The Greater Bay Life Straddle

Two Eastern savings giants with no obvious Apollo/Athene-style balance sheet engineering. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 17 of 2026.

The topic for this week’s note has been gurgling around at the back of the 🐿️’s mind for quite some time. My Hormuz Crisis-enforced buyer’s strike has given me time to think about how to re-position my China / Asia equities book when the time comes to add back risk.

My China coverage in the past 2 years has focused mainly on the topics of consumption and technology. Very little ink has been spilled on the sector that has frankly powered a significant portion of my returns from the region with only a passing mention - financials.

One of my favorite fun facts is that Chinese State-owned banks are responsible for over 25% of total returns in the past 2 years for DVYE 0.00%↑ (EM High Dividend ETF) that has been one of the larger building blocks of my BUSHY™ beta portfolio for the past 3 years.

The ‘Big 6’ Chinese banks and ‘Big 5’ insurers have returned more than 2x the MSCI China since the beginning of 2024. It’s not all about catching the rips in Alibaba BABA 0.00%↑.

Yet it has felt much more appealing to write about baijiu innovators and Labubu dolls. This is wildly ironic for me given how significant the role of the financials (over 60% of my deal flow) was during the last 10 years of my investment banking career. I guess that’s the old PTSD kicking in again…

I mentioned back in January that the IPO of AIA was one of the first deals that I worked on upon returning to Hong Kong in 2010. The life insurer went on to compound like a complete beast for the next decade. A ‘one decision stock’ for any Asia-Pacific portfolio manager.

For someone that has been bullish on Chinese stocks since late 2023, I am kicking myself that it was not right at the top of my shopping list at HK$45 per share in early 2024.

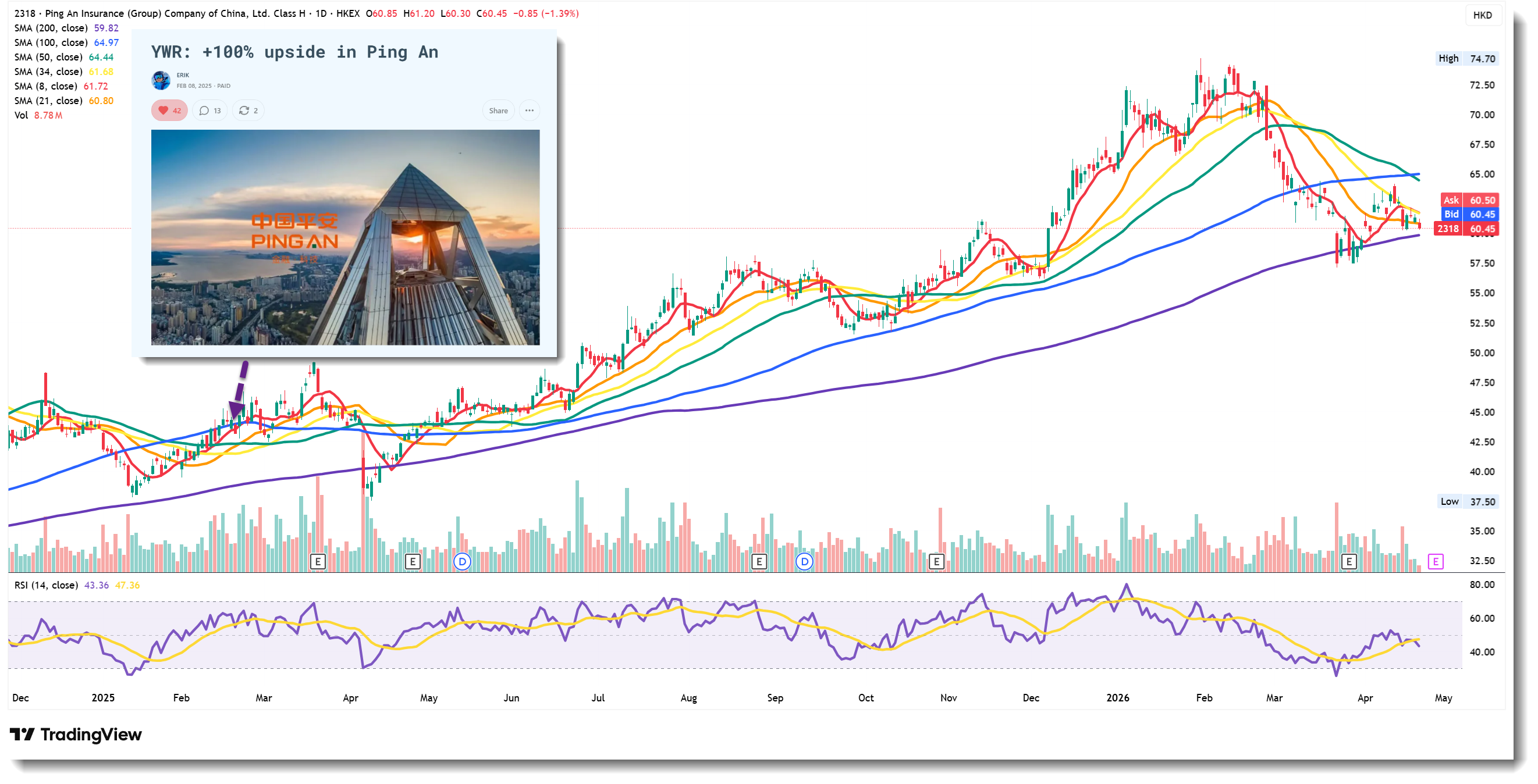

Then last year in February, my pal (and excellent financials analyst) Erik wrote a great note on Ping An Group “YWR - +100% upside in Ping An”. I was super familiar with Ping An and loved his pitch. My reaction however was to pester Erik about my strategic vision for its founder, Peter Ma (more on that later). This foolish rodent should have just bought the stock!

More on that later. I suspect that there has been a subliminal reason that I have not given much thought to these businesses. But why the hesitation? Because life insurers sit at the epicenter of my deep macro fears regarding the private credit market.

Over past decade, the Western life insurance industry has been hijacked by private equity. To manufacture yield, the sector’s balance sheets have been stuffed with private credit paper and levered CLOs. As the cycle starts to crack, Western insurance books look vulnerable.

Benny and I talked about this on Thursday evening - the link below will take you to the relevant segment.

Also, if you are not among the 104,000 viewers that have already seen it, take a moment to watch Steve Eisman explore how regulatory arbitrage is allowing ‘Team Saddlebags’ - having run out of capacity with the pension funds and endowments -to offload paper into captive insurer vehicles. Should be mandatory viewing for anyone that owns a life insurance policy or an annuity.

Most Asian lifers have limited need to engineer yield via private credit (with the possible exception of those crazy Taiwanese lifers)1. Their growth comes from pure demographics, and they have the ability to match their long-duration liabilities with traditional financial assets.

The Great Forced Migration of Household Savings