Eyes on Stalks

The Blind Squirrel's Monday Morning Notes, January 1st, 2024. Happy New Year to all readers!

Eyes on Stalks

It was not until well into a long career of misusing it in conversation with bemused Chinese colleagues that the 🐿️ learned that the expression “May you live in interesting times” had no legitimate source in any learned Confucian text! The closest you can get to something similar in Chinese literature is "Better to be a dog in times of tranquility than a human in times of chaos." (Feng Menglong, 1627). Where on earth does that leave us poor rodents?

2024 is certainly set up perfectly for those apocryphal ‘interesting’ times:

Geopolitical tensions simmer on, with seemingly limited impact on risk assets (however many maps of the Red Sea get tweeted by excited owners of shipping stocks!)

Investors start the new year giddy from one of the best Santa Claus rallies in the history books.

But were Santa’s (The Fed’s) gifts evenly distributed, and will that potentially lead to some FOMO activity as the year starts and investors try to chase the ‘new market leaders’?

Normal New Year seasonal fund flows would in any event probably suggest that both fading the recent strength in risk assets is premature and that adding positions here would possibly be to err on the side of reckless.

Global liquidity and fund flows from retirement savings, collateral redeployment and fresh structured product hedging continue to overwhelm fundamentals-based narratives. We are, however, heeding Cem Karsan’s Delphic advice and keeping an eye on January’s VIX expiration (17th) as a potential window of weakness for risk (based on flows).

Recession (depth and timing) debates rage on in a manner very similar to this time last year. The 🐿️ finds himself in the uncomfortable position of having sympathy with both sides of the debate.

We need to get through critical political elections in 40 (!) global democracies, kicking off with Taiwan on January 13th and culminating with ‘The Big One’ (US Presidential) in November.

