Nah mate, I just need to outrun you!

The Blind Squirrel's Monday Morning Notes, 26th February 2024.

Summary

Trading asset bubbles (consciously!) is a game of avoiding becoming the ‘second fastest’ (to the exit) when the inevitable ‘pop’ happens.

All that us mere mortals can rely on in the end is risk management. These days, that involves managing both upside and downside tail risks.

Bubble riding is one thing. ‘Team Saddlebags’ is playing a different form of ‘Chicken’.

In the second section, we look at adjustments that need to be made to our first FOMO trade (in semiconductors) and review interesting developments in a number of our acorn positions.

Welcome! I'm Rupert Mitchell aka The Blind Squirrel and this is my weekly newsletter on markets and investment ideas. If you've received it, then you either subscribed or someone forwarded it to you (add yourself to the list via the button below). Please also consider becoming a paid subscriber!

The audio companion to this week’s note will be uploaded to Substack on Tuesday to allow me to incorporate comments and feedback from this note. It will also be available as a podcast on Apple, Spotify and the other usual podcast apps.

Nah mate, I just need to outrun you!

I know that the original (probably Canadian!) proverb involves a bear - which may or may not be appropriate in the market context of today - but I am going to go with 2 squirrels and a cheetah on the African savannah. This is a rodent-based newsletter after all!

Trading asset bubbles (consciously!) is a game of avoiding being the ‘second fastest’ (to the exit) when the inevitable ‘pop’ happens. Even the most sophisticated participants in ‘greater fool’ markets fall into the trap of thinking that they will have the foresight to ‘call time’ on the madness and sell before the correction.

But leaving early is tough. It is a well-known fact that the greatest profits from bubble trading are attained during the final parabolic phase of a move. Your 🐿️ was feeling pretty clever back in January when I closed my long cocoa position (owned from December 2022). I was nervous of repeating my mistake of holding onto a sugar position for too long in late 2023. Failing to get out at the first sign of stalling momentum proved costly to that trade’s P&L.

Am I cross about this? No, not really. Hats-off to the hard-core trend following CTAs whose machines (i) saw no break in primary trend in early January and (ii) were not dealing with any psychological scar tissue from having recently given up some large gains in a different soft commodity.

I cannot believe that it was almost a year ago that Mrs. 🐿️’s compliance restricted list prevented me from calling time on ‘valuation lunacy’ at Nvidia. $400 per share ago! It is sometimes better to be lucky than good!

All that us mere mortals can rely on in the end is risk management. These days, that involves managing both upside and downside tail risks. Regular readers will know that the 🐿️ is a curmudgeonly value investor at heart. Who would have thought that owning some out of the money technology stock call options these past few weeks could be a more effective sleeping aid than a handful of Tamazepam and a bottle of Scotch?

In Handling the FOMO: Part 2 (we published ‘Part 1’ using SOXX 0.00%↑ two weeks earlier), we advocated buying low delta call options on the Nasdaq 100 (via the QQQ ETF) as an alternative to being sucked into the market euphoria:

How does this structure work versus an ‘all-in’ (common stock) commitment to US tech equities over the next 6 weeks? Let’s say that you wanted to allocate 25% of a notional $500k portfolio to the Nasdaq 100 today. A 10% move would add 2.5% to your performance on an outright (cash equity only) basis. Allocating 0.37% of that account to these calls would add 1.73%. On the upside you forego 0.86% of performance. Your downside is a ‘paper cut’. (Feb 8th, 2024).

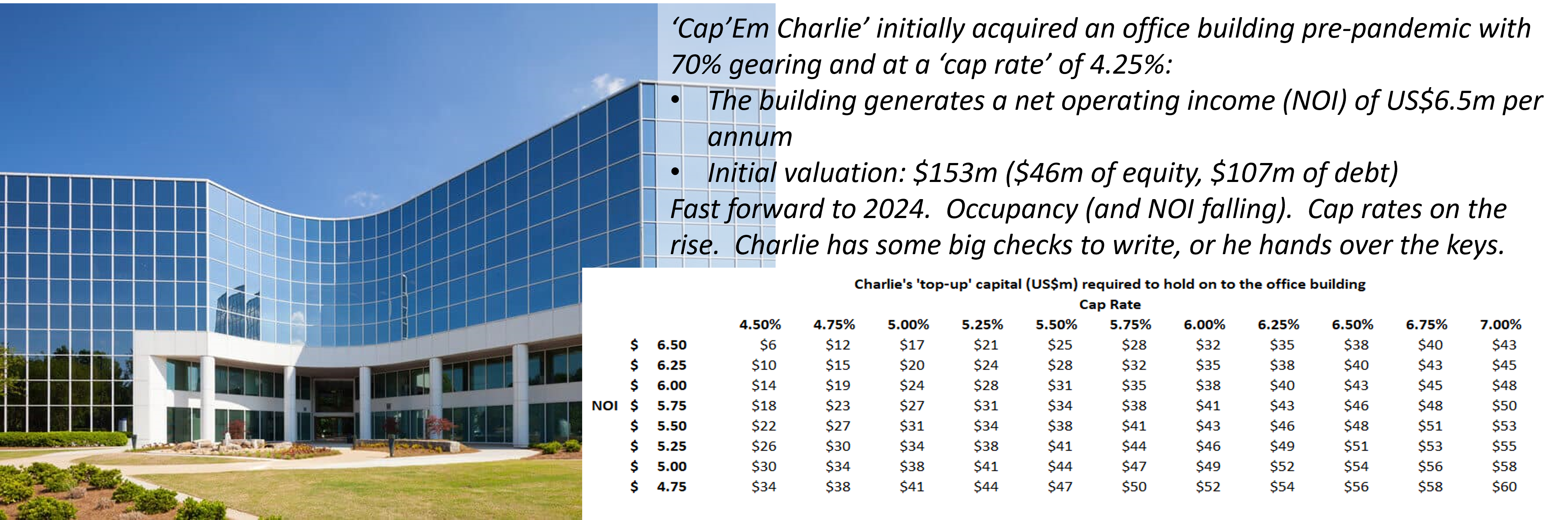

AI bubble riding is not the only example of a nervous prey weighing up their chances versus their peers. In the world of commercial real estate, asset owners anxiously monitor their cash flows and debt covenants. Many of these owners are facing the brutal realities of ‘cap rate’ mathematics.

