The Physics of SpaceX

Could Musk run out of buyers? Could the deal break the market? No paywall on this report from the 🐿️ - it is a Public Service Announcement. 2026, Week 20.

Blind Squirrel Macro paid subscriptions are paused until early June. I am unable to accept new paid subscribers until then.

This is a special free edition. In addition, I have removed the paywall on SpaceX material from earlier this year (links at the bottom of the note). Please share this public service announcement far and wide!

The ‘Start the Week’ note will be out for existing paid subscribers on Sunday night or Monday morning EST. Please get in touch if you recently subscribed to my work and are interested in a trial / review of the archive.

The Physics of SpaceX

Well, the SpaceX S-1 finally dropped this week. As you know, the 🐿️ (together with podcasting partner Benny) have been following this one very closely. Even if you (like this rodent) have no intention of placing an order in the IPO, all investors and traders have no choice but to pay attention to the circus.

The latest ‘price talk’ for the deal is that SpaceX is expecting to raise $75bn at a valuation of $1.75trn (more on that later) in mid June. Including the 15% greenshoe, the company’s underwriters will need to place $86.25bn worth of stock. There is no (even vaguely close) historical precedent to such a raise, and I think it will place a huge test on the stability of the US equity market.

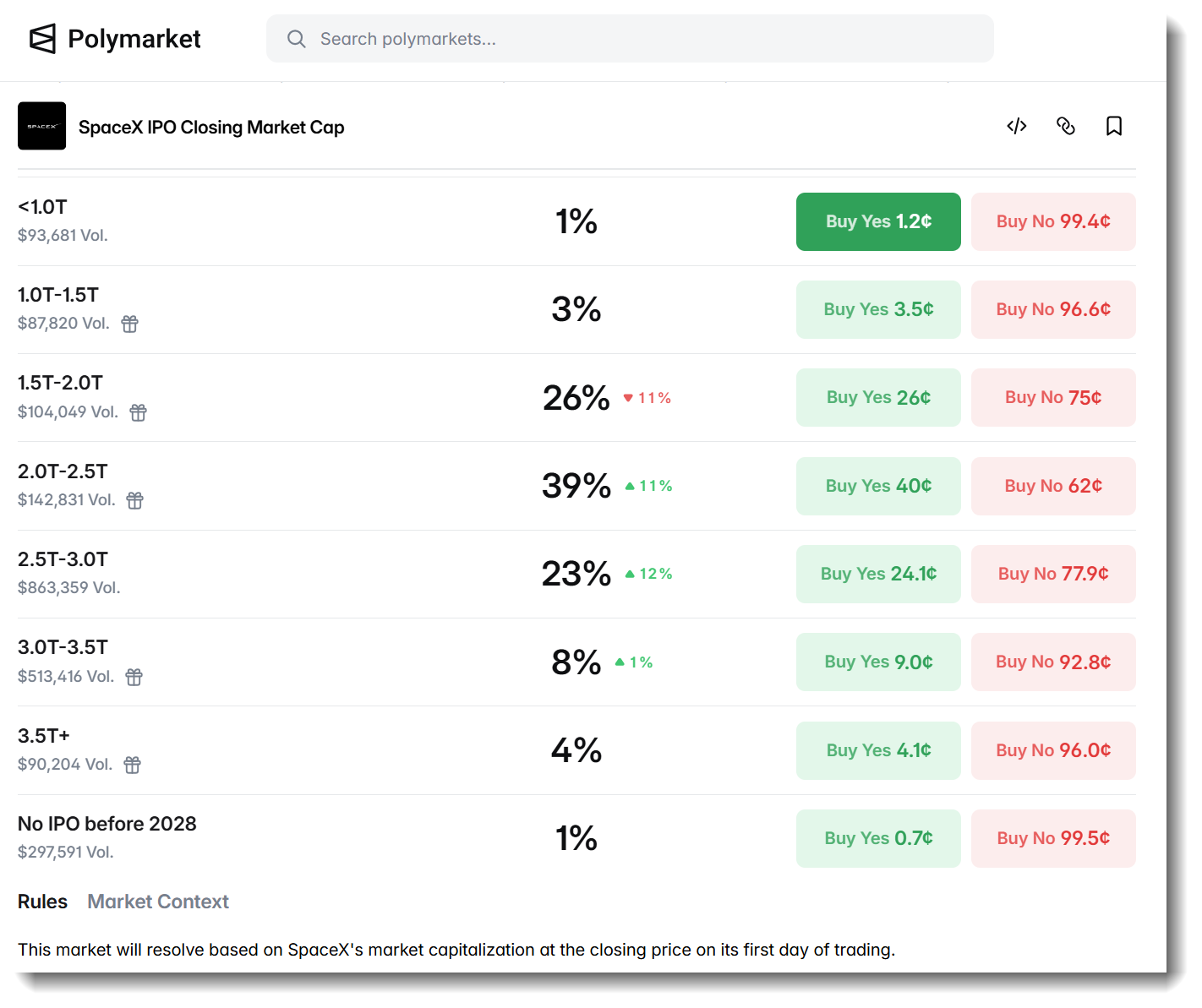

But right now the ducks are quacking - Polymarket odds are pricing a 74% probability of an end of listing day market capitalization for SpaceX in excess of $2trn.

And if the SpaceX common stock is insufficiently racy for you, the ETF Sponsor community has already filed some completely degenerate alternatives for you. I imagine that listed weekly options will be also on the menu within days of listing.

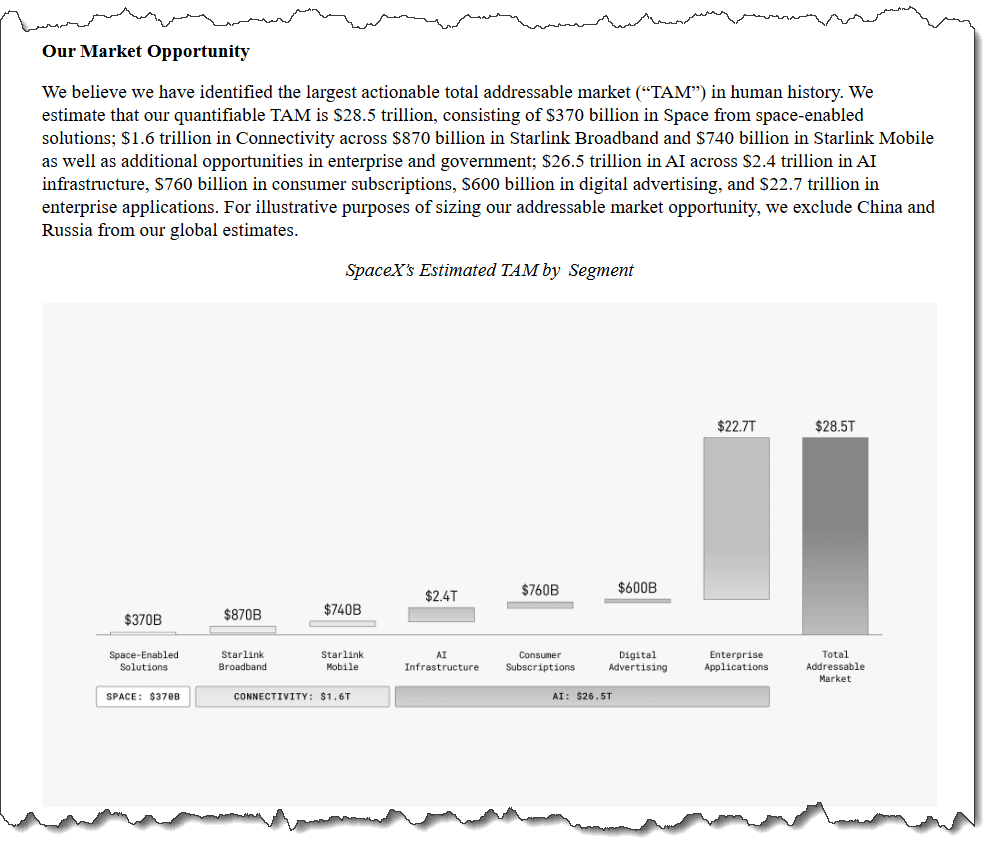

Once you have browsed through the glossy rocket photos and voluminous risk factors of the SpaceX S-1, you soon stumble upon the document’s ‘money shot’ - almost 80% of SpaceX’s TAM has nothing to do with rockets or satellite broadband subscriptions!

Most of “the largest total addressable market in human history” is AI Enterprise Applications. The largest estimates of AI Enterprise Applications 2030 TAMs that I have been able to find online range from $50-300 billion. I guess that the inclusion of Mars more than makes up for the exclusion of China and Russia…

Has everyone lost their minds?

