Doc, my EM Tech is Sick!

The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 9 of 2026.

Audio edition is already available on Substack app and browser! Since starting to write this note mid-week, I have made some significant changes to the portfolio. I accelerated the de-grossing of both the BUSHY™ beta portfolio and the Acorn book. Full details will be in tomorrow’s ‘Start the Week’ note. Emerging Market tech equities received some of the most aggressive pruning. Possibly overdue.

Richard Oldfield, the legendary value investor that started his career in the early 1970s at Warburg Asset Management (later Mercury, now subsumed into Blackrock (via Merrill Lynch) - sigh), is the author of one of the 🐿️’s favorite books on investing - “Simple, But Not Easy”.

In the book, Richard argues that meeting with company management is dangerous because it can compromise an investor’s objectivity. He warns that executives are often highly charismatic salespeople capable of spinning compelling narratives that can distract from fundamental realities.

I would put certain company site visits in the same category. Last October, the 🐿️ visited Tencent’s investor center as part of a day of meetings in Shenzhen.

After the session, I concluded that Tencent was still cheap and that it would be premature to sell any shares:

“After a very good run, I had been beginning to feel that my single largest China exposure was due for a trim. The Tencent of 2025 is so much more than the owner of the WeChat ‘super app’ with a leading video game publisher and cloud business tacked on the side. It is hard to understate the penetration of the group’s tentacles into so many corners of technology innovation. Standalone decacorns and unicorns lurk behind every corner and also pose potential existential threats to many already listed global technology companies.” - (Link to full meeting report from October).

Wrong call! Should have listened to Mr. Oldfield. I had morphed from indifferent rodent to fanboy.

The stock has taken a 20% dirt nap since a dizzy 🐿️ re-underwrote his position. I finally sold the majority of my Tencent shares last week as part of a global de-risking of my equity book.

The 🐿️ has been bullish on emerging markets since late 2022. My early buys were deep value plays - anchored by a large position in DVYE 0.00%↑ (the iShares Emerging Market High Dividend ETF).

My original position in Tencent had a value angle too - my original exposure was via the Naspers-controlled Amsterdam listed holding company, Prosus (i.e., Tencent exposure at a massive discount). I flipped into the HK line of Tencent when Prosus bought yet another food delivery app business. Regular readers know my views.

The low beta, low valuation approach to EM investing has been a winning path in the most recent cycle. There are times when the “Western Fried Rice” approach (basically KWEB 0.00%↑ or BABA 0.00%↑ call options) has delivered short-term lottery ticket returns (e.g. ‘Tepper Time’ in September / October 2024).

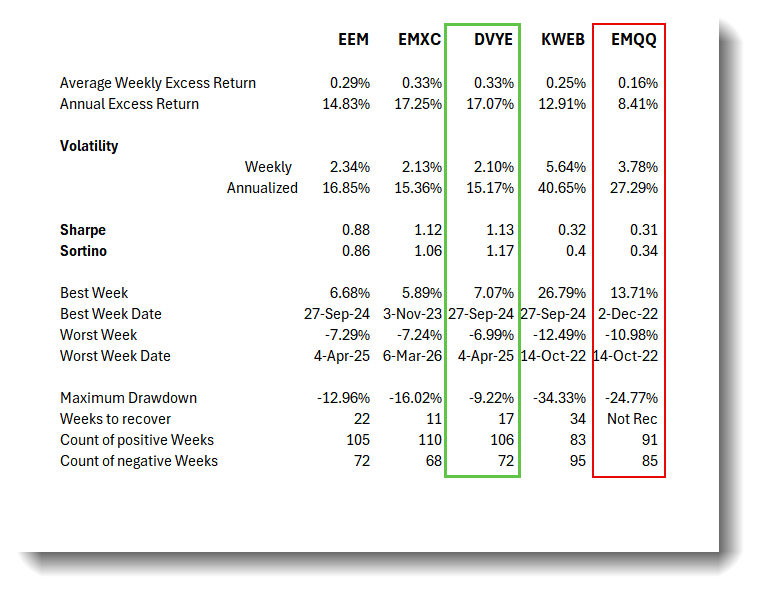

During this period DVYE 0.00%↑ has produced superior total returns to other broad-based EM exposure such as EEM 0.00%↑ EMXC 0.00%↑ (EM without China) KWEB 0.00%↑ (China Internet) and EMQQ 0.00%↑ (EM Internet).

Furthermore, it has done so with a significantly superior volatility (15% annualized) and drawdown (max 9.22%) profiles. I calculate a Sortino ratio of 1.17 (between October 2022 and now) for DVYE versus EEM at 0.86.

Last week, I also waved goodbye from my BUSHY™ beta portfolio to the fund with the worst Sortino ratio - that EMQQ 0.00%↑ ETF. I had originally bought the position in EMQQ in September 2024 as a (very) crude long hedge against short positions in profitless US delivery companies / SBC Incinerators. I was making a point about EM tech companies treating their shareholders better on the capital allocation front (still very much the case).

I got stopped out of that DASH 0.00%↑ short position pretty rapidly (my poster child delivery app target eluded me again) but my ‘hedge’ was up 30% in a month and transitioned to a core holding lazy long.

After 2 violent ‘yo-yo’ roundtrips in early 2025, I sold half of the position in early January this year. The balance became part of my ongoing de-grossing exercise last week - again, further details in The Drey and in tomorrow’s ‘Start the Week’ note.

Doc, my EM Tech is Sick!

So to the title of this note. With hindsight, it took me way too long to react to the fact that not all emerging market trades were working uniformly. As mentioned before, I had certain PTSD-related reasons for not participating in the recent DRAM risk ‘orgy + slaughter’ up in Korea