The Crooked Smile

Time to talk about the US Dollar - we have a lot riding on it. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 25 of 2026.

Quick reminder that the cost of annual subscriptions will be rising from $360 to $450 at the end of June (next week!). Monthly subscriptions will remain at $45. As ever, all existing subscribers are grandfathered at their original rates.

I know that Ray told Tammy in the final scene of The Firm that he loved “her crooked little mouth” but allow the 🐿️ a tiny bit of poetic license…

Right now, Stephen Jen’s “dollar smile” is looking decidedly crooked after Kevin Warsh’s debut press conference violently yanked up the right side of Holly Hunter’s second best “feature”.

For those in need of a quick refresher, the “dollar smile” model dictates that the greenback strengthens in two scenarios: global panics (the left side) and periods of US economic exceptionalism (the right side). Between them lies the dollar trough, where the assets this rodent likes most tend to flourish.

We were supposed to be sliding comfortably into that trough. Instead, Warsh’s 130-word hawkish ‘pivot’ last Wednesday has seen a kink in that smile emerge.

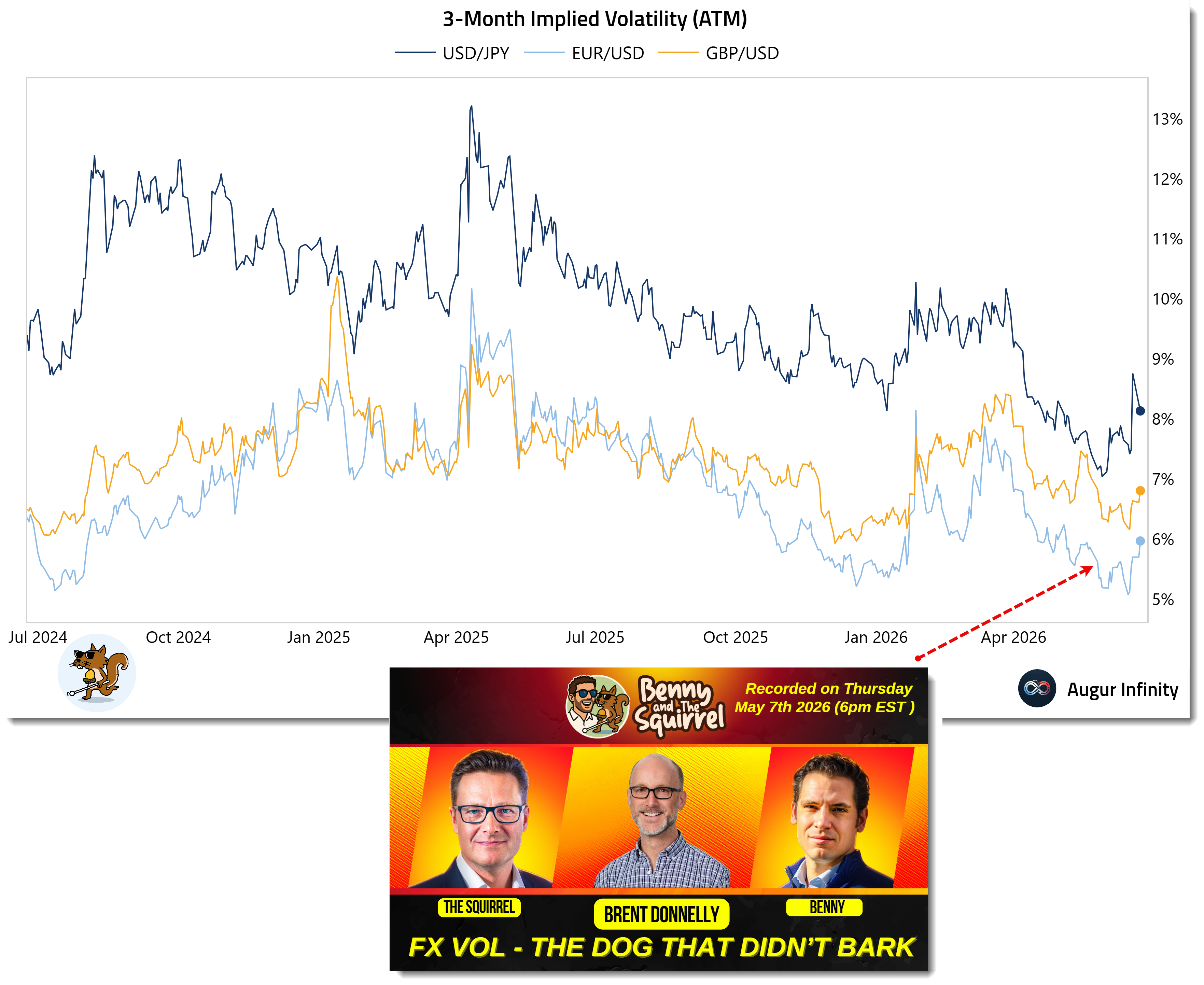

Kevin Muir warned me that the ‘Market Gods’ would have something to say about the title to the early May ‘Benny & The Squirrel’ conversation with Brent Donnelly:

Will the removal of the crutch of Fed forward guidance finally breathe some life into the sleepy world of FX volatility? Well, it’s a start. Actually, I think seeing the back of the Fed hand-holding will put a lid on positioning extremes by market participants that I see as the dry tinder for the next risk deleveraging unwind.