Close your Eyes and Ears

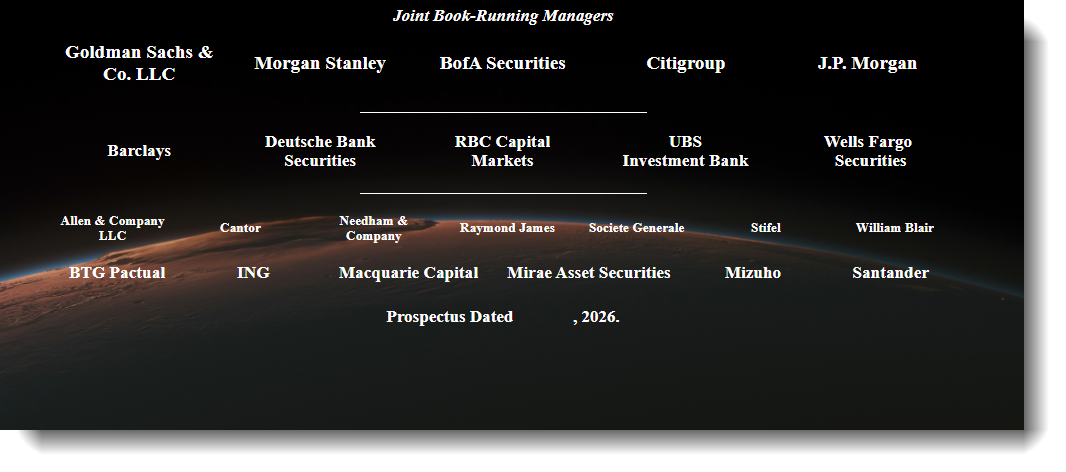

You are currently being submitted to a continuous barrage of propaganda. You must tune out CNBC BubbleVision (“Rockets!, Mars!, wow!”)! SpaceX has also co-opted the entirety of Wall Street. The assembled syndicate below is probably looking at a fee pool of $850m, assuming a (well below market and yet to be confirmed) underwriting commission of 1%.

That number buys a ton of cheerleading (top tip - keep an eye out on Jefferies - they have a highly-ranked and now un-gagged Aerospace & Defense analyst and were not included as an underwriter).

Next, please please please ignore these 👇clowns - I have engaged (🙏 Jason) a full-time stunt double to listen to (and summarize the bullshit contained therein) the insufferable All-In podcast each week.

The Silicon Valley and Midtown Manhattan ‘bros’ are already very very very long SpaceX. Their (extremely vocal) participation in the IPO will be performative only - aka a modest ‘averaging up’ of the basis of their existing exposure.

Bottom line: if you are considering buying stock at a $1.75 trillion valuation, you have absolutely no business listening to the ‘objective’ 😉 cheerleading of those that bought in at less than 10% of that number. Fade the noise! I implore you.