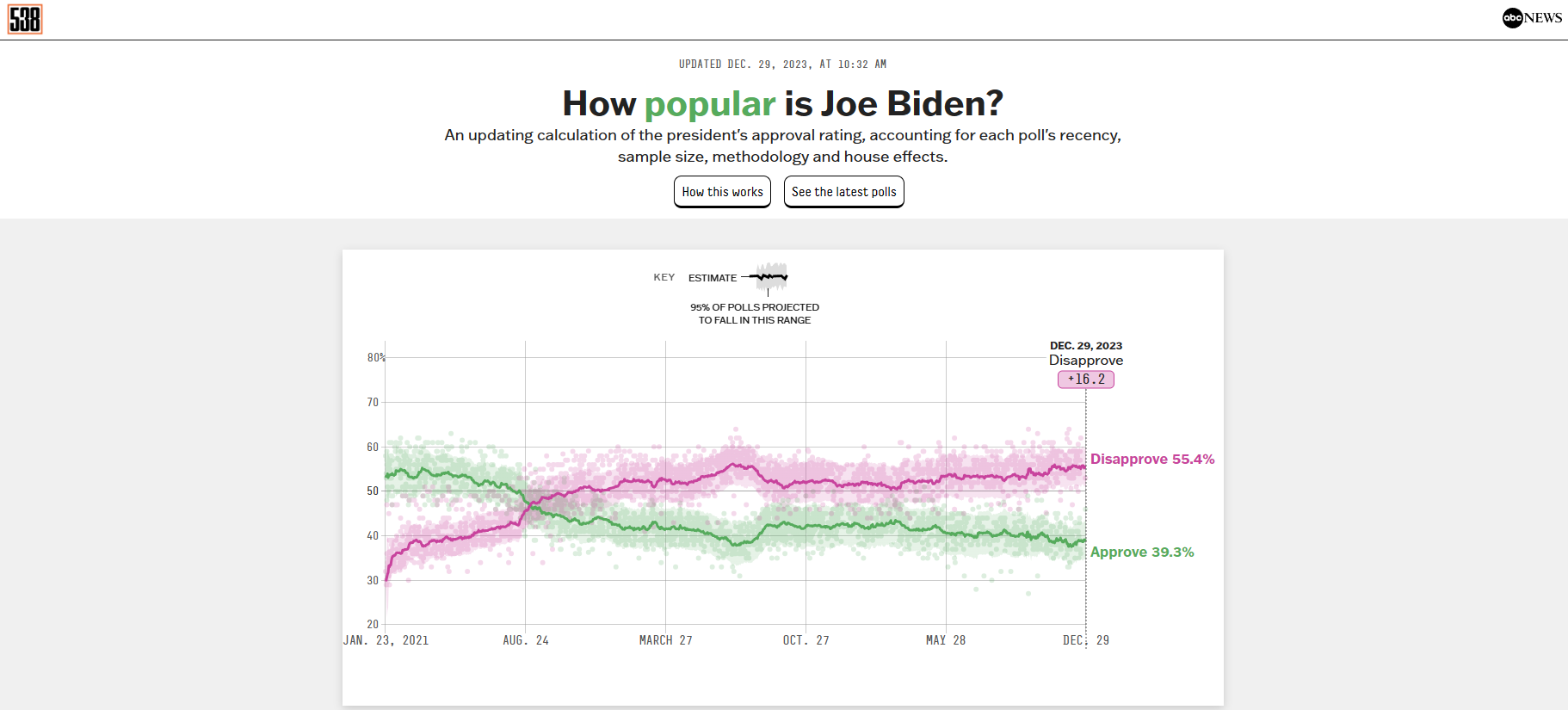

It does not require any tin foil headgear to see President Biden’s approval ratings as a key leading indicator for markets.

These polls make nightmare reading for Jerome Powell. His dreams are currently haunted by the ghost of Arthur Burns warning him about the reputational risk that comes with a premature easing that triggers an inflation resurgence. I imagine that when you are worth a few hundred million dollars, reputation is just about all that really matters.

On the flip side, a ‘higher rates’ triggered recession or collapse in equity markets likely leads to the election of a man that called him “a golfer who can't putt” (surely a completely unacceptable insult to a former private equity titan!).

Joking aside, I actually hate to be stressing this political dynamic. However, to be honest, that political-interference-in-monetary-policy horse bolted some time ago. Senior former Fed officials even have a track record of saying the quiet bit out loud.

Folk just need to park any ‘Financial Justice Warrior’ tendencies and get prepared to deal with it. If it makes you feel any better, try to think of it in terms of a function of human psychology rather than any kind of grand ‘globalist’ conspiracy theory.

Intellectually, building a case to be ‘short’ long duration fixed income and equities in 2024 is pretty straightforward. In practice, such a strategy would probably be very expensive against the backdrop of a dovish easing campaign from the Fed that may not cease even in the face of strengthening inflation and growth data.

We already saw some half-hearted attempts by Fed speakers to ‘talk out’ some of these ‘priced’ rate cuts before Christmas. The skid marks can be seen clearly on their Brooks Brothers’ shirts from where Santa’s sleigh ran them over! Hawkish noises accompanying some fresh bullish inflation data or employment developments could be more effective. Let’s see.

More information breadcrumbs come our way as soon as this Wednesday with the release of the FOMC minutes from the December meeting. The messaging there is likely to be well choreographed. Reactions to firm payroll numbers later in the week or firmer CPI/PPI numbers next week will be much more interesting to gauge.