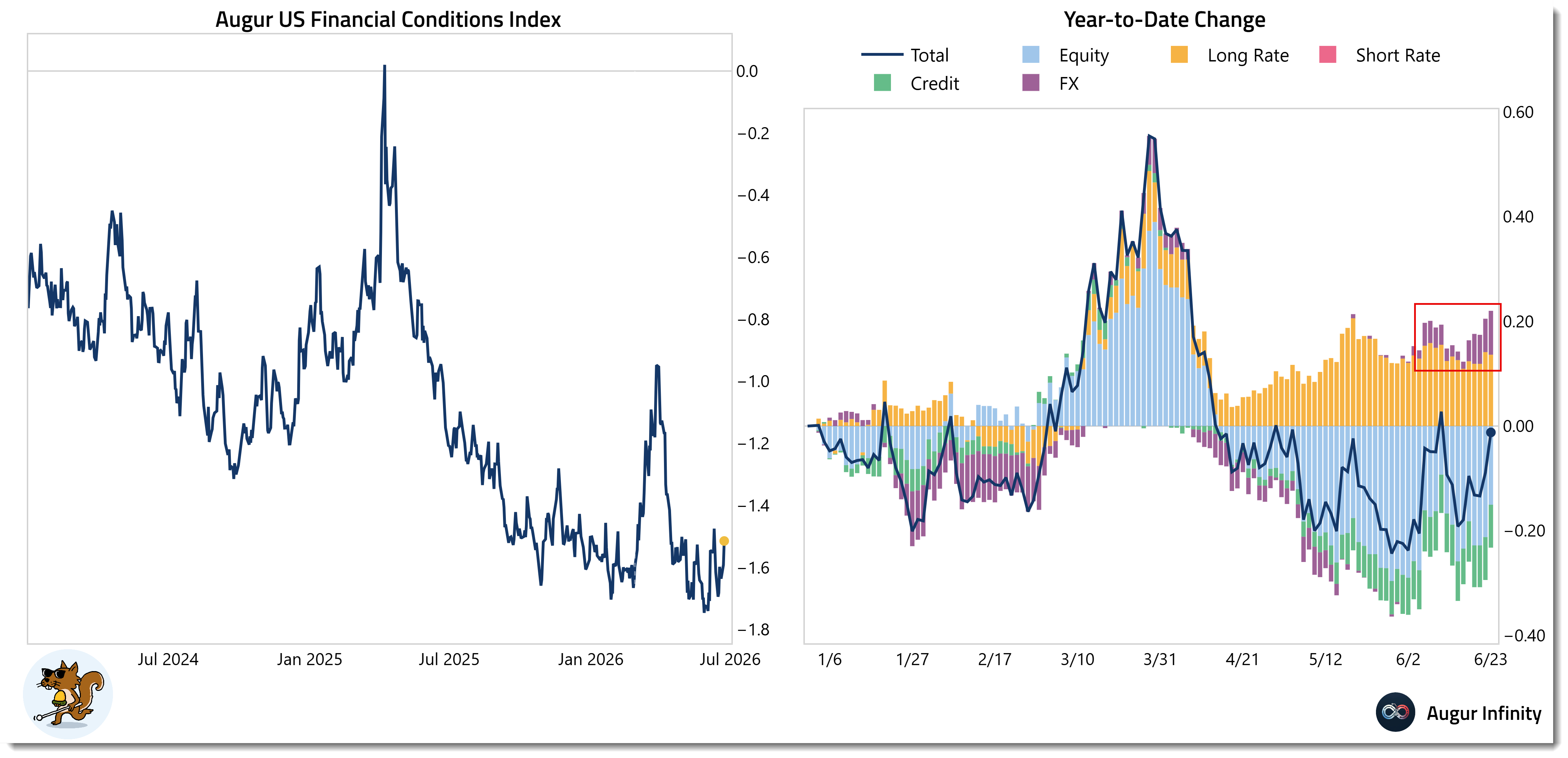

Renewed FX vol has certainly done much of the heavy lifting in terms of the recent tightening of US financial conditions (red box below).