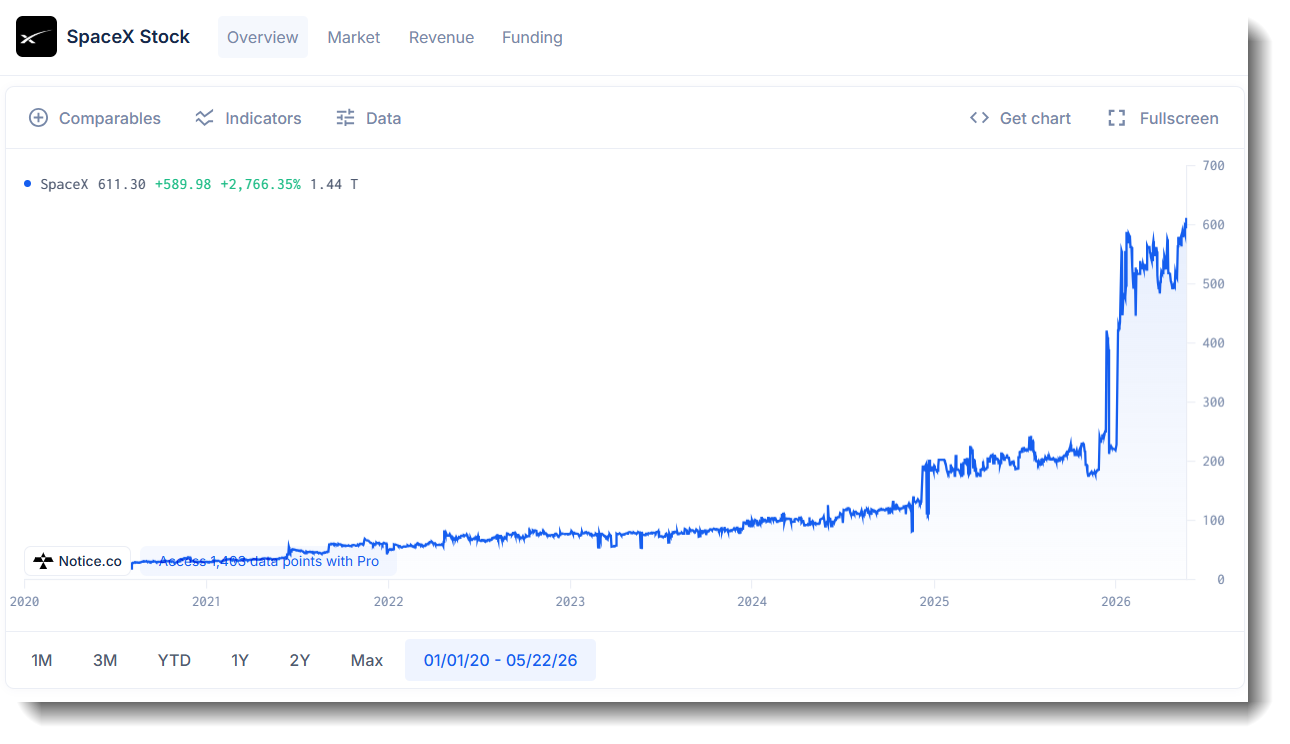

Below sets out the abbreviated SpaceX fundraising history. Elementary grade math will tell you that the basis of majority of the SpaceX cap table is in the trade at less than 5% of the current ‘price talk’ valuation.

These investors - who have collectively put in less than $11bn of equity (versus $2trn of proposed market cap) into SpaceX - will be all over the TV and podcast circuit over the next few weeks encouraging you to embrace their bags.

Even if these insiders tell you that they are ‘topping up’ their position in the IPO (and they will be very vocal), I would humbly suggest that you fade them hard!

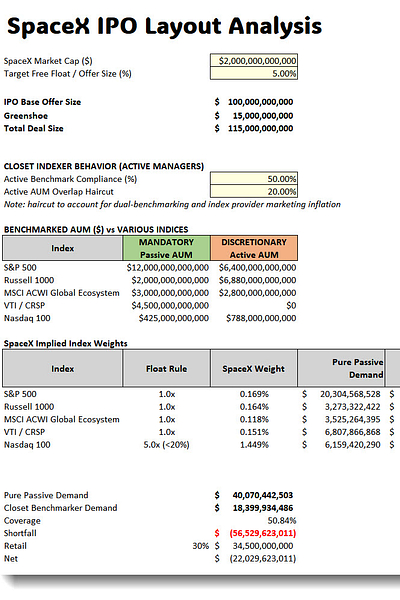

Does the layout math math?

