But 🐿️, it's the next China!

The Blind Squirrel's Monday Morning Notes. Year 3; Week 13.

If China is uninvestable, how come the traditional Indian equity bull case is that it’s the ‘next China’? 🤷♂️

Before we kick off, a quick reminder to check out my conversation with Craig Coben on the eve of Coreweave’s messy IPO debut on Friday. It has aged pretty well so far! Link here 👇 (it is also in your podcast feeds):

But 🐿️, it's the next China!

That oft repeated mantra that ‘The World’s Largest Democracy’ is destined to become a great economic power has been trumpeted into the 🐿️’s ears for just about as long as he has been involved in markets. Frankly from even well before China was big deal!

This rodent has earned his frequent flier miles in Indian capital markets! In the mid-1990s I was involved in raising capital for Indian corporates via London-listed GDRs. By the time I had moved out to Asia in the late 90s, India was being looked after by capital markets teams in Hong Kong and Singapore.

I am not sure whether the Mumbai to Hong Kong ‘red eye’ flights are worse than their Delhi to London equivalent. Not sure it matters. Either way, Indian ECM was following the rodent around the world like one of the backup cars in a Top Gear Special.

When I was based back in Europe in the mid 2000s, I found myself involved in a new wave of London Stock Exchange listings for Indian corporates and then spent much of the 2008 financial crisis liability managing an (inherited) portfolio of Indian clients that were all defaulting on the privately placed convertible bonds they issued during the 2006/7 bull market. Not fun!

Two years on, and based back in Hong Kong, I was dealing with India again - wrangling with jumbo privatizations like the Coal India IPO, selling a couple of yards of HDFC overnight for the boss’s boss and trying not to get picked off up by Machiavellian private sector promoters (at least one of whom ended up doing jail time). By the way, the word promoter is the technical term for the controlling shareholder of an Indian listed company. Any association with the dark arts of stock promotion is entirely coincidental. Maybe.

I often observe how so many of the noisiest China ‘permabears’ have never set foot in Shanghai. When it comes to India, I am pretty sure that most of the vocal overseas Sensex cheerleaders of the past few years have limited experience of just how incredibly hard a market India is to do business in unless you are one of the politically connected tycoons.

The First Attempt at the ChIndia trade

The 🐿️ was way too early in trying to call a top in Indian equities during the summer of 2023.

Back then I was stopped out of a short position in INDA 0.00%↑, the MSCI India ETF pretty rapidly. I had underestimated two factors:

A continuation of the allergy to Chinese equities among the global asset allocator community that had led to a crowding by global and emerging market funds into Indian equities. The reweighting back to China I was calling for took much longer to emerge (if you believe that it is actually starting to happen now).

A further acceleration in the explosive growth of domestic equity investing culture within India. Domestic mutual fund AUMs doubled again, and a further 50 million retail brokerage accounts were created over the next 12 months.

Incidentally, it turns out that all of those copies of Benjamin Graham’s ‘The Intelligent Investor’ and Charlie Munger’s memoires that were discarded in disgust by value investors in the West when the market cap of Fartcoin topped $2.7bn last year have been finding their way to the market stalls of New Delhi.

The Current Trade

The 🐿️ re-shorted Indian equities in November of last year. A few factors triggered this return to the scene of the crime.

China’s ‘David Tepper’ moment in September had finally started some meaningful fund flows back into Chinese stocks. It felt to this rodent like the beginning of something bigger.

SEBI, the Indian securities regulator introduced a range of measures designed to curb excessive speculation by retail investors, who had collectively lost substantial amounts of money in leveraged trades. Futures and options volumes collapsed in response to the new rules. It makes you ponder as to just how much leverage alone (0DTE options, levered ETFs etc.) is responsible for the 2023/24 moves in US equities.

The new US administration’s focus on tariffs and trade. India is the 9th largest trading partner of the US with a trade deficit of almost $50bn in 2024 and it has some of the highest tariffs and non-tariff barriers of any nation globally. It did not look as though Modi’s strong personal relationship with Trump was going to be enough to help India’s plight on that front.