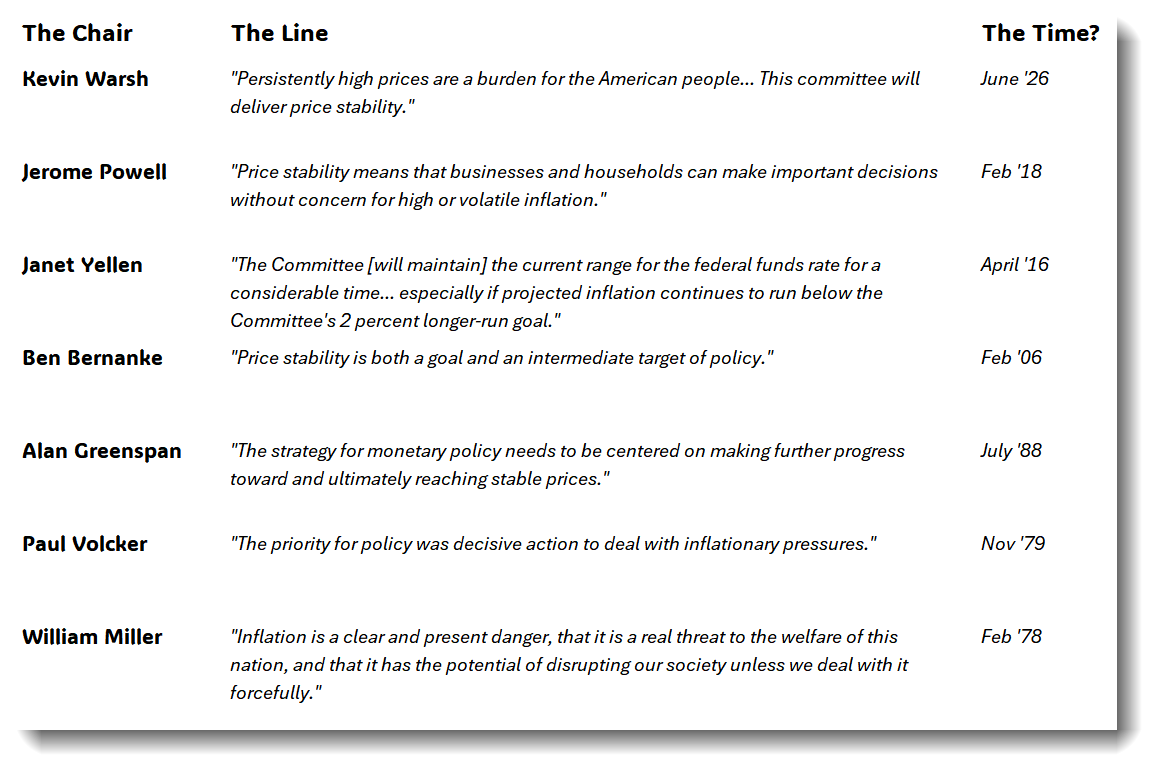

But what should we make of this collective narrative pivot around Warsh from the ‘Trump Administration water boy’ to ‘the next Paul Volcker’ that has become a staple of financial commentary over the past week?

To be honest, what did you expect? Warsh only said pretty much exactly what every Fed Chair has proclaimed upon taking office since this rodent was in short trousers.

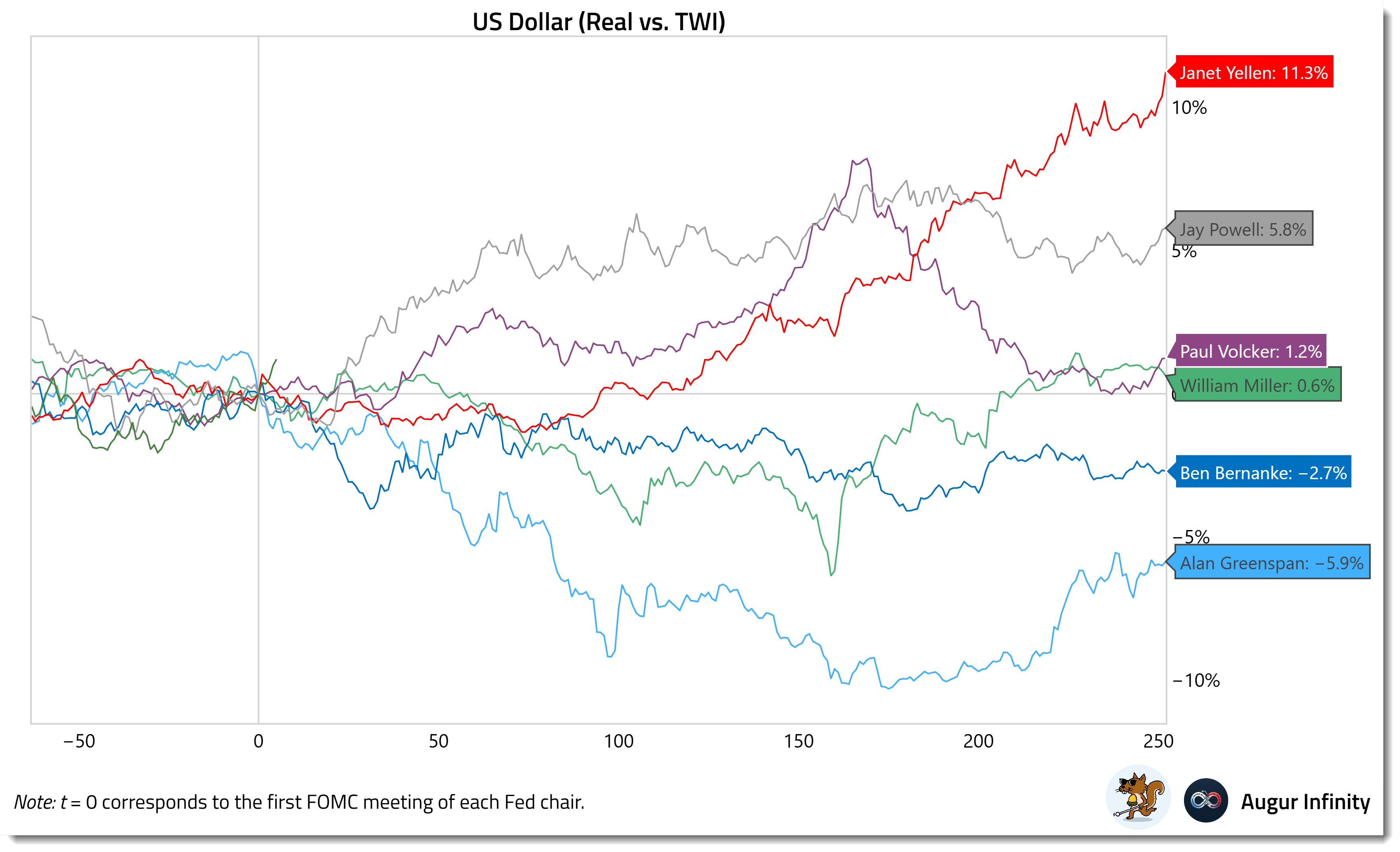

Fun fact: Paul Volcker’s first year (‘79/’80) saw roughly 7 percentage points added to the Fed Funds rate. He certainly followed through! This eventually prompted the dollar to move - soon to be reversed aggressively.