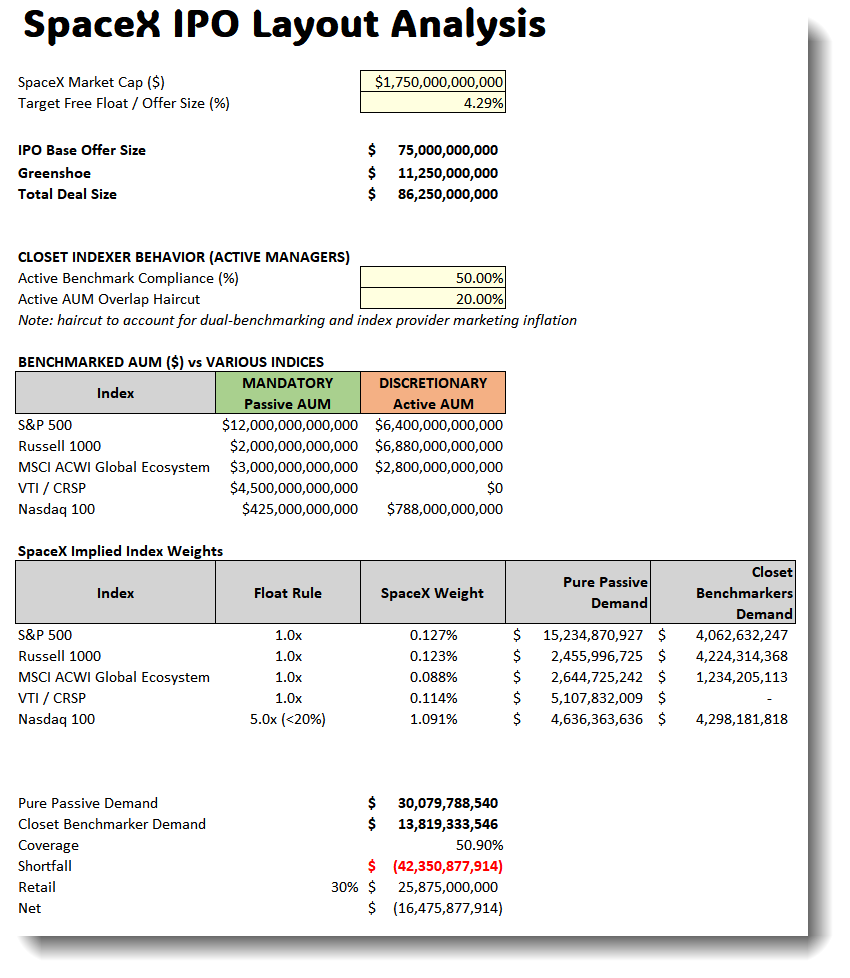

I am revisiting my SpaceX IPO layout model from April.

The index committees have - as Benny and I feared - also been co-opted by ‘Team Elon’. SpaceX will enter every major benchmark index at the earliest possible opportunity. Nasdaq - with its 5x free float multiplier rule - is particularly egregious. But does it really make a difference?

On current price talk, let’s assume (a very long putt) the following. Musk manages to:

capture 100% ($30bn) of the captive index demand for the offering (more on the mechanics of this below)

enfranchise 50% of the demand from active managers that ‘closet benchmark’ the major indices

find a home for 30% of the deal ($26bn) with retail investors - a staggering absolute number to raise from this cohort (I remember the days when a 5% allocation to retail was considered aggressive)

Assume all of the above and Musk still needs to find another $16.5bn of demand just to get the deal to 1x covered.

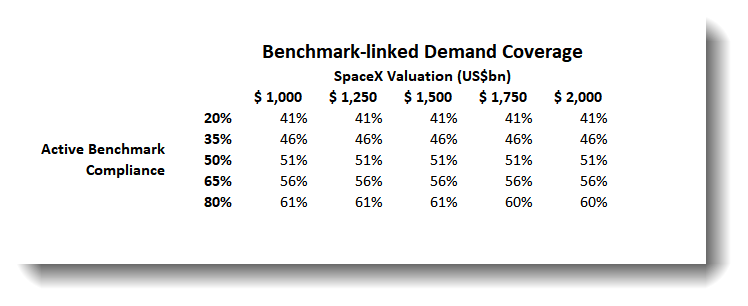

Have a play with the numbers yourself 👇:

Even if you toggle for the IPO valuation and the ‘compliance’ of closet benchmarkers Musk’s bankers are still left short of allocable demand to the tune of 40-50% of deal size.

Who plugs that hole when anyone that is anyone (sovereign wealth funds, hedge funds, family offices) has already been shown the deal on multiple occasions over the past 10 years AT A FRACTION OF THE VALUATION CURRENTLY BEING CONTEMPLATED? I spent 25 years of my life taking companies public around the world - color this 🐿️ skeptical…

The Hedge Fund Passive Warehouse Trade

Let’s return to that $30bn of demand from the passive index funds. Guess what? The likes of Vanguard, State Street, Blackrock and even Invesco (asset of manager of QQQ 0.00%↑) are not putting orders into the IPO order book. They cannot buy SpaceX until the day that the company is admitted into the various indices they track.

The idea is that hedge funds will step in to act as temporary liquidity providers, anticipating that they can sell the stock at a premium to the index buyers (SPY 0.00%↑ QQQ 0.00%↑ VOO 0.00%↑ et al ) shortly after listing.

In theory, the execution of this strategy would look like this:

Hedge funds bid for large allocations in the IPO order book. To fund these massive purchases without blowing up their prime brokers’ balance sheets (under Basel III) capital requirements, they will lean on synthetic leverage via swaps.

Because warehousing billions of dollars of SpaceX stock exposes the hedge funds to broader market drawdowns, they will likely also need to hedge (via S&P 500 or Nasdaq futures).

As the fast-tracked index inclusion dates arrive, the funds will sell their warehoused shares to the passive funds - hopefully at a markup.

The problem is that if these hedge funds misjudge the timing or if passive demand is weaker than modeled, they could be caught holding massive, highly leveraged positions in an illiquid market. It also does not help when most of your peers have the same trade on.

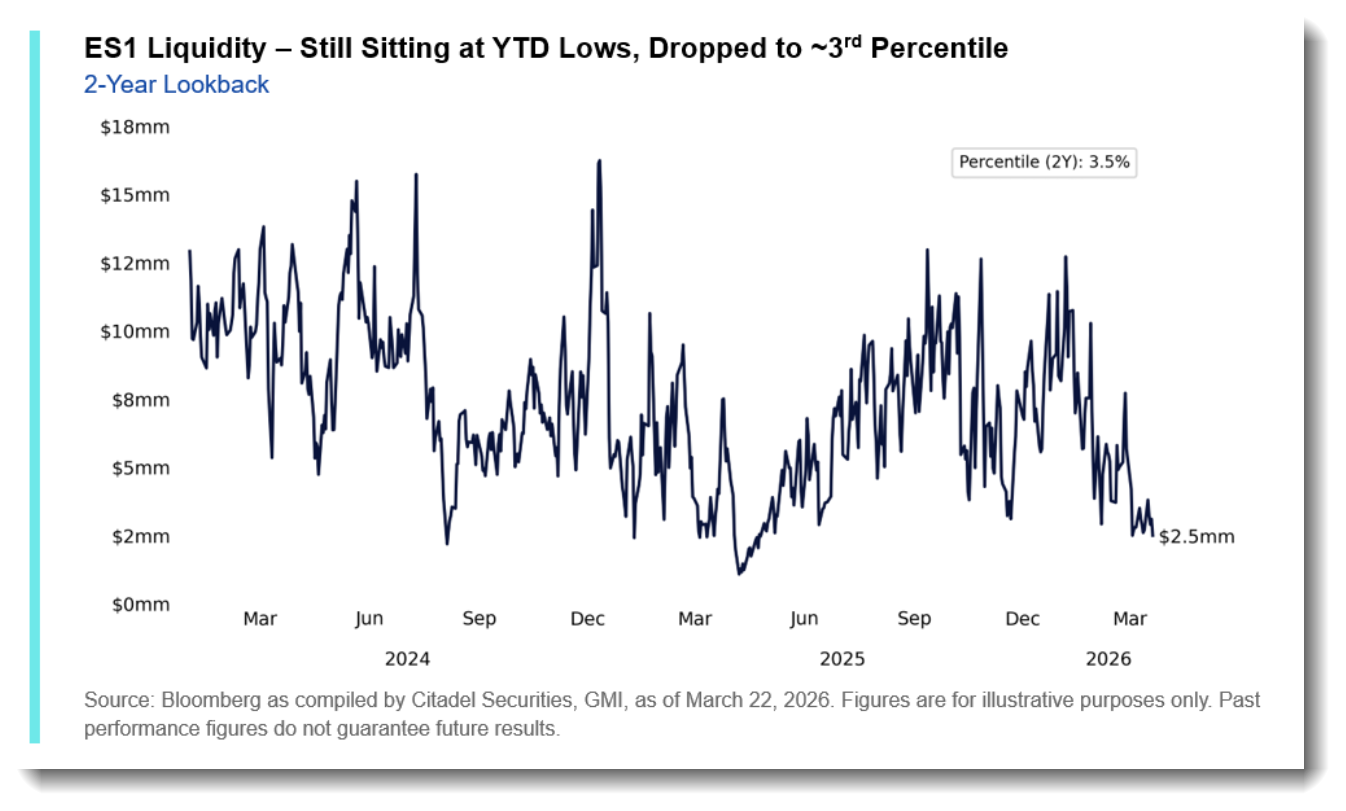

Top-of-Book Liquidity Constraints

Then there is a ‘making room’ problem that faces the broader market.