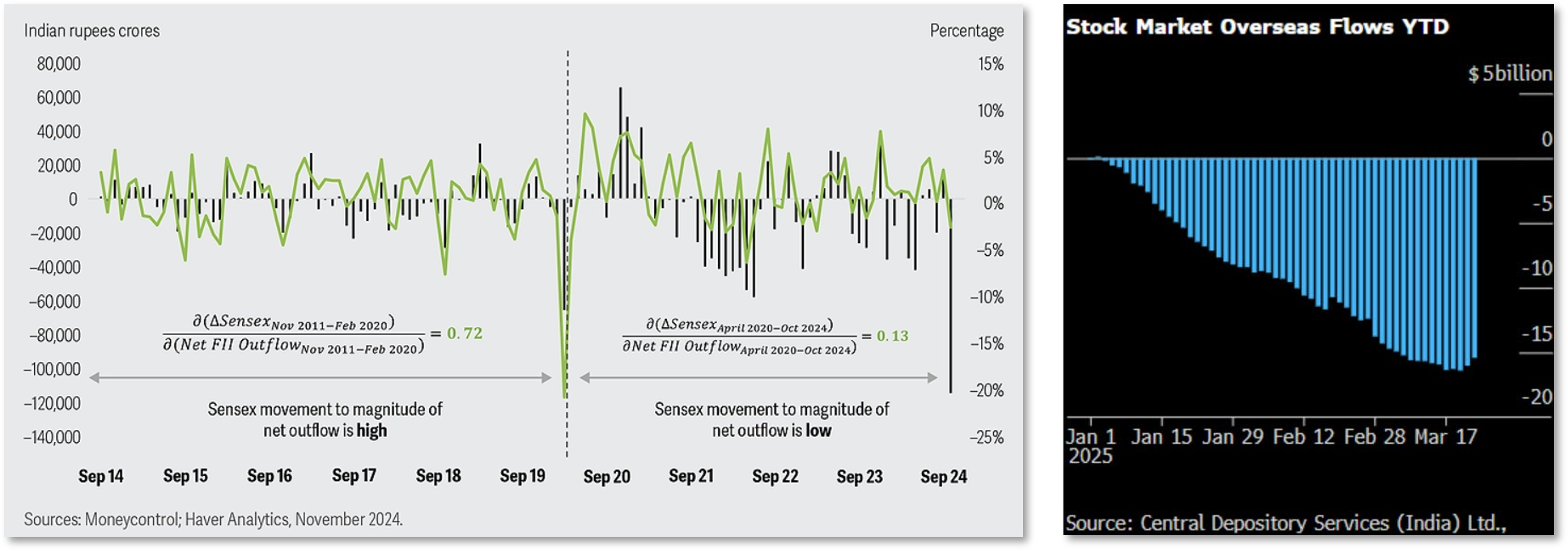

This combination of factors has seen significant volumes of foreign investment capital leave Indian equities. So far, outflows have exceeded by a significant margin those seen during the pandemic.

Year-to-date, India has been one of the few emerging markets not to benefit from the broader rotation into international assets. The pace of the equity outflows has indeed slowed in the past couple weeks allowing for a c. 7.5% rally off the recent lows in the MSCI India.

We need to reassess where we are in the life cycle of the India leg of our original ‘ChIndia’ (long China, short India) trade.

Taking Stock on Macro

Even with RBI policy rates steadfastly above 6%, core inflation is starting to tick back up. Not great.

We then need to reconsider where India sits in our increasingly multi-polar world. Since its independence, India has jealously guarded its strategic non-alignment. Like other BRICS nations, India continues to elect not to take sides among the great powers, and it is not immediately clear to this rodent that India can gain huge advantage from any ‘friend shoring’ / supply chain diversification / ‘China+1’ trends.

