Tape Bomb Refuge

The Blind Squirrel's Monday Morning Notes. Year 3; Edition 4.

Financial exchanges could be a port in a tweet storm.

Tape Bomb Refuge

‘Tape Bomb’ (noun): - A presidential proclamation (on or offline) that sends markets into a tailspin (aka ‘Tweet Tremor’ or ‘Digital Detonation’).

It has been less than a week since the inauguration of Trump and the ‘tape bombs’ have been raining down hard! Last weekend, the 🐿️ suggested that commodity and FX traders might want to lock their buy and sell buttons away in a desk drawer for a few days. With hindsight, that counsel is ageing pretty well!

Monday saw currency traders rush to cover short positions in Canadian Dollars and Mexican Pesos on the revelation that the initial batch of executive orders contained no specificity in relation to tariffs on the US’s northern and southern neighbors, only to get rug pulled faster than a meme coin trader by some off the cuff statements from an impromptu Trump press conference later in the day. Fun times in FX!

When it came to China, the initial trade war vibes appear softer than could have been envisaged during the heat of campaign rhetoric (“60%!” “Immediately!”).

Of course, we all know that this is not the end of the tale. Those with distant memories of the markets of 2018/19 should remind themselves of the volatility that can come to asset markets once ‘tit for tat’ trade measures start hitting the tape on a monthly basis.

The chart below from Goldman makes it pretty clear that tariff headlines can make for a hairy backdrop for risk. As they say, nobody wins in trade wars.

Perhaps ‘nobody’ was too much hyperbole from the 🐿️. The sound of traders clicking buy and sell buttons like one of Dr. John C Lilly’s monkeys in response to each trade-related tweet and utterance is music to the ears of the owners of the world’s financial exchanges. Could exchanges be a refuge from the ‘Tape Bombs’?

The greatest gift to the exchanges is investor repositioning and, even without the trade war speculation, we are already living in a world of constantly see-sawing macroeconomic narratives. The past 2 years has seen interest rate markets re-price the odds of a recession just about every 6 months.

The 🐿️ does not want to enter the debate as to whether or not tariffs are inflationary in their own right or instead just a one-off sales tax that creates higher prices (‘tomato/tomahto!’). Surely those price hikes mess with the all-important (psychological) input - inflation expectations?