As passive investors and closet benchmarkers mechanically sell roughly $44 billion of existing holdings to fund their SpaceX bids, they will execute against a market where “top-of-book” liquidity (the ability to transfer risk quickly at the current bid/ask spread) is severely depleted.

These days, investors can transact far less capital ‘at the touch’ without moving prices. Large, directional and simultaneous sell orders across passive players will shred through this thin liquidity. Traders will be forced into deeper layers of the order book where liquidity is even thinner. Wider bid-ask spreads, increased transaction costs, and heightened volatility comes to the broader market.

At the single stock level - even for the giants of the Mag7 - top of book liquidity is even thinner as well as heavily fragmented across dozens of different exchanges and dark pools. During periods of stress, algorithmic market makers will likely pull their quotes - individual name liquidity could evaporate.

On the face of it, $44bn does not sound like a great of money. However, students of friend of the podcast Michael W. Green will know that there is a price impact multiplier effect to consider. According to his most recent work, this amount of selling could feel $1 trillion of price impact. Do check out our conversation from January.

Does making room for SpaceX deliver a ‘double tap’ to the forehead of an already fragile and top heavy S&P? It has to be a possibility, but nobody is discussing this.

And it’s not just Day 1

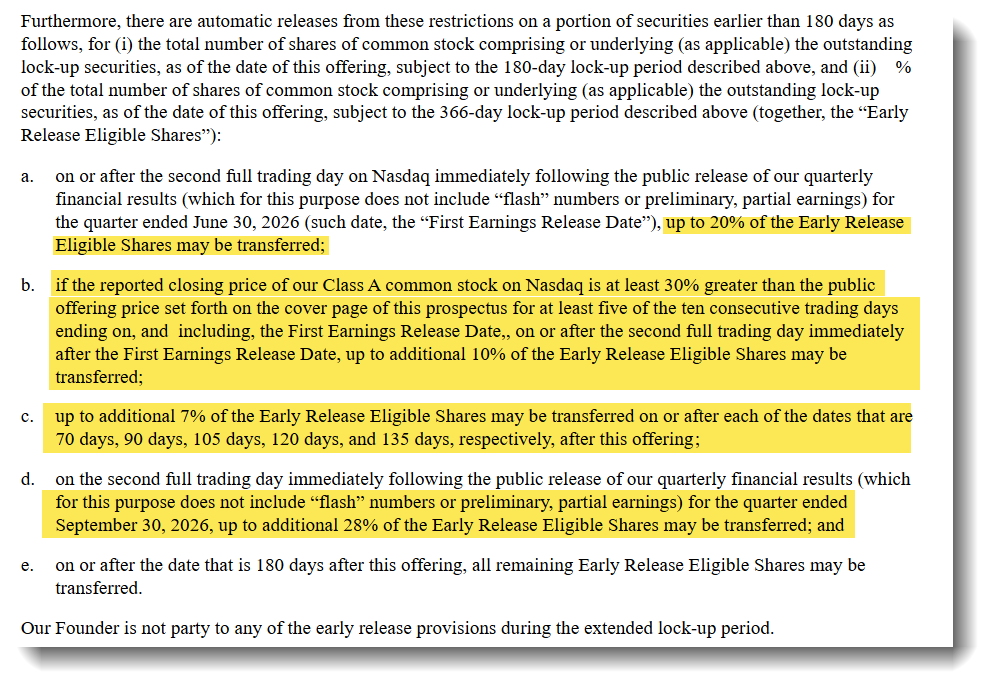

Assuming that the $86.25bn gets successfully allocated, the market absorption is still not done. A wall of supply is coming from those insiders that bought SpaceX at a fraction of the price.