There is simply not enough equity in their buildings to enable them to roll their commercial mortgages in the current interest rate environment. It has been over 20 years since I last read Tom Wolfe’s brilliant novel ‘A Man in Full’. The book plots the bankruptcy of a fictional Atlanta commercial real estate mogul, Charles “Cap’m Charlie” Croker.

The book contains the truly memorable ‘saddlebags’ scene in which Croker visits the ‘asset workout’ team at his bank. This is total ignominy since his bankers traditionally came to visit him in his palatial offices! It’s a scene that I imagine being played out on a daily basis in regional banks across the United States.

“The sweat patches under his arms had converged and were now running down his sides, forming a pair of saddlebags on his shirtfront. They were the size of two dinner plates, and they were darkening the fabric of his white shirt”…”The bankers stared at the saddlebags of sweat on Charlie Croker’s shirtfront. One of them whispered to another, ‘Is he melting?’ The other replied, ‘No, it’s worse. He’s evaporating.”

In the highly leveraged world of commercial real estate, equity disappears fast. Let’s do a quick worked example:

In reality, Charlie is almost certainly ‘handing over the keys’. He has lost his equity and also taken a blow to his ego, but his bankers now own a half-occupied office building which in many cases is worth a lot less than the outstanding amount on their loan. Do they really fancy repurposing these assets as residential dwellings or EV charging stations?!

Let’s face it. In the real world, the bankers have got ‘saddlebags’ too! When you owe the bank $100 it’s your problem, when you owe them $100m, it’s their problem! Credit markets are starting to be razor-focused on the CRE exposure of these regional banks.

The recent failure of New York Community Bancorp has put the KRE 0.00%↑ S&P Regional Banks ETF back to the top of everybody’s risk matrix.

The AI bubble traders are still fantasizing about infinite ‘total addressable markets’ of AI model training and inference. They may be vaguely aware of ‘hot’ CPI inflation prints and the latest utterances from voting members of the Fed’s FOMC but they are not hugely fussed. For now, tech equities do not care about the path of interest rates.

However, ‘Team Saddlebags’ is hanging on every single Delphic soundbite from these voters. The Treppwire podcast has become a regular listen for the 🐿️. Listening to the Trepp team run through the latest ‘fire sale’ transactions in commercial real estate as they plead for the relief of lower rates has a ‘Hunger Games’ vibe.

Unlike the bubble trader who is concerned about timing his exit, ‘Team Saddlebags’ is eyeing up its peer group hoping that the ‘Lag Reaper’ (©ChaseTaylor) of high rates comes for one of ‘those guys’ first and makes a sufficient mess for the Fed to start urgent, aggressive cuts to interest rates.

By the way, “Team Saddlebags” is now an official 🐿️ meme. It will cover all businesses that only exists because of the last decades of low to zero interest rate policies. Blackstone is Chairman Emeritus of the team!

The old mantra of ‘extend and pretend’ gets replaced with ‘keep up the denial until there is enough carnage elsewhere that the central bank has no choice but to bail out those of us that are left still standing’. Not quite as catchy really.

Now if regional commercial bankers and their clients are desperate for some aggressive dovishness from the Fed, spare a thought for the likes of the ECB’s Christine Lagarde, the BOE’s Andrew Bailey and the RBA’s Michele Bullock!

Pain in their own real economies (represented by small and medium sized domestic businesses) is much more closely linked to prevailing front-end / cash rates (before you even get to the pain in residential mortgages!). These major employers are not in the privileged position of having termed out their debt at low rates during the pandemic.

However, the foreign central bankers need to weigh up the risks (to their own currencies and domestic inflation rates) of moving to cut interest rates ahead of the United States.

A ‘controlled detonation’ of a handful of regional banks may indeed be preferable for Jerome Powell and his colleagues relative to the implications of starting an interest rate easing cycle that was deemed premature by a bond market that is spotting signs of re-emerging inflation. But Powell might not have a choice if there is an accident.

Last week, we published an ultra-low-cost strategy to hedge against the risk of the Fed losing control over the long end of the treasury curve (i.e., much higher yields). This is not a base case for the 🐿️, but the various ‘Team Saddlebags’ among the US regional banks and foreign central banks might well be secretly yearning for the emergency cuts that might trigger it.

Special request. Valentine’s Day 💓 marked the 1st anniversary of Blind Squirrel Macro going live on Substack. I have put together a brief reader survey. Thank you if you have already completed it. If not, it will only take 30 seconds of your time to complete, and I would love your feedback as I strive to make the content better. Important: Please add your email to the comments box if you would like a reply (otherwise it’s 100% anonymous)!

That’s it for the front section this week. In Section Two (for paid subscribers), we look at adjustments that need to be made to our first FOMO trade in semiconductors and review interesting developments in a number of our acorn positions.