So, you are big in Fintech?

Review of the 🐿️'s BUSHY™ Multi Asset ETF Portfolio and live Acorn trade ideas. 2025, Week 25.

In case you missed it, the weekend note came out early on Sunday morning EST. It contained Part 3 (of 4) of the🐿️’s annual ‘Acorn’ stock take. For this week, we re-underwrote the house view on global financials. Do check it out!

Before we get on to the weekly BUSHY™ and Acorn portfolio review, some unfinished business from the weekend edition.

So, you are big in Fintech?

Over the past decade the phrase ‘fintech’ has become an asset class that encompasses a multitude of worlds - from simple credit card and payments plumbing and predatory lending - to saying you were involved in crypto without actually wanting to use the ‘c’ word while Bitcoin was in a drawdown a couple of years ago.

Last November, I lifted the hood on the digital payment world after the number of hardcore value investors that were tweeting about PayPal PYPL 0.00%↑ reached a crescendo. I ended up including PayPal in a small basket of global payments companies that we added to the portfolio late last year.

The 🐿️ concluded that while we listen to a lot of hot air from VCs and fintech evangelists promising transformative productivity and growth vectors, payments are, at their core, a simple fee plus float business. They seemed like a reasonable play on a ‘higher for longer’ interest rate environment.

That bold macro thesis did not survive February’s violent sell off in high beta risk assets. I was stopped out of the broad basket at the end of that month. I did, however, hold on to a small position in Brazilian ‘neobank’ NU Holding. To be honest, this was more of a ‘LatAm bull’ call than anything else.

One subsector of the fintech world that the 🐿️ was definitely keen to avoid was BNPL or ‘Buy Now Pay Later’ (unsecured personal lending). Square / Block’s involvement (via Afterpay) was nearly enough to disqualify it from my original payment basket. The fact that Affirm AFRM 0.00%↑ is holding on to a $20bn market capitalization is a source of rodent bewilderment and I am not remotely surprised that Klarna’s IPO plans were put on hold in April.

BNPL is a classic example of one of the classic ‘red flags’ in corporate finance - namely, always be wary of a high growth financial. Fueled by tie-ups in hyper-discretionary spending segments from DoorDash burritos to Botox jabs and Coachella tickets, the BNPL originators have generated some wild top line growth.

Gross Merchandise Value (GMV) annual volumes have ballooned from around $30bn in 2019 to estimates of over $500bn for 2025 with forecasts approaching $1trn for the end of the decade. That’s IF these lenders make it that far.

The January 2025 US CFPB report on the sector makes for some chilling reading when it comes to the credit profile and (Oprah-style, “you get a loan!”) acceptance/ underwriting rates across the industry (do they turn anyone down?) Perhaps this is why certain folk in Silicon Valley are so keen to shut down or at least restrict the power of the CFPB). So much for the AI-powered credit scoring we were all promised!

The endless debates about recession odds (at the level of the entire US economy) ignore the fact that the (young and poorer) cohorts that are the biggest users of unsecured personal lending are probably ALREADY in a recession, whatever the PhDs at the NBER have to say about 2 negative quarters of GDP growth (18 months after the event).

Most BNPL lenders are either private equity backed or yet to accrue meaningful equity buffers and their primary revenue source (relatively high 2-8% - versus regular card payments - merchant fees) looks vulnerable to cost-cutting by retailers and service providers if economic conditions start to turn down.

Another risk facing the sector is access to ABS (securitization) funding markets. Credit capital markets may have rebounded sharply since the April spike in spreads but still feel fragile.

