Sticking the Landing

The Blind Squirrel's Monday Morning Notes, November 20th, 2023.

Summary

Are we reading too much into the legendary Jim Chanos closing his hedge fund? ‘Hopium’ is a powerful drug for the value investing community.

Is the US economy going to ‘do a Simone Biles’ and stick its soft landing. This is indeed the prevailing narrative in the 2024 outlook reports from Wall Street. How should this 🐿️ respond?

I have no plans to fade this rally in long duration assets. In fact, we are cheerleading it all the way as we are very long one of the longest duration trades of all - uranium miners (since the mines hardly ever end up getting built!)

This week’s portfolio update and Acorn review (for paid subscribers) covers #uranium (in much more detail) plus #Ags#Energy #Offshore #PrivateEquity #Prosus #AUDUSD #ChIndia.

The audio companion to this week’s note will be uploaded to Substack on Tuesday to allow me to incorporate comments and feedback from this note. It will also be available as a podcast on Apple, Spotify and the other major podcast apps.

Sticking the Landing

The irony of the legendary Jim Chanos announcing the closure of his Kynikos Associates fund the week after I wrote a love letter to the short selling community is not lost on this 🐿️.

There is much excited speculation in value land that this move might mark a major turning point in the post GFC dominance of growth investing over all other style factors.

The news also happened to coincide with the expiry of (yet another) Tesla (worthless) put spread strategy in the main portfolio on Friday. Fitting (given that Chanos was one of the EV company’s most vocal bears).

This small position was one of the last remaining bearish bets in my equity book, as large cap tech stocks continue to pull the market towards fresh highs for the year. As ever, narratives need to be found to justify price action and we are back to the ‘landing’ debate.

TS Lombard’s Dario Perkins made my day (as well as his own clearly!) last week when he produced the chart below. Can there be any greater of illustration of the triumph of hope over experience when it comes to the popularity of ‘soft’ landing narratives just ahead of the reality of the recession biting?

According to Bank of America’s latest ‘Fund Manager Survey’, nearly three-quarters of their clients now expect a ‘soft’ or ‘no’ landing outcome for the US economy. Early autumnal concerns around risk assets have evaporated. Volatility has collapsed and the Santa Claus rally is on with a vengeance!

The strength of the rally in risk assets (with the notable exception of crude oil which appears to be telling a completely different economic story) has forced a tactical retreat from our bearish positioning in profit-less tech stocks and an implementation delay in our ‘short Big PE’ trade.

