Confessions of a ‘China Reopening’ Bag-holder

The Blind Squirrel's Monday Morning Notes, May 15th 2023.

Summary

We have been “China Reopening” bulls year to date. It has largely been an ‘expensive’ point of view to hold but have we been saved by the famous curse of The Economist cover?

It’s less than a year since asset allocators told their clients that Chinese assets were un-investable. This is embarrassing, but fortunately they have an out. There is another major East Asian nation that tends to do well when China is thriving.

Japan is a great ‘first derivative’ investment for those who dare not tell their LP investors that they want back in to China. It also happens to be a cheap market relative to the rest of the world and priced in a cheap currency.

In calmer waters, on the other side of the ‘X date’ and related US political shenanigans, we shall be adding Japanese and other China-related exposures.

In the Acorn portfolio, we are excited about our new position in wheat WEAT 0.00%↑ and about the latest developments at Goldman GS 0.00%↑ , in uranium URA 0.00%↑ and Occidental Petroleum OXY 0.00%↑

Confessions of a ‘China Reopening’ Bag-holder

I promise I am not trying to be contrarian. I fully confess that, at the moment, the 🐿️ is 100% a ‘China Re-opening’ bag holder1:

While we trimmed some of our copper and other industrial metal exposures in Q1, we still have have plenty of them.

We are not short of energy / crude exposure either.

We banked some decent profits on our Tencent / Prosus ‘Acorn’ option trade, but are almost ‘round-tripping’ the balance.

Plenty of China ‘value’ (real estate and banks) sitting within the $DVYE too.

Owning luxury car manufacturers (i.e., Mercedes Benz) is hardly a classic ‘short China’ trade either.

To cap it off, we just started a major portfolio position in the greatest China derivative of all, the Ozzie Dollar!

Combined with a near allergy to owning large cap US tech stocks, the 🐿️portfolio is having a far from ideal start to 2023. However, let’s be clear, narratives ALWAYS love to follow price action…

and so we fully expected to be reading the following:

However, imagine my delight when one of my favorite analysts, AM/FX writer Brent Donnelly, the self-appointed Chief Investment Officer of Magazine Cover Capital went with the following lead item for his excellent and highly recommended

...

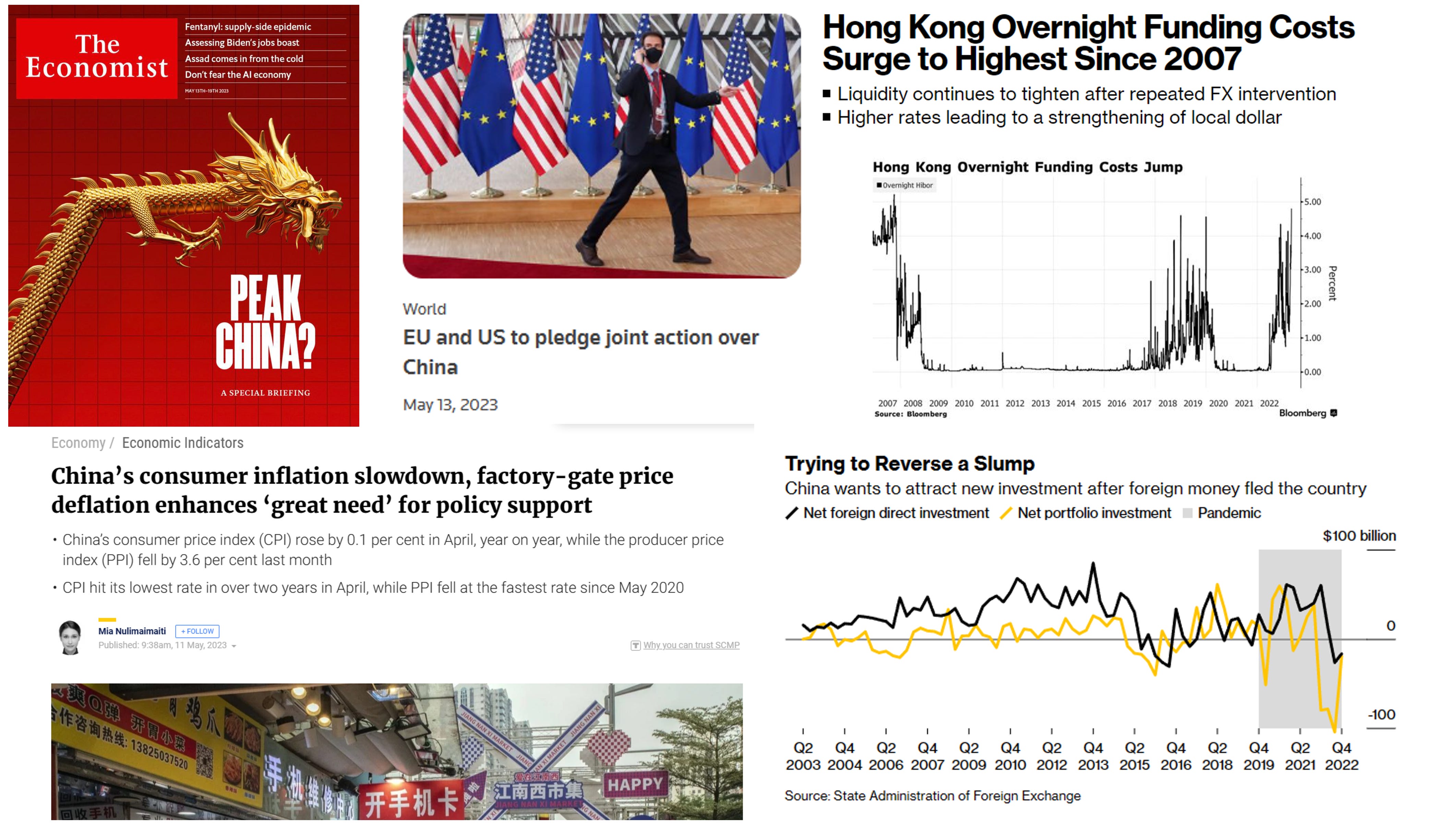

…just a matter of hours before Magazine Cover Capital’s favorite ‘pole star’ contrarian indicator, The Economist, went out with its “Peak China” cover (top left in our montage above). Brent is spot on about the mood, narrative and the price action but will the curse of The Economist cover once again work its magic?

Bruce Mehlman’s influential quarterly slide deck also just dropped last week. Always an excellent read. Mehlman Consulting distribute it for free and it’s all over social media but I attach it below in case you missed it.

This quarter’s first section was devoted to a section on China that concluded with ideas on how to take advantage of a re-shoring (away from China) investment thematic. The trouble is is that it contained this slide:

It strikes the 🐿️ that this ship - in terms of the tectonic plates of global trade - sailed a while ago. A quick scan through Cognitive Investments Jacob Shapiro’s must-read Global Situation Report [link to free sign up] will tell you that Australia is busy sending trade commissions back to China after a long hiatus while Vietnam “does not have the infrastructure capacity to accept any more re-shoring investment”. In a similar vein, the industrial hubs of northern Mexico are already heaving with Chinese manufacturers.

We then were amused to open our friend Erik's

on Saturday, pointing out how China / Asian equity bull runs have often been preceded by troubles in the US banking sector (in the early 1990s post the Savings & Loan crisis and again following the GFC). We love an echo...Erik ponders a world in which growing consumption sees “China flip[s] from trade surpluses to deficits [and] the rest of the world has to figure out what to do with all their RMB”. Implication could be China’s capital markets become the world’s largest where international investors currently own only a token allocation.

Yes, capital controls remain an issue today, but if the world’s apex consumer swings from San Francisco to Shenzhen, capital flight fears are replaced by a steady tide of RMB in need of a home in Chinese financial assets. We buy in to this long term theme.

However, at this point in time, your average Western asset allocator is sweating bullets. It is less than a year since he/ she was telling endowment trustees and investment committees that Chinese financial assets were ‘un-investable’. Yikes. This is embarrassing. Fortunately, he / she has an out. There is another major East Asian nation that tends to do well when China is thriving.

Japan is a great ‘first derivative’ investment for those who dare not tell their LP investors that they want back in to China. It also happens to be a cheap market relative to the rest of the world and priced in a cheap currency. The market also just got a very vocal endorsement the other day from everyone’s favorite investing nonagenarian, Warren Buffet.

Our friend Chase Taylor has been collating some great thoughts on Japan lately, most recently in this weekend's

. Valuation differentials are compelling. You could argue that we have seen the "improving governance" movie in Japan many times before, but it does feel like it has teeth this time.However, the trump card of a Japan investment thesis would be the great capital repatriation trade (refresh your memory on that argument in our 'Squ-ISDA' piece from a month ago).

So far, we have not hit the big buy button on Japanese equities. We are long the currency and there is a semi-written ‘Acorn’ report on Japanese equities sitting in my ‘drafts’ folder. Our only reason to hold back is general risk concerns.

I do not intend to spill ink over ‘x-dates’, debt ceilings and technical defaults by the US Treasury. Read about that elsewhere (Fintwit's Paulo Macro would be a good place to start). Bottom line, if something bad happens and even if then it is rapidly fudged fixed, I see no upside in having fresh risk positions in the portfolio. I just makes way too much sense to this 🐿️ to wait.

In calmer waters, on the other side of the ‘X date’ and US political shenanigans, we shall be adding Japanese and other China-related exposures.

I try and respond to every note I receive as well as reader’s comments here on Substack (unsubtle hint: likes and comments may seem trivial but they do something funky to Substack’s algorithms which helps new readers discover me - which is really good for 🐿️s). Sharing really helps us too! 👇

Keep reading with a 7-day free trial

Subscribe to Blind Squirrel Macro to keep reading this post and get 7 days of free access to the full post archives.