Time for some Hard Yakka!

The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 12 of 2026.

In case you missed it, Benny & I sat down with Kuppy last Thursday afternoon. Check it out on YouTube. We chatted about ways to prepare yourself when markets are misbehaving. This week the🐿️ is trying to look beyond the Iran war and focus on his adopted homeland.

I hope I have been pretty clear on my gameplan for dealing with current markets. It is very simple - every day that the Strait of Hormuz remains closed to all traffic, I reduce risk, add to hedges and polish the ‘shopping list’ of CUSIPs that I intend to buy once the Strait is freely navigable.

The only exceptions to this aggressive de-grossing have been energy-related positions and agricultural commodities (effectively an indirect energy play).

It is time to position for the other side of the current crisis. It’s been 4 years since the 🐿️ made his home in the “Lucky Country” and am now just a few forms, a quiz and a ceremony away from becoming an Aussie citizen. Strewth! That happened fast!

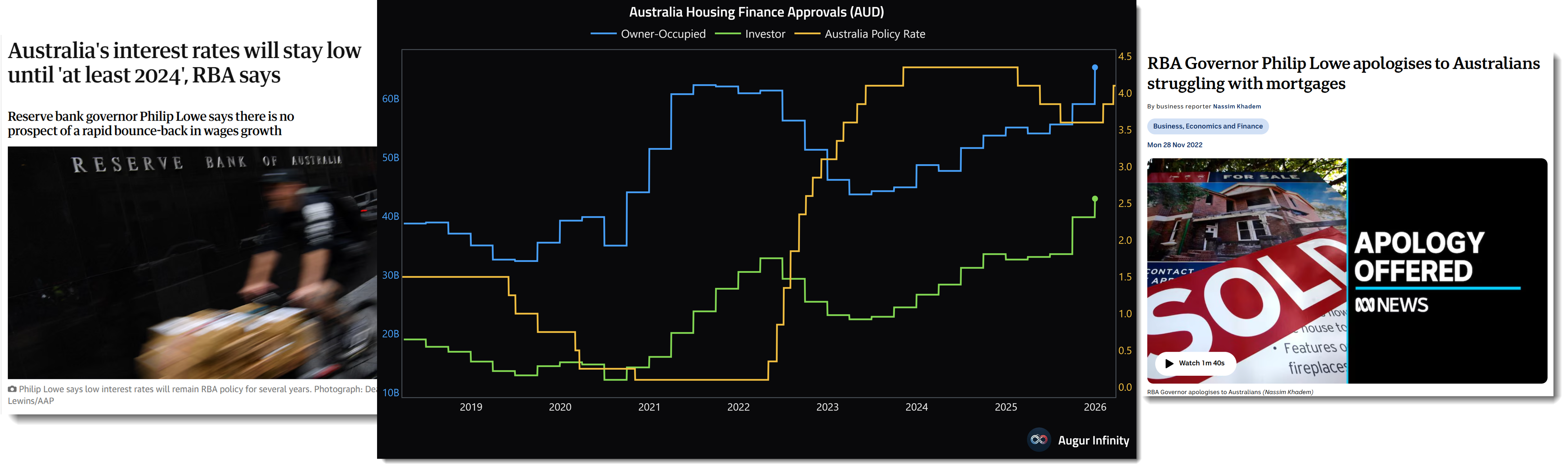

When I arrived in Melbourne in March 2022, the RBA was tackling a supply chain-driven inflation shock triggered by the pandemic and the Russian invasion of Ukraine.

Record levels of fiscal and monetary stimulus had left Australian households with roughly $240 billion in accumulated savings by the end of 2021, allowing businesses to pass higher costs on to consumers and wages to spike in response. ‘Tradies’ could name their price (if you could get one to even return your call).

The rate hikes came hard and fast on a real estate-obsessed population that had been given a green light from the central bankers to gear up on ‘propadee’ only the previous year.

How could such a wealthy and resource rich nation become so vulnerable to events taking place on the other side of the world?