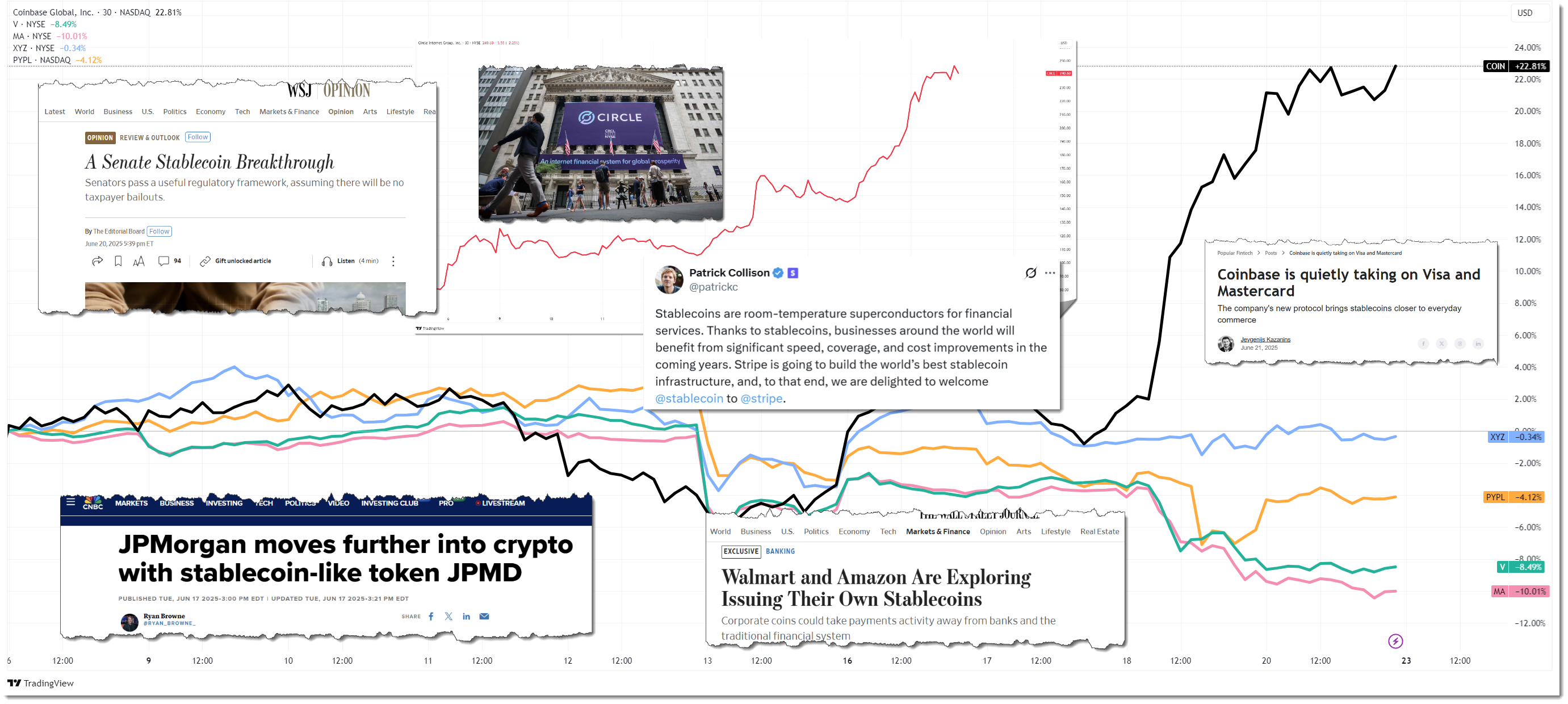

The BIG story in the broad church that is fintech these days is of course stablecoins. The last few weeks have seen the spectacular post-IPO stock price performance of USDC issuer Circle CRCL 0.00%↑ and more recently the passing of the GENIUS Act through the US Senate.

The 🐿️ is watching from afar with a quizzical gaze. I get why we all want cheaper and quicker payments (even if we might miss some of those safety/ insurance features and the airmiles). I get why Western Union’s share price chart resembles a challenging ‘double black diamond’ ski run. Expensive international remittances should have been a thing of the past many years ago.

I understand how Jamie Dimon will take defensive steps to protect his corporate deposit franchise. I get how giant retailers like Amazon and Walmart want to cut their banking and payment processing fees. I can also see clearly why Scott Bessent might be keen to foment another source of potential demand for his prolific T-Bill issuance.

However, there are a few big issues that have this rodent’s whiskers twitching:

We are all right to moan about the high rents we and merchants all pay in fees and charges to the Visa / MasterCard duopoly (and the layers on top of them like Stripe). Will we really be any happier paying those same rents to an alternative centralized fintech giant in the future (just without the reward points)?

Is it really smart to threaten the viability of the deposit franchises of our commercial banks? Please don’t listen to the hard money / narrow banking guys. I fear that a world without credit and fractional reserve lending looks kind of a bit Mad Max-ish.

Are we taxpayers not likely to be on the hook anyway if these stablecoin schemes go awry? I thought this comment from the WSJ Editorial Board was on point.

“The Senate legislation says stablecoins “shall not be backed by the full faith and credit of the United States” or subject to deposit insurance. But the FDIC insures bank deposits, and putting it in charge of regulating stablecoins may create the impression of an implicit government backstop. When the Reserve Primary Fund broke the buck after Lehman Brothers went belly up in 2008, Treasury guaranteed money-market funds to stabilize markets. Ditto for Silicon Valley Bank’s uninsured deposits in 2023. If a popular stablecoin breaks the buck, will the feds come to the rescue?” WSJ Opinion, 6/20/25

Silicon Valley Bank was only 2 years ago, folks! Circle, the issuer of the USDC stablecoin, had $3.3 billion in cash reserves on deposit with SVB at the time of the bank's collapse in March 2023. Just think about it. It has already happened!

It is hardly as though ‘Team Crypto’ comes with a stellar reputation for corporate governance standards. And when it comes to investment within the stablecoin ecosystem, it is even less clear where the opportunity lies.

Of course, technically the new legislation does not allow stablecoins to bear interest. This is semantics. The industry has already figured how to pass through the yield on the T-Bill collateral (less a haircut of course!).

If the ‘rake’ on USDG, backed by Kraken, one of the largest crypto exchanges, with Singapore’s DBS as custodian for the collateral is already sub 3%, how long before margins in the world of stablecoins get effectively competed down to zero.

No wonder the team at Tether, who have been keeping the lion’s share of stablecoin collateral yield for themselves for the best part of a decade are looking upset!

Best of luck to the new Circle CRCL 0.00%↑ bulls. Word of warning. Do not ride that ‘momo train’ for too long!

The BUSHY™ Portfolio - Week 25

BUSHY™’s 8-week winning streak finally came to an end, our beta portfolio closing Friday -0.36% for the week, +7.96% on the year.

Breaking down the returns at the asset level: