricing!

However, I do suspect that there is still a great deal of ‘red sweep’ money hanging out in the R2K / IWM trade. This will need to be reversed out in the event of a different electoral outcome before any kind of positive seasonal effect can kick in.

In any event, if you are believer in a ‘Santa Rally’, I think that (i) you can sit on your hands until you see a result this week and (ii) investors and traders can do much better than the ‘Zombie beta’ of the Russell 2000.

Before getting on to the Acorn review and portfolio update, I wanted to flag an area where I have started to do some work. That is very expensive North American restaurant chains. I keep the tiny (but very well constructed) EATZ 0.00%↑ Restaurant ETF on my market dashboard.

You would have thought that this group would be a pretty reliable barometer for the health of the real economy. Judging by its performance in the past 12 months, the US economy would appear to be doing just fine.

However, the 🐿️ is firmly in the camp of those thinking that last week’s correction in the valuation of Wingstop WING 0.00%↑ was long overdue.

Even after a 20% pruning, this purveyor of finest chicken wings still trades at a flighty (😉) 14.9x forward revenues. I am aware that there is a large cohort of burned short sellers when it comes to this name (one good friend refers to the restaurant chain as his own personal ‘widow maker’!).

The 🐿️ is not ready to add his name to that group but have been consistently intrigued by the extreme valuations of some of these growthy themed restaurant chains. Chipotle CMG 0.00%↑ has been a confounding stock market phenomenon for some time. New kid on the block, Mediterranean fast casual chain CAVA 0.00%↑, even makes Palantir look cheap!

At the moment, the US consumer is showing no sign of quitting.

However, this rodent believes that once this cycle truly starts to turn, these richly valued fast casual dining chains could derate dramatically. We will be ready. For now, it feels early and, as the legendary Bill Fleckenstein says, you only ever shoot stocks in the back!

As ever, if you have any questions, please message me via the button below or ping me in The Drey.