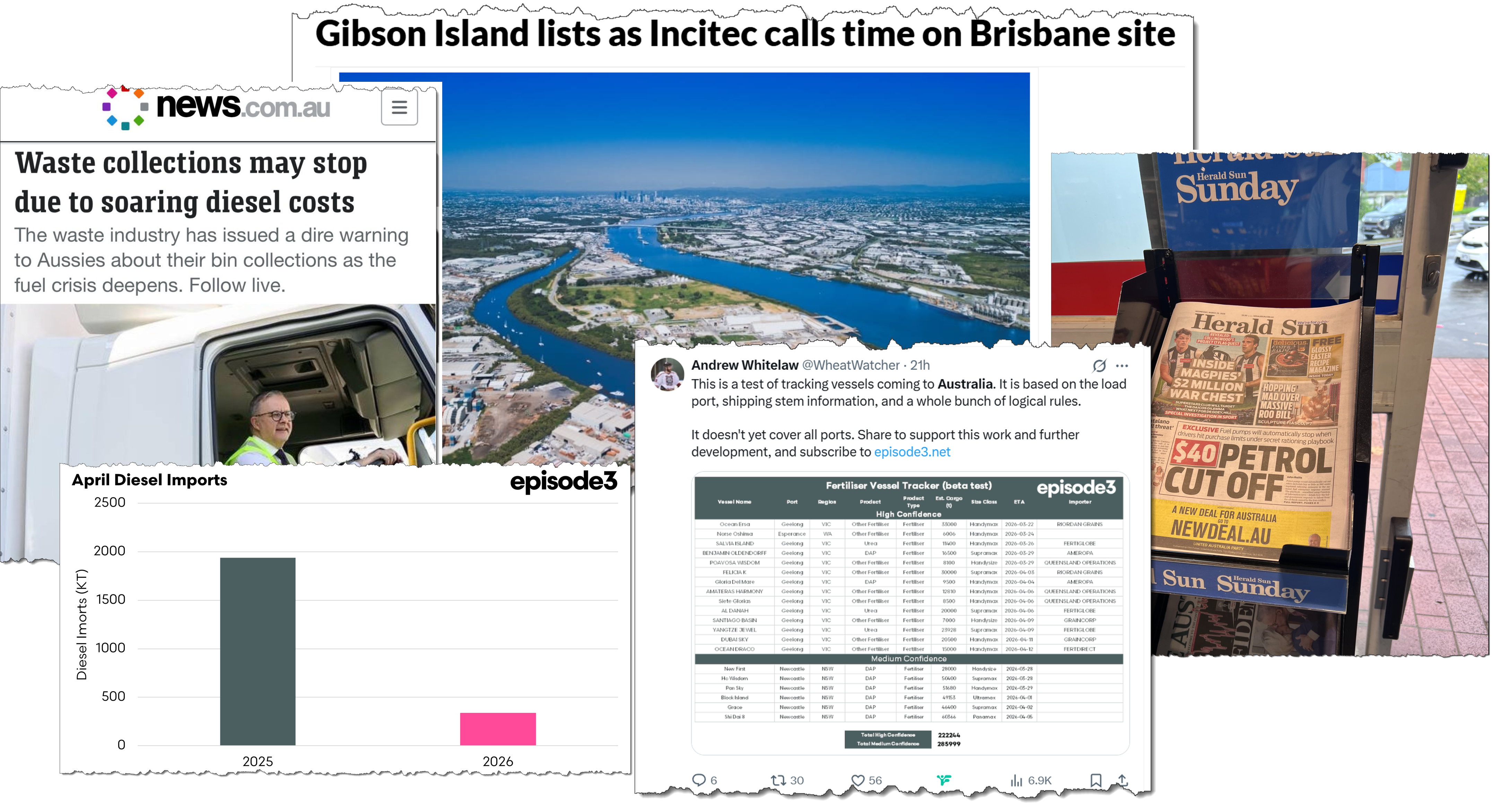

Yet, here we are again. Within 3 weeks of the start of the Iran war, we find ourselves perilously close to fuel rationing and in danger of not having enough nitrogen/urea for the the autumn preparation and winter crop sowing window.

3 years ago, I mistakenly thought that the lessons of 2020-2022 would prompt action. In “The Lucky Country. Finally!” (April 2023), I mistakenly felt that the new world order would be a tail wind for the currency.

“We shall rehearse the arguments about Australia’s ‘bonkers’ (technical term) residential real estate market and the RBA’s poor handling of its domestic rates market. All undeniable. We may well indeed have our first recession here since they were ‘outlawed’ in 1991. However, the “Lucky Country” is rich in the stuff which the world (not just China) is going to need for many years to come. It also happens to be one of few ‘reliable’ resource partners for the global West. There is also the natural bid to AUD that repatriation of (unhedged) assets by the country’s jumbo superannuation funds will supply as the boomer generation retires this decade. We suspect that, in hindsight, 2023 might look to be an outstanding entry point into the currency.”