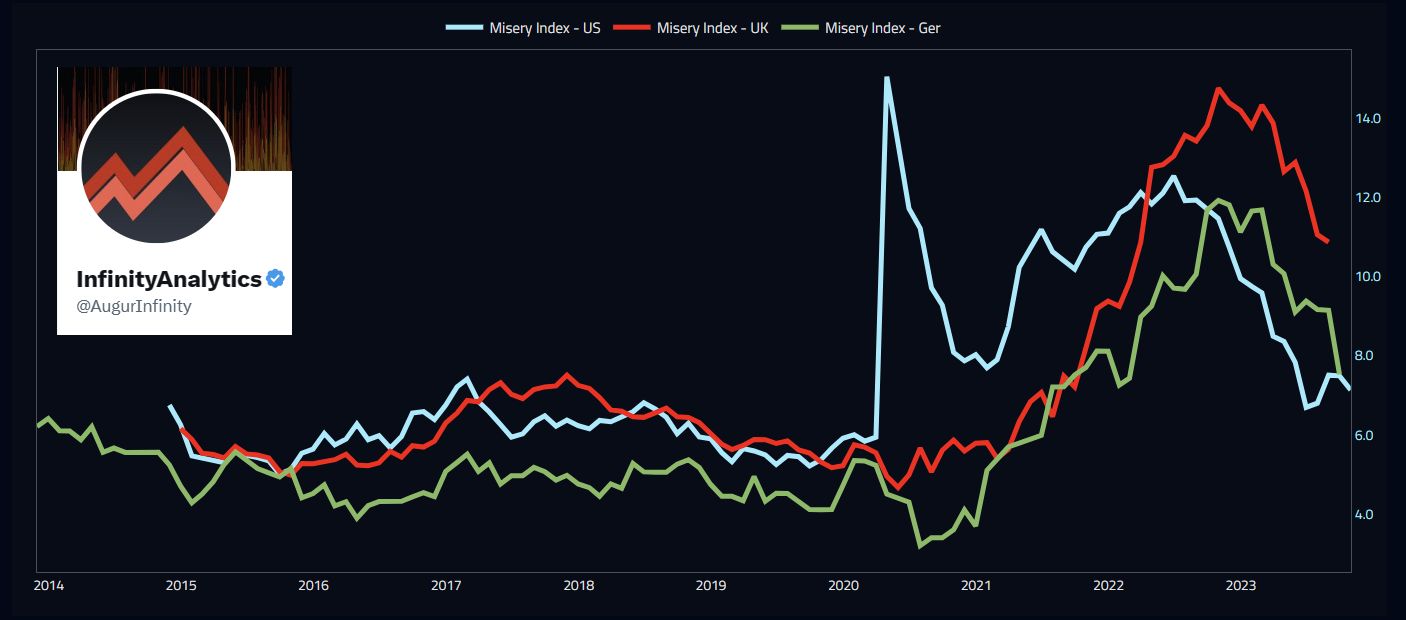

Are these recent moves simply a Pavlovic reaction to a collapse in the Misery Index (the sum of the unemployment and inflation rates)?

With a change in government on offer to 41% of the world’s population in 2024 (representing 80% of global market capitalization and 60% of global GDP), this could not come at a better time for (incumbent) politicians. Inflation rates are indeed falling (for now). It may be enough to get the bond market temporarily excited, but the 🐿️ is pretty sure that this data doesn’t fool the electorate. Dario again:

And then when it comes to employment, surely the true impact of the past couple of years’ interest rates hikes is yet to be fully reflected? The 🐿️ is keeping a close eye on (potentially significant) revisions to those jobs numbers.

As the holidays approach, fund managers’ inboxes are filling with 2024 market outlook pieces. My friends at Harkster have helpfully put them all together in one place. At the risk of over-simplifying, the broad narrative from the sell side points to falling inflation and bond yields; a weaker dollar, and a mild (or even non-existent!) recession.

The funny thing about consensus views is that they have an uncanny habit of not playing out. Right now, equity and bond markets are at the mercy of the year-end performance chase (by active managers) as well as systematic fund flows (from corporate buybacks, passive savings and structured product hedging activity). A heady cocktail to bet against.

The 🐿️ is sensing some ghosts from this time last year. So much so that I was prompted to have a look at what I was writing last November. It turns out that narratives rhyme…

There is a serious point here (Dario, mate, I promise I am not a stalker!). This is traditionally a dangerous time of year to be fading market strength. This time last year, a similarly ‘soft’ inflation print had just triggered a 2-day, 10% rally in the NASDAQ and had started to get “#SilverSqueeze” trending again on Twitter. Does that not feel eerily familiar?

With hindsight, we now know that markets then were in fact most probably reacting to a massive injection of global central bank liquidity released in response to the UK’s LDI / Gilts crisis. I covered this back in April in “I get it, Baldrick is Dogecoin”. What (more prosaic) reality are the narratives seeking to explain this time around?

In 2022, I made the (expensive) mistake of being skeptical around the year end risk rally in tech. Not this time. I have no intention of trying to fight this break-out in long duration equities. In fact, I currently have a large position in uranium and uranium miners (the ultimate duration asset since most of them will never actually build their mines!).

Although this is a commodity-specific special situation, the sector has a habit of attracting a (polite term) ‘faster’ type of money. A general ‘risk-off’ event would probably be very unhelpful to the cause.

I hesitated before writing up an Acorn on Uranium back in February. Back then I wrote: “It is an amazing macro / fundamental story that has an almost perfect track record as a heartbreaker of a trade. ‘The Great Uranium Short Squeeze’ is always just around the corner. It does, however, feel that the themes are now finally lining up.”

Away from equities, we have no position in developed markets fixed income for the time being. Last year, we played the bounce in TLT 0.00%↑ from the post UK Gilt crisis lows into the new year. We executed something similar this year in 30-year futures from the October lows (since exited).

We remain unexcited by long duration fixed income, but we are now working on a new bond Acorn for paid subscribers. The focus is on the front end of the curve this time.

That’s all for the front section this week. This week’s portfolio update and Acorn review for (beyond the wall) covers #uranium (in much more detail) plus #Ags#Energy #Offshore #PrivateEquity #Prosus #AUDUSD #ChIndia.

+++

We have just launched our subscription service. Find out more → Details here.