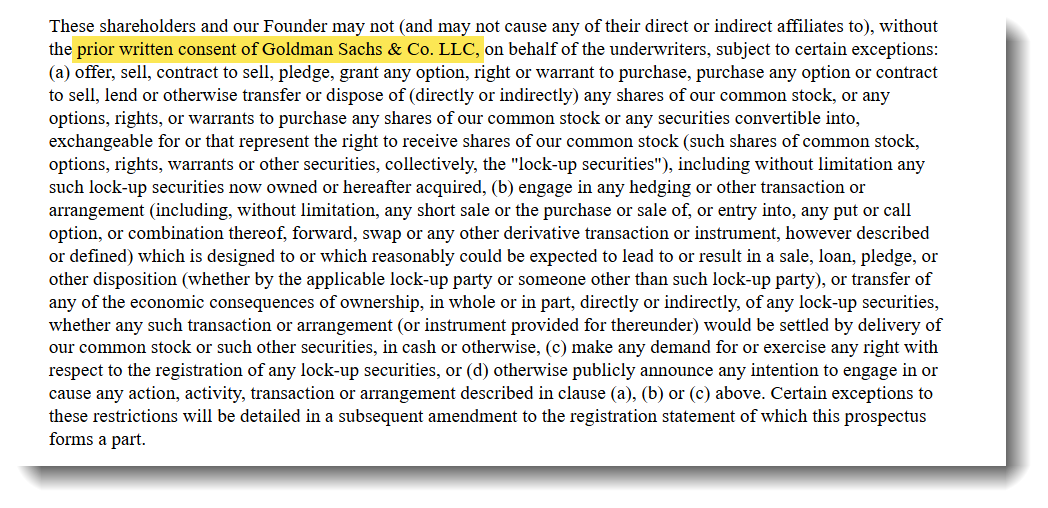

The S-1 makes clear that Musk (approximately 42% economic interest - with 85% of voting power via super-voting Class B shares) is subject to a normal lock-up but a lot of SpaceX insider stock joins the free float remarkably quickly.

“Early Release Eligible Shares” have not been quantified in the draft S-1 but the lock-up schedule and triggers are set out below and I have seen estimates that 80-90% of the non-Founder shares will be freely tradeable by November:

SpaceX insider stock supply risks becoming a drag on the S&P equity supply / demand equilibrium for many months to come, just as 401k flows and hyper-scaler buybacks slow down as AI capex sucks the life out of most of the real economy.

Will it Even Happen?

Back in April, Benny and I were skeptical whether the IPO would happen at all. We were wary of the obvious trade which would have been to short Tesla in the run-up to the SpaceX IPO as the Musk acolytes sold their shares to fund the switch into more direct play on the Muskonomy.

The eventual combination of SpaceX with Tesla seems inevitable. What if the challenge of finding a home for $86.25bn of stock laid out above turns out to be beyond the skills of the greatest stock promoter in human history?

The obvious ‘Plan B’ would be to reverse SpaceX into Musk’s existing listed vehicle. RIP the Tesla shorts if that happened! Back in early April the odds of a merger announcement by June 30th were priced at 5%. They are now at 1%.

Indulge the 🐿️ in a bit of wild speculation. Many column inches last week were devoted to the appointment of Goldman Sachs as ‘lead left’ on the IPO. This included a fun piece from my pal Craig Coben in the FT (linked below). Craig, a former Global Head of ECM at BAML, will be joining Benny and me on the podcast in early June.

All it took for GS to displace Musk’s traditional bankers at Morgan Stanley apparently was for David ‘DJ Sol’ Solomon to slide in to Musk’s DM’s on Twitter. Really?

The 🐿️ had a front row seat to the intense rivalry in Equity Capital Markets between GS and MS. It was a blood match. To lose any deal was bad enough. To lose it to Morgan Stanley was a cardinal sin!

MS banker Michael Grimes staked his reputation (and a great deal of firm capital) financing Musk’s buyout of Twitter. He even followed Musk into government for a while. Surely the top slot in the ultimate Muskonomy mandate was nailed on for Mr. Grimes?

What if Musk has done the same demand math as the 🐿️ and really wanted to keep Grimes focused on his job as lead M&A advisor on ‘Plan B’?

Perhaps this theory is a bit ‘tin foil hat’ but 100:1 odds on Polymarket for an emergency ‘shotgun’ Tesla/SpaceX marriage by the end of June do not look like a crazy flutter. Frankly probably better EV than buying SpaceX at a $1.75 trillion valuation. Just a thought. You have been warned.

Benny & The Squirrel Out!

****Bonus Extras

I have released all of the work that Benny & I have done on this situation from behind the paywall. This includes the full April note and podcast as well as the latest full valuation model that we created with Manus and which agreed with our April assessment.

Spaced Out!

Happy Easter to all who celebrate. This weekend’s note is a Benny & The Squirrel collaboration! We preview the jumbo SpaceX IPO. The two of us have moved a decent amount of primary paper between us over our careers. And this one is a doozy!

If you are a free subscriber and cannot wait for June to subscribe and get access to the paid content, send me a note and we will see what we can do about a trial.

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.