The ‘Pacific Peso’ let me down. Only in the past 90 days has it recaptured that “outstanding entry point”. And to be clear, the currency has strengthened recently largely for the wrong reasons - a war premium on commodities that will partially unwind if the Strait reopens.

Why did I play the FX back then? I am often asked why I tend not to write much about Australian equities. Easy. Nosebleed expensive banks and a couple of large cap mining giants (I prefer Glencore) dominate one end of the market; resource plays that would make a Vancouver stock promoter blush at the other end; and anything interesting in the middle of the pack tends to get bid up to an insane multiple. Also, the Lucky Country already has way too many stock pundits.

In February, the ASX finally recaptured (briefly) its highs in US dollar terms of - wait for it - November 2007.

25 Years of Sovereign Resilience Erosion

It is now undeniable that we are in an “up ladder I’m on board” world. Perhaps the imminent shortage fuel, fertilizer and (probably) bog roll is the crisis my adopted homeland needs to force long overdue structural reform. Australia needs to ruggedize. It is time for some ‘hard yakka1’!

The China-driven mining boom of the 2000s infected Australia with a nasty Oceanian variant of ‘Dutch Disease’, the traditional curse of resource rich nations. I remember holidaying in Australia (from Hong Kong) in 2011. Taxis between the vineyards of Margaret River made private jet travel seem cost competitive.

The mining boom was great for the CUBs (‘cashed-up bogans’) but an Aussie Dollar at 1.10 was the death knell for domestic industry. Nothing could compete with cheap stuff from Asia. The Australian economy fast became a quarry with a speculative property bubble grafted on top.

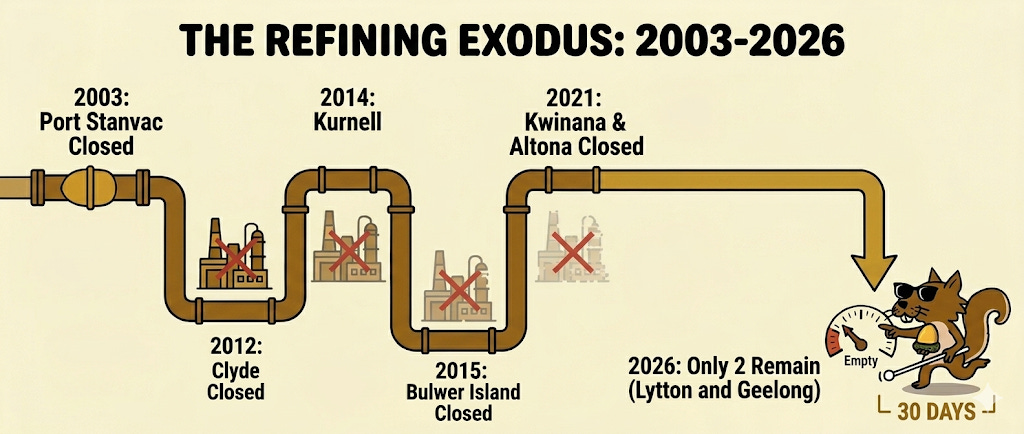

The strong currency wiped out Australia’s heavy manufacturing base. The automotive industry got hollowed out and then finally euthanized when the final Holden Commodore drove off the production line at the Elizabeth (SA) plant in 2017.

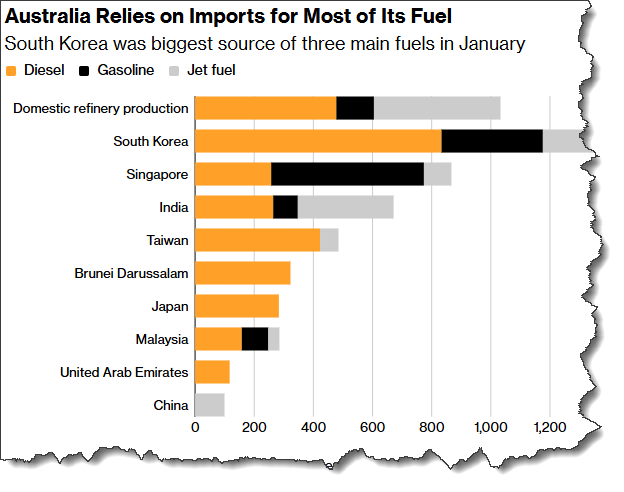

The strong dollar also came for domestic oil refining, leaving us today in the non-secure position of only 30 days of onshore stocks of refined product. Local refiners could not compete with cheap product coming from the mega-refineries of Greater China, Singapore, Korea and India. The closures came thick and fast.