This is what that looks like alongside the famous cigar chomper’s successors:

Even if following the traditional script, Warsh’s words were enough to blast the dollar out of the ‘2 big figure’ trading range that has existed since ‘Liberation Week’ last year.

My guess is that markets were primed for Trump’s pick to offer at least something to the doves and position a Fed willing to follow the established pattern of “looking through” any transitory impact on prices related to the Iran war.

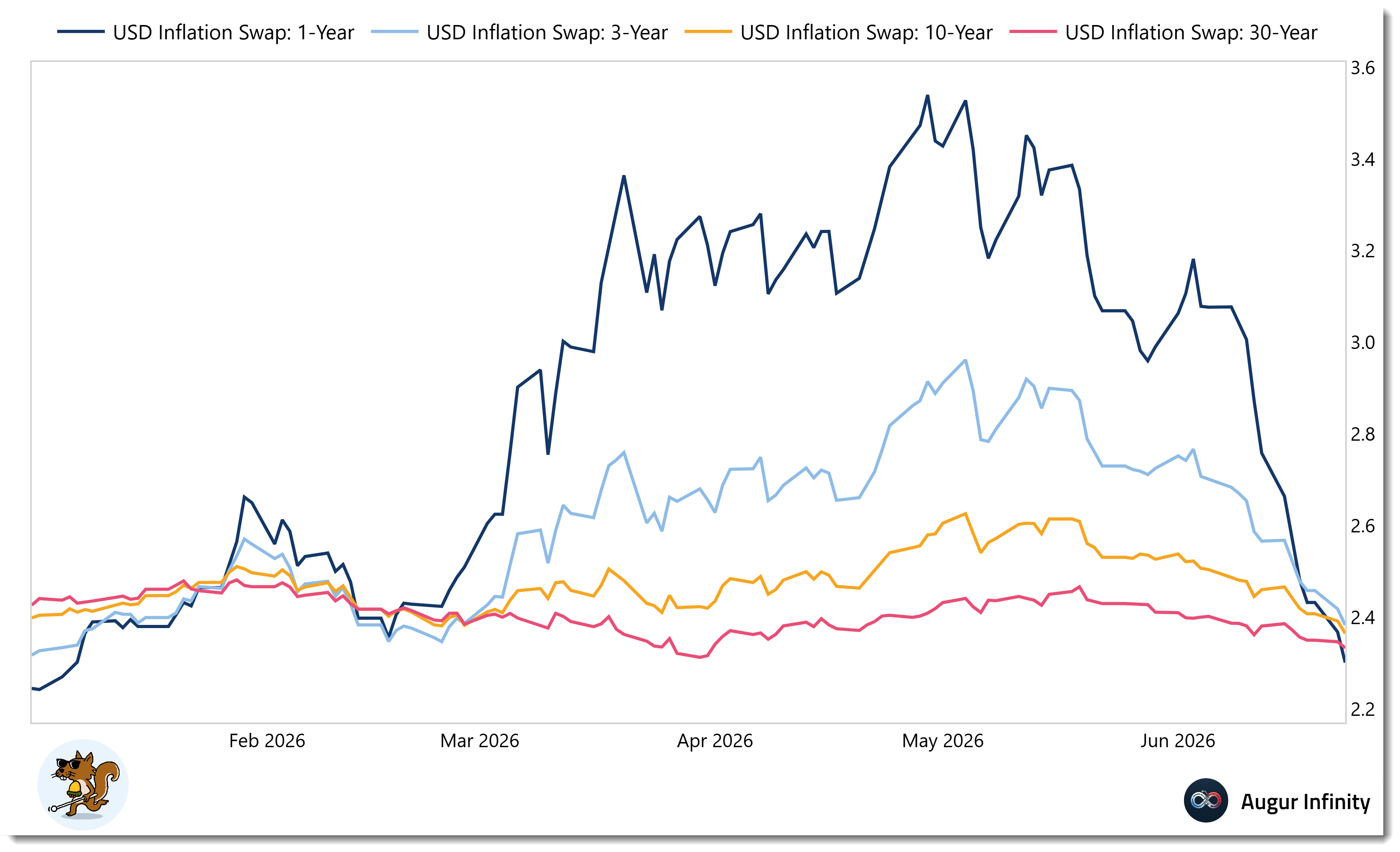

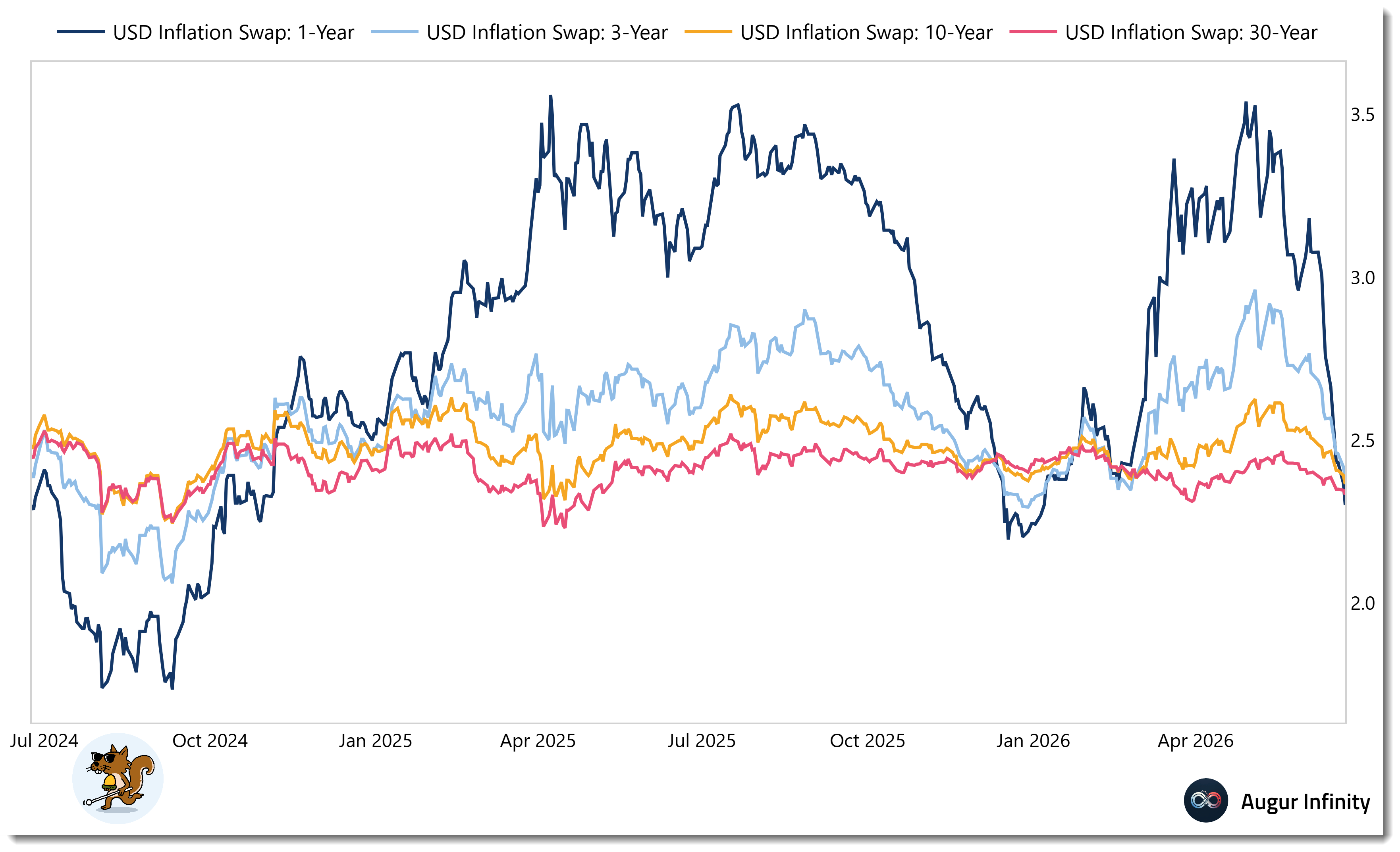

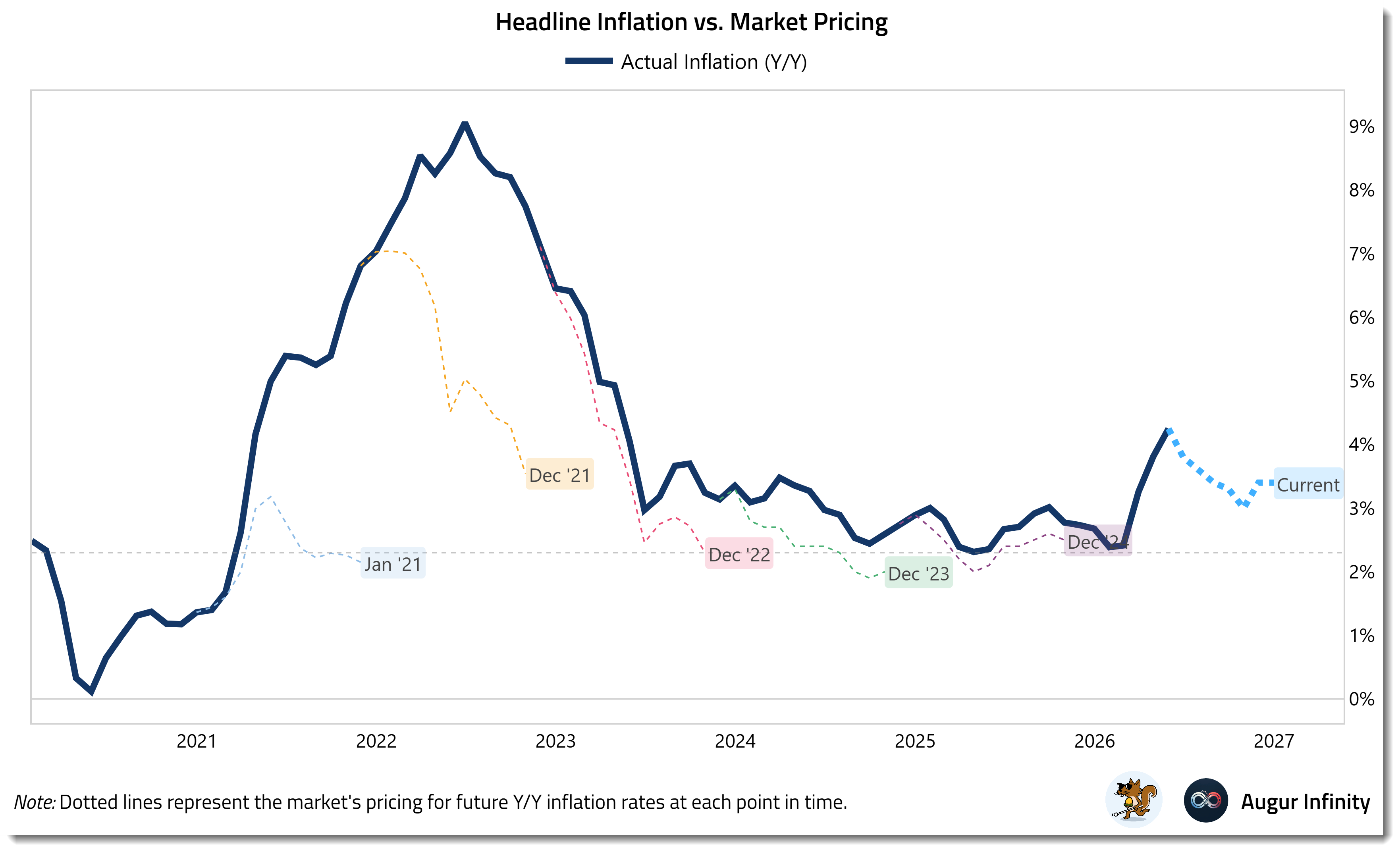

Well, Kev’s bold rhetoric has certainly been effective at curbing inflation expectations:

Which are now at close to their lowest point (across the curve) since the Trump Administration took off.

Even if cynics might possibly argue against the predictive properties of the inflation swap market.

