Gonna need a bigger narrative!

The Blind Squirrel's Monday Morning Notes, January 29th, 2023.

Summary

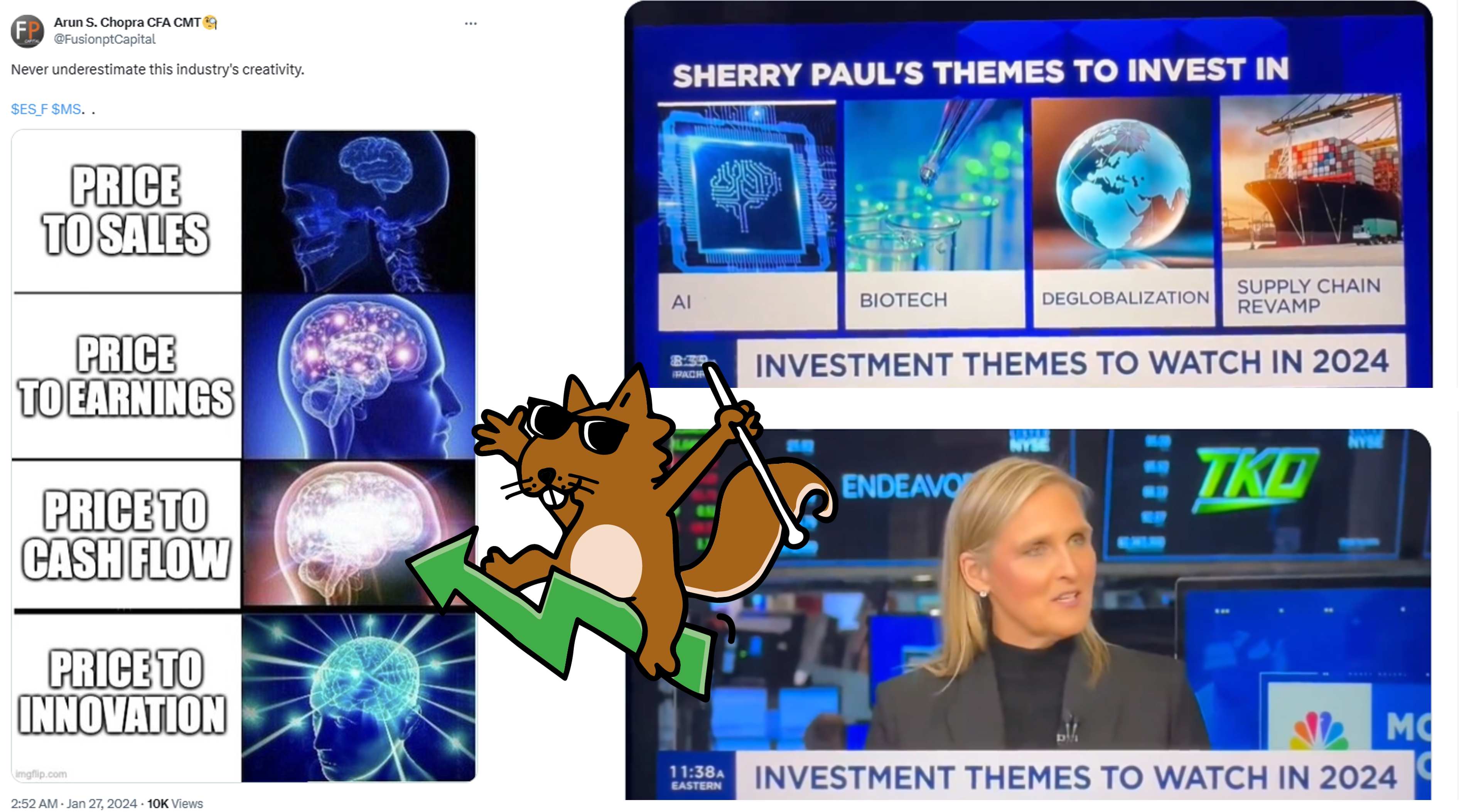

The 🐿️ dodges a Great White, while the Wall Street commentariat ‘jumps the shark’ with new valuation metrics for growth stocks.

We look at the role of semis in the current AI boom and think about what happened to the ‘picks and shovel’ stocks of the Web v.1.0.

In part 2, we discuss a big week ahead in macro and earnings; our semiconductor hedge; how to play (very tight) credit spreads; luxury names; energy and refiners; uranium; Brazil and Ags.

Welcome! I'm Rupert Mitchell aka The Blind Squirrel and this is my weekly newsletter on markets and investment ideas. If you've received it, then you either subscribed or someone forwarded it to you (add yourself to the list via the button below). Please also consider becoming a paid subscriber!

The audio companion to this week’s note will be uploaded to Substack on Tuesday to allow me to incorporate comments and feedback from this note. It will also be available as a podcast on Apple, Spotify and the other usual podcast apps.

Gonna need a bigger narrative!

As a relative newcomer to the ‘Lucky Country’, Ozzy Man Reviews’ “Oh Crap” sentiments are never far from the back of this rodent’s mind when contemplating the sheer quantity of lethal fauna knocking around ‘down under’!