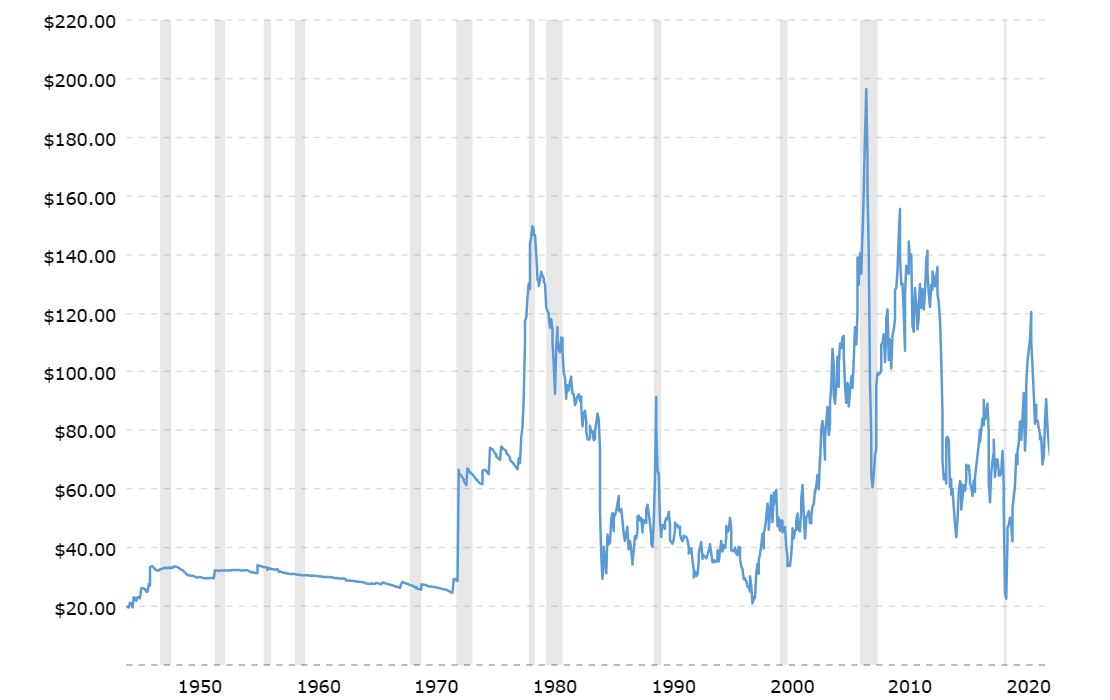

As regular readers are aware, the 🐿️ does not believe that the inflation genie is firmly back in his bottle. Energy is obviously the key input and crude oil is certainly on the back foot right now. However, zooming out, on an inflation adjusted basis WTI crude prices are only marginally above the levels seen since the formation of the OPEC cartel in the early 1970s.

This is creating a flattering picture for the only chart that is as important as President Biden’s approval ratings. Gasoline prices! These are down dramatically from the ‘torches and pitchforks’ levels of 2022 and will no doubt be managed aggressively in an election year. Even if they can be suppressed near term, there is a strong beach ball under water vibe about them. This article ‘The Peak in Gasoline Demand Turns Out to Be a Mirage’ certainly caught the 🐿️’s eye.

I fully acknowledge my inherent bias towards higher energy prices and inflation. There are plenty of folk much smarter than this 🐿️ that strongly disagree. One thing that many can probably agree on is that a return of inflation volatility is distinctly possible. This volatility will see stock / bond correlation revert to its normal (positively correlated) state.

I remain increasingly taken by the view that the last 2 decades of inverse correlation between equities and fixed income (the secret sauce of risk parity and the 60/40 portfolio) was an exception rather than a new rule. If the past 2 months are anything to go by, Treasuries and stocks, which have been moving in lock step, look to me like the same bet.

Eyes on Stalks

Like the young GI clutching his M16 on night patrol in the jungles of Vietnam, the 🐿️’s eyes are on stalks. Realpolitik dictates that the path of risk assets in an election year is higher. Shorting any asset outright, even if the fundamental arguments are impeccable, feels like a low ‘expected value’ trade.

Even if political deadlock in Washington ensures no further fiscal stimulus, there is still plenty of firepower from the ironically named Inflation Reduction Act that is yet to be spent. Easy monetary policy and liquidity management will pick up any remaining slack. However, there are risk trip wires (in the form of hot economic or inflation numbers) everywhere. And the bond vigilantes are lurking out there in the darkness.

That’s all for the front section this week. In second section (for the 🐿️’s paid subscribers) we will go through our 2024 gameplan for each asset class and review our existing live Acorn trades.