Episode 56 was recorded at 5.45pm EST on Sunday 31st May.

I am not able to publish paywalled commentary on a billing pause - so for the next 3 weeks, enjoy the show notes for free! Pod summary, show slides and audio edition are downloadable below.

Today’s Slides

Audio only version (for paid subscribers)

Pos Summary

Q2 Performance Review & The Semis Trade

Squirrel confesses to a poor Q2 — sat on his hands and missed the market rally

The one dominant trade of Q2: semiconductors — Korea, Taiwan, and SOXX (SMH) all parabolic

Everything else either flat or dragged higher by semis; EM is now effectively a semi ETF in disguise

Micron & Valuation Concerns (Minute 2)

Micron trading at price/ sales levels last seen at the peak of the prior tech boom

Debate on nominal vs. log charts for properly contextualizing valuations

Key question: what multiple do you put on peak semi earnings?

Darius Dale’s point cited: earnings expectations are a lagging indicator — analysts chase stock price narratives

Risk of an earnings bubble (analogous to 2006–07 housing, not a 1999-style price bubble) — multiples aren’t crazy, but earnings may be over-earning

“Amnesia” Theme Explained (Minute 5)

The episode title explained: Squirrel’s portfolio has “amnesia” — no memory (stocks)

He closed the call leg of his SMH strangle, cheapening September puts by ~15%

Congrats to those who rode the memory/semi bull - time to take chips off the table

~54–55% of the market is passive — non-thinking participants

Shorts (like Benny in April with SMH) got run over, leaving few on the other side

The “shoot it in the back” strategy discussed — warned it’s harder than it looks (silver analogy: down 37% in one day)

Momentum vs. mean reversion trade styles debated — both hosts identify as inherent mean reversionists

Institutional buyers of Hynix/Samsung running into single-name concentration limits

Marginal buyer now coming from structured products — leveraged ETFs/ETNs

Downside leverage works twice as aggressively — asymmetric risk building

Portfolio Performance & Energy Positioning (Minute 10)

Squirrel’s YTD performance chart shown: outperformed S&P through Q1, now behind after the semi rally

Only 30% equity weighting in multi-asset portfolio; over half of equities is energy

Watching BNO ETF (front-month Brent) — oil inventories have been decimated

“Barrel counters” all came into 2025 bearish and are now really worried about supply

AI CapEx Sustainability & Valuation Sanity Checks (Minute 14)

Ben currently doing deep work on Coreweave and the broader AI CapEx numbers

Free cash flow yield on Russell/QQQ is thin — market in “rare air” across multiple valuation metrics (Q ratio, Buffett indicator, trailing P, forward P)

Combined with potential earnings bubble = “very interesting situation”

Stocks as claims on the economy’s assets vs. actual income/GDP — market stretched at historic extremes

References Michael Pettis’s “bezel” concept: paper wealth exists only if you can actually exit

Post-GFC we’ve been in persistent overvaluation; 2022 was a small drawdown but “we’re back”

CapEx Funding Waterfall (Minute 18)

Nomura chart referenced: decomposing AI CapEx into cash-flow-funded vs. debt-funded portions

Capital markets funding sequence: cash flow → term loans → high-yield/IG bonds → equity

Warning: if Mag 7 start issuing common equity on top of IPOs, that would be a serious red flag

Cancellation of buybacks = first sign of equity dilution coming

$36B private credit deal done to fund Anthropic chip purchases cited as example of debt-funded CapEx

SpaceX IPO Valuation Sanity Check (Minute 24)

Compared SpaceX pre-IPO valuation vs. revenue multiples of prior major IPOs (Meta/Facebook, Google, etc.)

Facebook IPO anecdote: priced at $38, closed at $38 (Morgan Stanley used the whole shoe), then dropped to $17

Pre-IPO SPV deals with big front-loaded fees now circulating for SpaceX — reminiscent of Facebook retail frenzy

Day-one IPO returns historically poor for hot names; mechanics mean insiders are waiting to sell

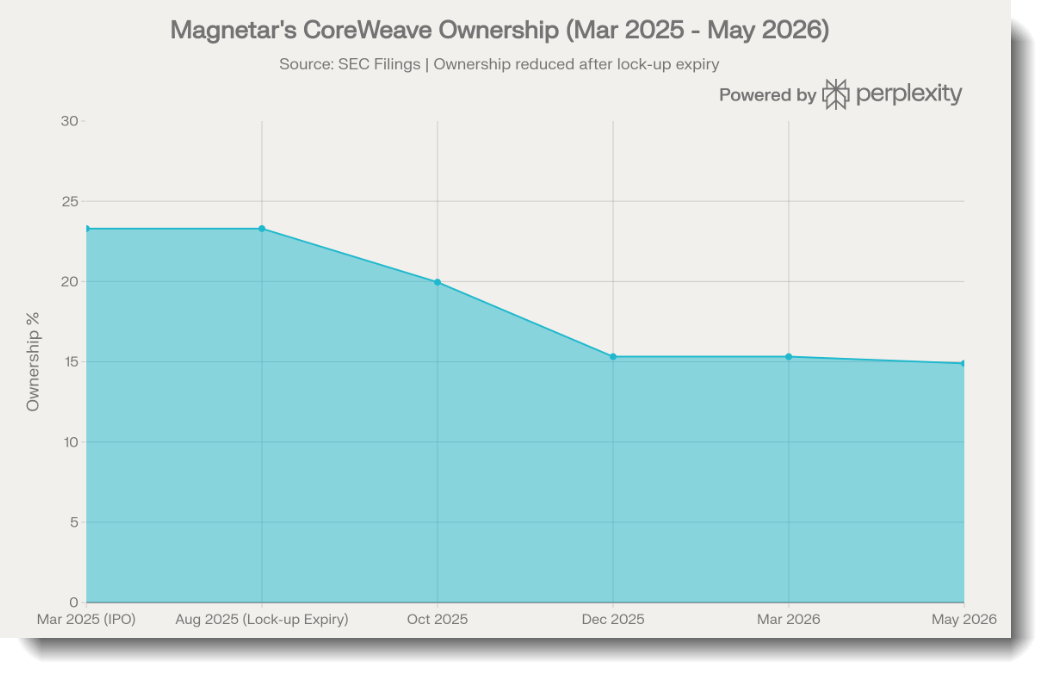

Coreweave / Magnetar / CDO Parallel (Minute 26)

Magnetar made $10B+ on Coreweave trade; drew parallel to their CDO trade pre-GFC — same characters, same playbook (get in early on the debt-funded boom, get out)

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.