As of early 2026, Australia refines less than 20% of its domestic annual consumption of gasoline, diesel, and aviation fuel. The only remaining operational assets are Ampol’s Lytton refinery in Brisbane (110kb/d) and Viva Energy’s Geelong refinery (120kb/d).

Storage might have helped with energy security but successive governments have balked at the A$20 billion bill for building the IEA-mandated 90 day stock requirement, arguing the toss that ‘product on water’ (en route from Asia) should be counted in the total. Cute (and inherently fragile).

The East Coast Gas Fiasco

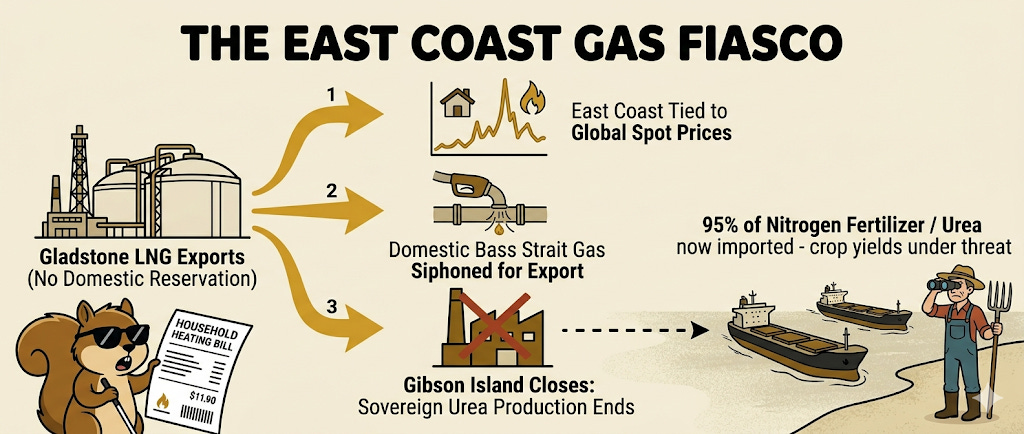

Somehow, notwithstanding the fact that Australia is a major producer of Natural Gas, the 🐿️ household’s heating bill is linked to the vagaries of the global LNG spot price.

In the early 2010s, the Gillard/Rudd governments approved the construction of three massive Liquefied Natural Gas (LNG) export terminals in Gladstone, Queensland. At the time, the Federal Government argued against a domestic gas reservation policy (like the one that successfully protects Western Australia), claiming it would “discourage investment”.

These projects linked the domestic East Coast gas network directly to international benchmark pricing. Worse still, when the LNG exporters couldn’t pump enough of their own gas to meet their Asian export contracts, they began siphoning gas directly out of the domestic southeastern market, accelerating the depletion of the Bass Strait resources down the road from me.

To compound matters the policy effectively ended the domestic production of urea. At the end of 2022, Incitec Pivot (now Dyno Nobel) shuttered its Gibson Island plant in Brisbane.

We now have a situation in which Australia, a global ‘bread basket’ with one of the largest reserves of agricultural land per capita of any nation on earth, now imports 95% of its nitrogen fertilizer / urea requirements.

Wheat, cotton, canola and even dairy (for pasture) farmers - already stressed out by cost and availability of diesel - are now staring down the barrel of significant yield loss if those dry bulkers do not make it through.

Greed and “private equity” thinking has seen the Lucky Country trade its sovereign resilience for the sake of the odd basis point profit margin. It’s time to harden up!

Imagining the Sovereign Resilience Fix

We are in the wailing and gnashing of teeth phase of political discourse at the moment. The blame-storming about the energy crisis needs to end. Frankly both main parties share responsibility for the situation in which Australia currently finds itself.

The Gladstone LNG disaster was a Labor policy failure but the Coalition’s repeated and forceful rejection of a national gas reservation policy had the same effect. The refinery closures happened on both parties’ watch. The absurd Pauline Hanson never was - and never will be - the answer.

Fortunately, we (I think I can almost say that) now hold some cards…

Natural Gas

Gas is the (relatively) easy fix, and Canberra already announced a reversal of the export framework for Gladstone LNG late last year. From 2027, the government will implement a “permit-based model” that legally restricts exports until LNG producers guarantee that 15-25% of the gas they extract is earmarked for local domestic use.

To bridge the gap until 2027, the government is forcing the massive East Coast joint ventures (Santos’ GLNG and Origin’s APLNG) to pledge domestic supply under a new “Gas Market Code”. This month, APLNG agreed to offer 40 petajoules of gas to the domestic market between now and 2029.

GLNG did sign an agreement in February to supply 200 petajoules over 10 years to the SA Government (specifically targeting industrial manufacturing like the Whyalla Steelworks). But this supply does not actually commence until March 2030, leaving a dangerous near-term gap that has not yet been credibly addressed.

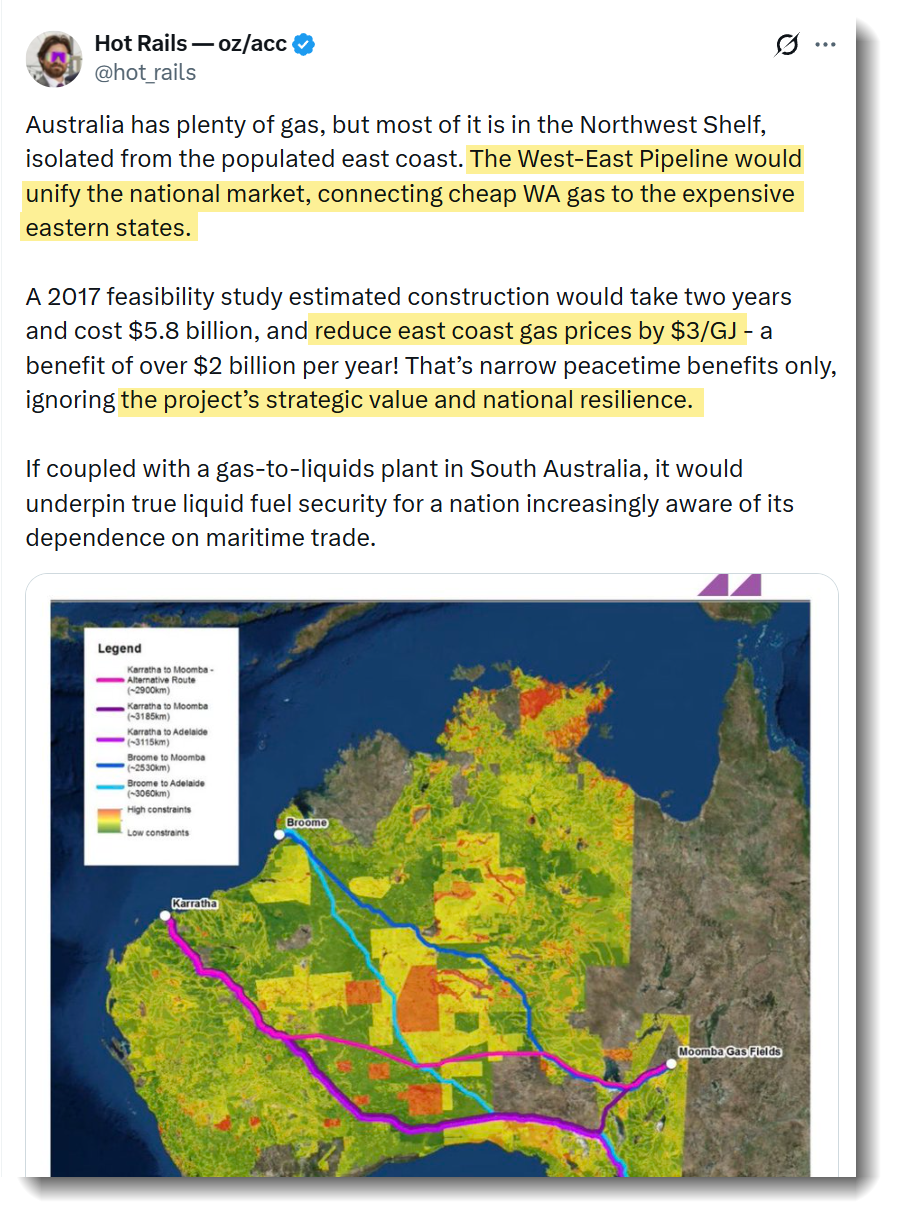

That should be just the start of it. Projects like the West-East gas pipeline have been kicked into the long grass by the consultant class in the past, I think the wake up calls of 2022 and today merit rescoring projects like this and its ilk through the prism of sovereign resilience.

Leadership in the Critical Minerals Race

Australia is not the only country looking to ruggedize its supply chains. The US defense apparatus has found out the hard way that its supply chains are completely vulnerable to China’s monopoly in rare earth processing. Australia has much of the raw material they need.

In late 2025, US signed consecutive critical minerals agreements with Australia and Japan. This framework explicitly pairs Japanese funding with Australian mining ventures to create a new closed-loop defense supply chain.

Real money is at work and the deals are coming:

Lynas Rare Earths (LYC: ASX) has been backed by Japan’s JOGMEC and Sojitz to supply WA rare earths for a processing facility in Texas part-funded by the US Department of Defense (USDoD).

Alcoa’s Gallium Refinery in WA. The USDoD / Australian government are co-investing with Japanese capital to secure the supply of gallium for advanced semiconductors used in military applications.

Ardea Resources (ARL:ASX) was also highlighted by the US Japan summit. Ardea has its Kalgoorlie Nickel Project (cobalt and nickel required for allied battery and defense supply chains) and now financial backing from Sumitomo & Mitsubishi for its feasibility study - a path to a $1bn AUS/US EXIM financing package.

International Graphite (IG6: ASX) is another potential US/Australia/Japan framework beneficiary in focus since China tightened is graphite export regulations.

Fertilizer Resilience

There are opportunities to play the transition toward sovereign fertilizer manufacturing through domestic gas-to-urea developers that are not looking to compete for resource with the Queensland LNG exporters:

NeuRizer (NRZ: ASX) is a (micro-cap) call option on the development of the Leigh Creek 1MTPA carbon-neutral urea facility in South Australia.

Strike Energy (STX: ASX)’s Project Haber in Western Australia is another major domestic urea development project seeking project financing even if the $6.5 billion Perdaman Ceres (2.3MTPA) facility (also in WA - and with a 20-year gas supply agreement from Woodside) is scheduled for completion in 2027. In a delicious twist of irony, the offtake agreement for Ceres is with none other than Dyno Nobel, the very company that closed Gibson Island in Brisbane.

The Carney Playbook

Of the public company situations set out above, Lynas already looks to have fully priced the opportunity. Ardea, Strike, International Graphite and NeuRizer still have plenty of project risk (and are priced accordingly). Probably not for this rodent but I am keeping an eye on them.

My point of raising these small and micro-cap situations is to highlight that there are plenty of shovel-ready projects around. A switch of gear towards an urgent focus on sovereign resilience is going to shift the dynamic in terms of project finance feasibility.

Canberra cannot fund this “Sovereign Security” capex on the federal budget alone. They are staring down the barrel of a $20 billion bill just to build empty fuel tanks, let alone underwrite critical mineral refineries and localized urea plants. But they have an ace up their sleeve.

According to the latest APRA data (December 2025), Australia’s total superannuation pool just hit A$4.5 trillion. To put that in perspective, Australia’s retirement savings pool is now approaching 170% of the country’s GDP - and growing at 8% per annum. About 50% of that total is invested outside of the country.

The super funds ran out of domestic bank stocks to buy a long time ago and have been increasingly lured offshore to camp out in US tech stocks, private equity and now more recently (and more scarily) private credit to US tech stock data center SPVs! Less than 6% of their AUM is allocated to domestic hard infrastructure.

The next thing for the Albanese government to do is take a leaf out of the Mark Carney playbook and harness the ‘super’ funds in the way that Canada’s giant “Maple 8” pension plans are backing their own economic transformation after one too many ‘51st State’ comments from their southern neighbor.

When Carney took over in Canada last year, he realized that compelling pensions to buy local would trigger an immediate legal crisis regarding their fiduciary duty to maximize returns.

So, he offered an attractive compromise - the “Major Projects Office”. If pension funds agree to finance domestic critical minerals, ports, and energy projects, the government will provide first-loss capital; eliminate the environmental (and other inter-provincial) bureaucracy; and fast-track the approvals.

It is working. Canadian pension capital is beginning to move and Carney was just in Sydney to make sure the Aussie supers are watching closely. An agreement was signed that will see the Canadian pensions and Aussie supers sharing the load on these massive “nation-building” projects.

Down under, Treasurer Jim Chalmers has come up with his version - the “Single Front Door” for major infrastructure investments. Its ‘Investor Council’ will act as a concierge for institutional superannuation capital. There is money behind it too - hardcoded into the Federal Budget under the “Future Made in Australia” framework.

The final piece of the jigsaw to drop will be a carve-out to the APRA performance benchmarks that will allowing super funds to invest in illiquid domestic infrastructure without regulatory penalty. As I said, there are plenty of shovel-ready projects ready to go.

Beyond celebrating the ruggedizing of the Lucky Country, what’s the angle here for the 🐿️? Pre-revenue ASX junior miners are not really my thing (even if I did include a local Melbourne pre-production gold mine in the ShinyAcorns™ portfolio the other day).

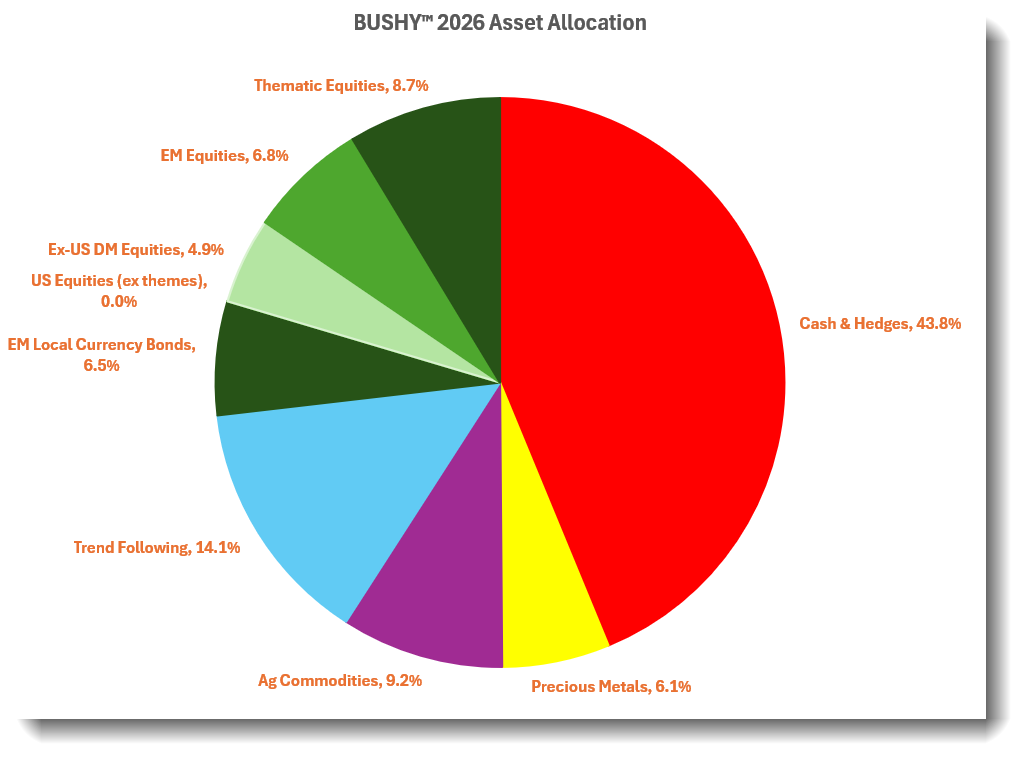

We are entering an era of state-sponsored capital expenditure not seen since the post-WWII boom. If a domestic industrial base is being recreated, there are less risky ways of playing the theme. I have put together a ‘Straya Ruggedization’ basket of 7 stocks that I have a hunch will thrive in this environment.

Details will be in tomorrow’s ‘Start the Week’ note. Yes, I know that usually comes out after the ASX has already traded a session. I will try to accelerate it. In any event, don’t forget that the Strait of Hormuz is still shut and we are therefore still in ‘shopping list’ mode.

As ever, please get in touch if you have any questions.

Squirrel out!

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.

In Aussie, the term “yakka” refers to work, and when combined with “hard,” it emphasizes tough, demanding, or persistent effort - whether it’s manual labor, office work, or studying. The word “yakka” comes from the Yagara Aboriginal language of southern Queensland, where “yaga” meant “to work”.

Good luck with supplies down there.

As we are seeing everywhere in the western world (except Europe it seems) just in case is trumping (no pun intended) just in time.