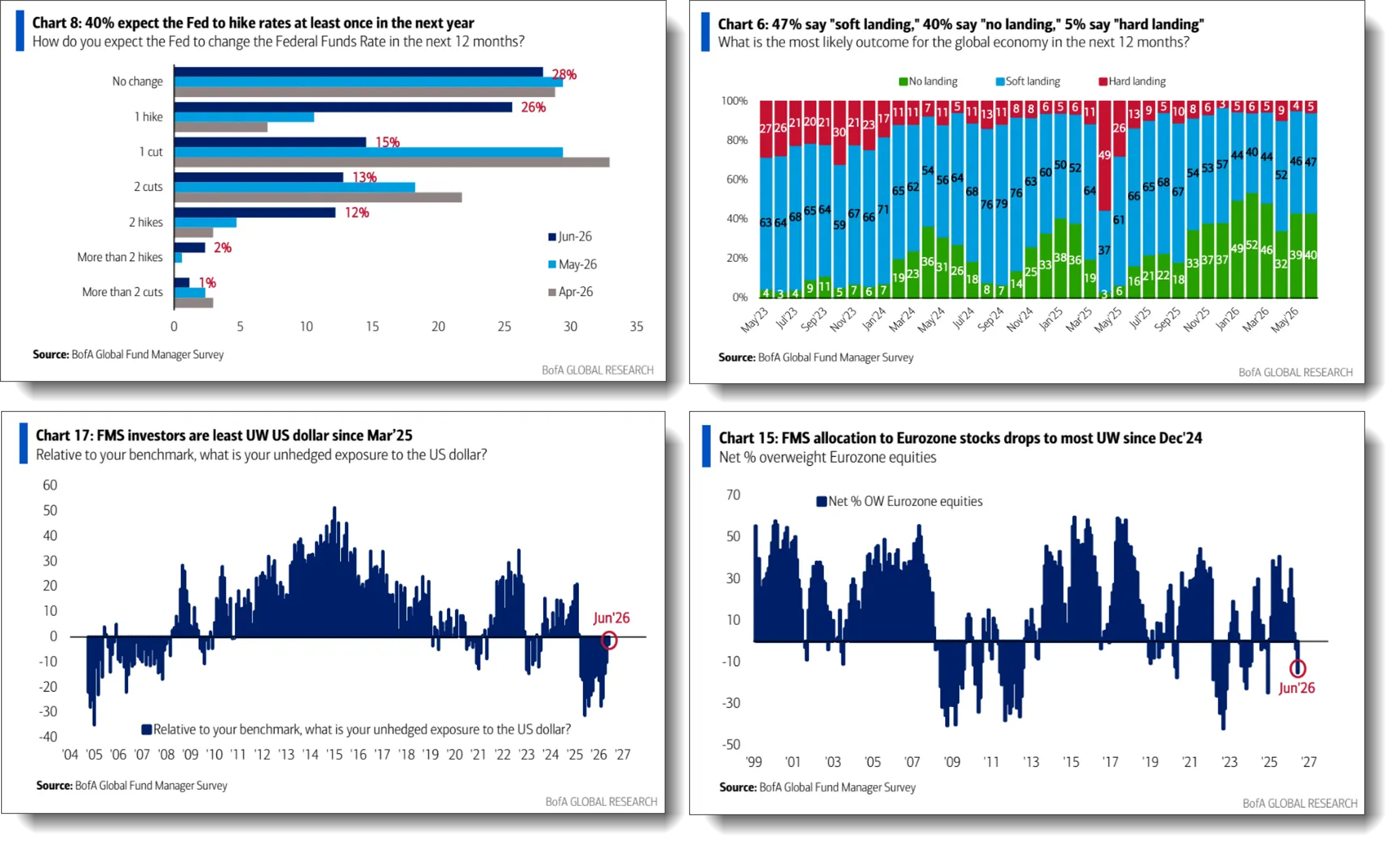

The latest BofA FMS also points to the effectiveness of Warsh’s words in terms of getting money managers to (i) take the hike risk seriously (without scaring off expectations for a ‘soft’ or ‘no’ economic landing scenarios); (ii) reel in the US dollar underweights from their 2025 extremes; and (iii) pare back their “foolish” (not my view, obviously!) recent experimentation with overseas stocks.

The move was certainly enough to finally shake this rodent out of his long duration fixed income hedge (PFIX 0.00%↑) at the beginning of the week.

It was a good entry in April but I should have taken the hedge off when I started adding my Brent crude oil BNO 0.00%↑ position at the beginning of June, as it is - to a certain extent - a similar bet. More on rates strategy and hedges at the end of this note.

That Oil Bet and the Dollar

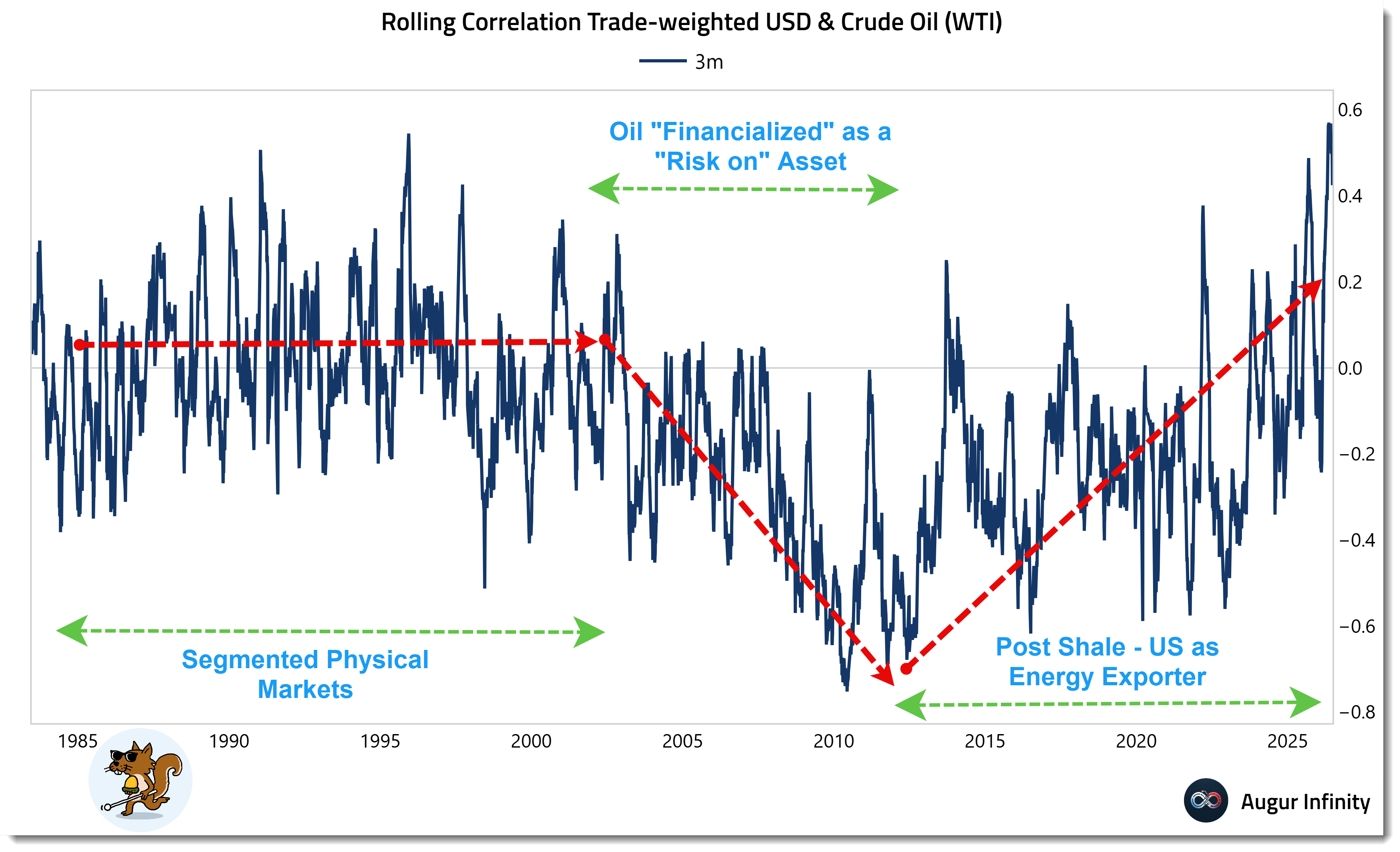

However, what if this dollar move is actually telling us that the barrel counters have a point after all and that energy markets are complacently sleepwalking into a second-round crisis created by a 2-3MMbpd net deficit in crude that has not disappeared?

My base case is that this is an underpriced scenario even without a renewal of tensions in The Gulf - something which (as at Saturday morning Australia - with futures markets shut for the weekend) seems far from settled.

It goes without saying that my P&L in crude is agreeing vocally with those inflation swap traders. No bueno.

The recent move in inflation expectations (at least over shorter timeframes) is certainly implying that my oil call is wrong. But what if it is not just expectation of positive interest rate differentials that lies behind the dollar’s recent tick up?

Over the past 15 years, the post-2000 era in which “financialized” oil (thank you Goldman Sachs!) traded as a “risk on” asset inversely correlated with the dollar has been gradually unwound in a post-Shale world in which the US is a major energy exporter.

Until the barrel counters are proven wrong by a genuine repair of the supply deficit - not just a kink in the dollar smile and a bad week for my P&L - this rodent is sticking with the BNO 0.00%↑ position.

Warsh’s Dilemma

Many old school bond traders were delighted with Warsh’s start and are encouraging him to stick to his hawkish guns.

I agree with Nick (a former Salomon rates trader) on the importance of term yields to the real economy in terms of housing, consumer credit and corporate finance. Indeed, “loss of the long end” has been a recurring concern at the back of my mind for many years.

However, the US financial market is becoming increasingly ‘Australian’. Gerard Minack once quipped that the Reserve Bank of Australia (RBA) is “the most powerful central bank in the world”.

‘Down Under’, the entire economy is linked to the RBA’s “cash rate”. Nearly all mortgage and corporate lending rates are adjusted within hours of a hike or a cut - with an immediate transmission mechanism into the real economy.

Increased exposure to front-end rates has become much more prevalent in the increasingly hyper-levered and hyper-financialized US economy.

As Nick Nemeth noted in his excellent essay (linked below), even members of the very top of the ‘K-shaped’ economy - Wall Street’s well-connected private equity and private credit titans - are now sitting atop a ‘Russian doll’ of compound leverage.

And pretty much all of that leverage is linked to floating interest rates (i.e., SOFR).

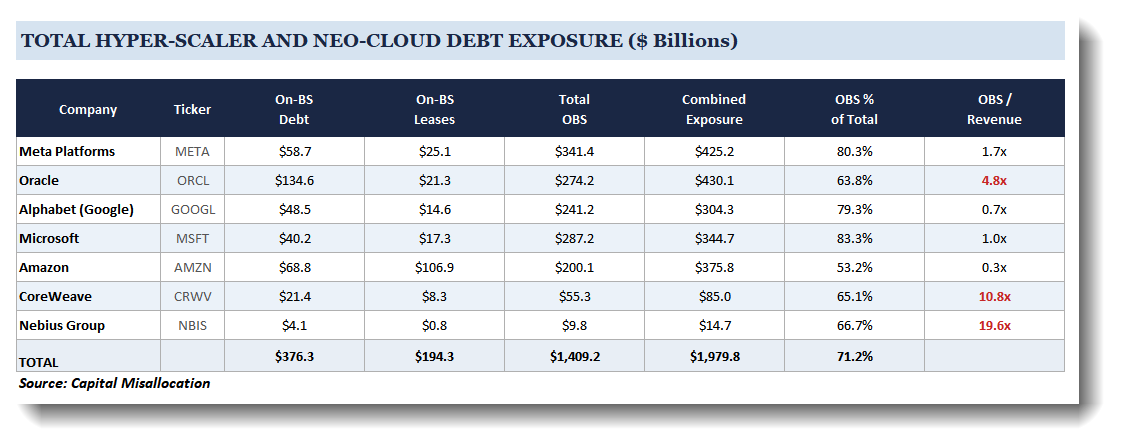

Then we have the engine of the latest wave of ‘American exceptionalism’ in global equities - the AI capex boom driven by the Hyperscalers. The big 7 have already accumulated around $2 trillion of on and off balance sheet debt as part of their data center builds.

Again, these AIDCs are mostly financed at the front of the curve via floating rate debt facilities.

Would it not be ironic if the data center boom that brought us circular (equity for chips / compute) financing to a new level created another circular effect whereby inflation created by all of this investment triggered a rates environment that detonated many of these off balance sheet financing structures.

Broken debt funding markets —> no (or at least much slower) capex —> no more hockey stick charts of token consumption from Goldman —> semiconductors turn out to be cyclical businesses after all (always were!).

While wealthy savers might get a modest pick up on their money market yields, that will not be enough to compensate for the downward marks on their holdings of QQQ 0.00%↑. At that point, US GDP loses both the direct growth from the AI Capex boom and the consumption by the all-important ‘top of the K’ at precisely the same time.

Mr. Warsh is in a bind. And he has a tough fortnight of economic data to navigate. He is going to need every fiber of those sharp suits, the ‘made for TV’ haircut and that winning smile.

I am expecting plenty more fighting talk with respect to the Fed’s price stability mandate in the coming weeks. Talk is cheap - and if it works to calm bond markets, great! On the other hand, the impact of rate hikes may look very different from previous cycles.

What it means for ‘Team 🐿️’