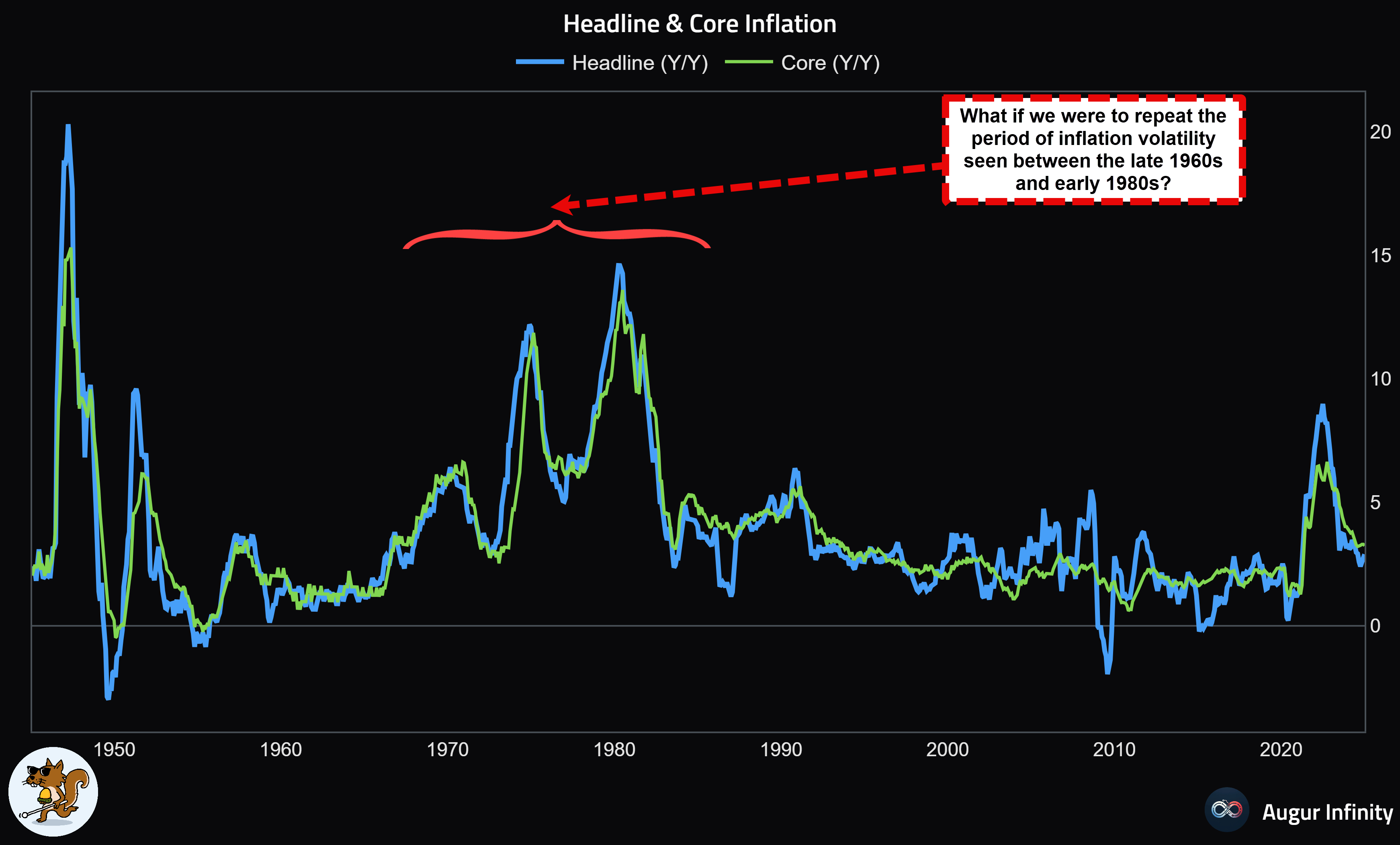

That hot issue aside, your macro rodent is sticking with his core view that we look to be entering a period of inflation volatility (with a lower floor) that could mimic the macro conditions in place when the rodent was wearing short trousers.

Inflation volatility requires more frequent portfolio repositioning. This leads to increased trading volumes in financial assets, leading to higher transaction fees and revenues for exchanges (with negligible increases in fixed costs). Exchanges also typically enjoy strong pricing power that allows them to raise fees to keep pace with inflation.

Liquidity in any financial asset tends to be dominated by a single trading venue. For example, dual listings of equities tend to be implemented for market access, political or governance reasons only. Trading volume always gravitates to one place - where the spreads are tightest. This effect creates almost impenetrable moats for most exchanges.

Market participants are always keen to try to foment competition in the market for financial asset ‘market squares’ in the hope of lowering transaction costs and fees. FMX’s Chairman (Howard Lutnick, the new Secretary for Commerce) is no doubt now well positioned politically but will it be sufficient to break the CME’s stranglehold on US Treasury and SOFR futures volumes?

History suggests that this is unlikely. Here is Mike Dennis, CME’s global head of fixed income, discussing the new competition from FMX in SOFR futures late last year: “It’s still early days but we see our bid-ask spreads are a quarter tick tighter in front month SOFR contracts and almost a half tick tighter as you move out the SOFR curve. As we know, a half tick equates to $12.50 per contract in SOFR futures which dwarfs the size of the transaction fee” [🐿️note: currently $1.25 per side, per contract].

You can, however, understand why Mr. Lutnick thinks that he might have a chance. Exchange monopolies have been successfully broken before. Look no further than NYSE’s loss of US equity dominance with its (effectively forced) demutualization and merger with Goldman Sachs’ Archipelago 20 years ago. This merger created the NYSE Group (now a subsidiary of the Intercontinental Exchange).

Then there is order matching technology such as dark pools, electronic communication networks (ECNs) and alternative trading systems (ATSs) that have enabled the largest customers, with the help of powerful lobby groups, to force changes when they consider the rents to be too high. These days, US equities have over a dozen separate trading venues (usually just a rack of servers in New Jersey).

In response to the assault on their core revenue source (i.e., the business of clipping tolls from trade execution), the exchanges have innovated. The modern battle lines of competition revolve around (pricey) data, new product creation, connectivity and other services.

2 decades on from the disruption in the early 2000s, the major global exchanges have diversified themselves significantly from simple rent collection, adding numerous (and high margin) lines of business.

I cannot tell you how many times in the past couple of years that I have seen charts showing the dominance of US equities as a share of global listed equities. With a market share greater than 70% today (versus 24% of global GDP and 4.2% of global population), it would make sense for any investment in financial exchanges to give thought to international exposure in the mix.

Meanwhile the investment focus of the ‘compounder bros’ has been commanded by SaaS and payments giants - on significantly elevated multiples! The 🐿️ thinks that mid-to-high teens forward EV/EBITDA multiples for the exchanges (basically in line with the S&P 500) compare favorably with where the market currently values those traditional ‘compounders’.

I think exchanges are worthy of a place in the portfolio. In Section Two, the 🐿️ lays out how these quasi-monopolists might fit in. We also provide updates on the BUSHY™ and Acorn portfolios.

Join hundreds of smart investors, market watchers and upstanding citizens by becoming a paid subscriber to Blind Squirrel Macro and receiving the other 65% of 🐿️ content, members’ Discord access (The Drey) and even ‘limited edition’ merch!).