Ultimately, the new US administration wants Apple to make iPhones and MacBooks in Alabama not Andhra Pradesh. Can India really replicate China’s high-end manufacturing footprint, and would it ultimately be worth their while to do so? Modern high-end manufacturing is increasingly automated. India needs jobs for its hundreds of millions of young workers not for robots.

In March 2020, the Indian government introduced the PLI Scheme to provide financial incentives to domestic manufacturing. This funding was initially targeted towards pandemic-related global requirements (pharma and medical devices). PLI has since been expanded to cover a total of fourteen sectors.

Too much of India’s recent economic history has been a playbook of human capital cost arbitrage with the West. It strikes me that India’s much vaunted demographic edge has been squandered on optimizing, amplifying or providing a support function to intellectual property emanating from elsewhere in the world.

IT services accounts for a disproportionate share of India’s exports (and I am still not sure what the latest developments in AI mean for that industry) and the domestic pharma industry is principally focused on the manufacturing of generic drugs.

I was listening to Jacob Shapiro and Marko Papic discuss the thawing relations between China and India on their excellent Geopolitical Cousins podcast over the weekend. Apart from giggling at their trolling of every single Georgetown ‘alum’ Beltway geopolitical analyst, I was taken by their discussion around India.

The idea that an Entente Cordiale between Beijing and Delhi could see China offload some of the lower value manufacturing work to India (“the dirty stuff that America will not do and which only China can teach”) creating jobs and a larger consumer market for BYD cars and Xiaomi smart phones makes a lot of sense. That may indeed work, but does it justify one of the richest equity market valuations on the planet?

HDFC is as close to being a ‘one decision stock’ (overweight or very overweight) for emerging market managers as any. The Indian lender’s valuation got to almost 6x trailing price to book value in 2018. Even after a significant trimming of this multiple, its superior earnings growth profile to the likes of Brazil’s Itau or Singapore’s OCBC struggles to justify a 100% valuation premium in today’s market.

In the meantime, the latest budget from the Modi administration has opted in favor of populist cheap frills in the form of $12bn worth of middle-class tax cuts, while passing up a chance to ‘go big’ on the promised infrastructure investment and reforms that were their previously stated driver of growth. This feels like a mistake.

Then I come back to the lost Russian energy dividend. Cheap Russian crude and product has been an economic tailwind and inflation headwind for India in recent years. The share of India’s energy imports coming from Russia is finally starting to fall.

India is a serial devaluer of its currency and I do not think it is any coincidence that the 2022 to 2024 period of relative stability in USDINR happened at the same time that India was importing discounted Russian barrels and raising foreign currency via the sale of refined product.

If you want a secondary data point, just check out the windfall revenue and earnings at Reliance Industries’ refining operations from mid 2022 up until late last year.

Another major source of India’s foreign currency income is services exports from the country’s giant tech / ICT / BPO industry. These exports are very exposed to any reduction in global tech spending (which could come from AI substitution or from weaker growth in Western economies).

Bottom line, there are factors at play that could see the INR resume its weakening path in 2025. This trend could extend even if the US dollar continues on the weakening path (versus other currencies) that the 🐿️ expects for this year.

The mini rally we have seen in the past 3 weeks certainly feels fadeable. USDINR reversing and trending towards 88.50 to 90 by year end does not feel implausible in my view.

Finally, I want to talk about the weather. Agriculture remains the largest employer in India, accounting for approximately 46% of the total workforce. Historically, the performance of Indian equity indices has been heavily influenced by the quality of the annual monsoon growing period. Plentiful rainfall is good for stock prices and domestic consumption.

The bad news is that a phenomenon known as the Indian Ocean Dipole (‘IOD’) is currently forecast to be in a negative phase for the 2025 (June to August) monsoon growing season. In a negative IOD, precipitation that would normally come to India’s growing regions gets ‘robbed’ by Southeast Asia.

A negative IOD in combination with a neutral ENSO (when neither El Niño nor La Niña is present) that is also forecast significantly raises the probability of very dry monsoon for 2025. That would not be great for stocks.

So, how is the 🐿️ playing it.