The 🐿️ would like to assure readers that the spotting of a 4-meter Great White lurking just off the local beach where we were staying last week had nothing to do with our slightly earlier than planned return to Melbourne over the weekend. Chief Brodie’s iconic ‘gonna need a bigger boat’ line from “Jaws” spent the weekend bouncing around the 🐿️’s head.

We humans can never resist the urge to find a narrative to justify price action. In a week in which, the Magnificent Seven - scratch that, it’s now probably the Magnificent Six after Tesla’s recent earnings - continued their march higher, Wall Street’s commentariat had its very own ‘jump the shark’ moment.

Morgan Stanley’s Sherry Paul pretty much ensured that she will be haunted by the ghost of Benjamin Graham when she exhorted the need for investors to reframe how they think about justifying valuations in the age of innovation.

One of Wall Street’s leading equity shops has clearly decided to “educate investors” that the world of prosaic accounting multiples is perhaps too limiting. Apparently “price to innovation” multiples make it “worth it to pay the premium”. Surely this cycle has just found a new catchphrase.

During the late ‘90s/2000s dot-com boom, the 🐿️ was working at Salomon Smith Barney in Asia. As a firm, our TMT (technology, media and telecom) investment banking practice focused on the second ‘T’ and was largely a spectator to the Web 1.0 capital markets bubble. The internet powerhouses at the time were Morgan Stanley with their “Queen of the net” Mary Meeker and CSFB with its “Friends of Frank” [Quattrone] list.

At Salomon, we had to largely scrape together a living from the less glamorous plays on the Dotcom boom, the ‘alt’ telecom companies. For that business, our resident ‘royalty’ was the ‘rockstar’ telecoms analyst, Jack Grubman. We know how that story ended.

Your 🐿️ carried the bags during a couple of Mr. Grubman’s ‘state visits’ to the Asia-Pacific region, as he lectured starry-eyed senior executives of Korean and Taiwanese state-owned telecom companies about the miracles of Worldcom’s Bernie Ebbers and Global Crossing’s Drexel-junk-bond-trader-turned-telecom-scion Gary Winnick.

Our team ended up pretty much ringing the bell at the top of the ‘Alt Telco’ market with the IPO of Asia Global Crossing in October of 2000. The internet bubble was already beginning to gently deflate, but the allure of this Pan-Asian fiber network (with Softbank and Microsoft as partners alongside Global Crossing) was enough to squeeze one last FOMO trade out of the market. Side note: agile traders could have traded out of the IPO with a 40% gain if they sold in January of 2001.

Many commentators like to cite Scott Mcnealy’s valuation truth bombs when describing that era.

So why is your 🐿️ bringing you on this trip down memory lane? Sun and Cisco’s networking equipment, together with the fiberoptic cable networks of Global Crossing and its ilk were the ‘common sense’(!), ‘picks and shovels’ way to play the explosive internet theme back then.

Fast forward 2 decades and we have the AI boom. The ‘picks and shovels’ this time around are of course the semiconductor stocks. This sector, with the rampaging Nvidia at its head, has been at the forefront of investor focus ever since the launch of Chat GPT in late 2022.

Last Tuesday, I sent out a note looking at an options-based structure intended as a “FOMO sleeping aid” for investors that are worried about missing further moves in the sector (career-defining for investors with a cap-weighted index benchmark) but who are wary of the extreme valuations.

The reason that commentators feel the need to change the traditional metrics by which we value companies is clear. Jacob Shapiro and Rob Larity pointed out in their (as usual) excellent Cognitive Dissidents podcast this weekend that, with the exception of the Nvidia-focused GPU chip ‘arms race’, 2023 was not a great year for industry financials. The median outlook for semiconductor company cash flows is also far from stellar.

Let’s face it, Nvidia’s Jensen Huang has given the market much to be excited about and to extrapolate. Back to that 2002 Scott Mcnealy interview:

“I was thinking it was at $64 [per share for Sun Micro at the peak], what do I do? I'm here to represent the shareholders. Do I stand up and say, "Sell"? I'd get sued if I said that. Do I stand up and say, "Buy"? Then they say you're [Enron Chairman] Ken Lay. So, you just sit there and go, "I'm going to be a bum for the next two years. I'm just going to keep my mouth shut, and I'm not going to predict anything." And that's what I did.”

Announcing $20bn buybacks; ‘monster’ forward guidance; new product teases; private cloud initiatives with Equinix; and ‘AI factories’ with Foxconn Huang clearly has no plans to “be a bum for the next two years”. He seems keen to continue to fuel the perpetual motion machine.

Benchmarked money must continue to play the game while the music is still playing. It is no wonder that commentators are reaching for non-financial metrics in order to justify value. To torture the adlibbed words of Chief Brodie, we’re gonna need a bigger narrative!

That’s it for the front section this week. In addition to ‘Handling the FOMO’, last week we also published a new acorn trade idea on the global tire sector.

If you are not already a paid subscriber, please consider joining the 🐿️ on the ‘other side’ of the velvet rope where this week we will be discussing a big week ahead in macro; our semiconductor hedge; how to play (very tight) credit; luxury names; energy and refiners; uranium; Brazil and Ags.