Absorbing the 🐋before 'Liberation Day'

March 31st, 2025. Weekly update for the 🐿️'s BUSHY™ Multi Asset ETF Portfolio and live Acorn trade ideas. 2025, Week 13.

8pm EST (Sunday) / 11am Melbourne Time (Monday). Given all of the tape bombs hitting I am getting this note out 12 hours early as history is being re-written by the hour. Good luck out there. Could be a tough week.

Before we get going, a quick reminder to add my conversation with ECM veteran Craig Coben to your listening / watching queue in case you missed it last week. We had a fantastic chat about the state of the IPO markets and our forecasts for the Coreweave IPO. CRWV 0.00%↑’s debut on Friday was about as messy as we had expected.

The weekend notes this week covered my latest views on Indian equities - one of the few emerging markets that the 🐿️ is not excited about for 2025.

We start this week’s weekly portfolio review with a quick clip from my favorite finance podcast, The Market Huddle. In part one, Kevin Muir interviewed Mi2’s Julian Brigden. Julian is a fully signed up subscriber to the asset rotation trade, so the conversation was dangerous for the 🐿️’s confirmation bias.

In part two of the show, Kevin and Patrick turned to the topic of the ‘JP Morgan whale’ trade. I tease Kev about being the ‘Captain Ahab’ to this particular derivative marine mammal. He has written about it to the point of obsession. Latest piece here (it is paywalled, but if you email him at (kevin@themacrotourist.com) I am sure he will send you a copy).

A quick description of the 🐋 trade in Kev’s words: “JP Morgan Asset Management created a fund named the Hedged Equity Fund (JHEQX), which invests in the S&P 500, and then each quarter, buys a put-spread to protect the position. To help defray the cost of that put spread, they also sell an out-of-the-money call.”

The quarterly roll of this giant hedge position (JHEQX has $20bn of assets) usually passes without too much fanfare, but Kev and Patrick were absolutely right to focus on it this weekend. Listen to this quick clip (link via the image below - 60 seconds) where Kevin discusses the predicament facing the option dealers on the other side of JP Morgan’s hedge as we go into month end with the S&P pinned at the upper strike of the put spread.

If negative sentiment created by the sloppy IPO debut from Coreweave was not enough, the story from the Washington Post over the weekend that Trump has instructed his trade team to ‘go bigger’ on the announced ‘Liberation Day’ tariff package will have made for tough reading for any of those option dealers not over-hedged going into the weekend.

As I write this on Monday morning (Melbourne time), S&P futures have opened down 70 basis points. Just to add icing to the cake, Goldman have just published a macro price raising their tariff assumptions for the 2nd time in as many weeks and calling for an additional 0.5% on core PCE inflation and bumping their 12-month US recession odds to 35%.

It could be another tough week in markets. Spare a thought also for the Morgan Stanley trader charged with managing the stabilization book for the CRWV 0.00%↑ IPO (if he has any bullets left after Friday afternoon).

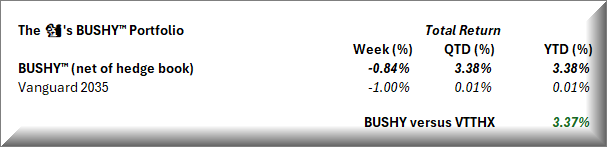

The BUSHY™ Portfolio - Week 13

Plenty going on this week besides the usual BUSHY™ update (which includes some thoughts on BUSHY’s hedge overlay). Acorn updates this week include deep coverage of our short book (‘BoyzToyz’, utilities, SaaS, Big Privates) and our volatility, rates and credit hedges.

Last week, BUSHY™ basically round tripped its gains from the previous week. Our Vanguard benchmark is back to flat on the year.

The portfolio leaked returns on all sleeves with the exception of precious metals (this was one of those weeks when you feel that you can never own enough gold), the CTA / trend following allocation and the High Yield credit hedge position (which is now 8% of 🐿️ NAV).