In Episode 57: Ameesh Agarwal (CIO, University Place Asset Management) joins Benny and the 🐿️ to dissect the economics of AI data center investing. His firm underwrites the base infrastructure layer — shell, power, and location — avoiding GPU exposure due to uncertain 4–7 year depreciation cycles and negative unit economics.

The show was recorded at 6pm EST on Wednesday 3rd June, 2026.

I am not able to publish paywalled commentary while on a subscription billing pause - so for the next couple of weeks, enjoy these show notes for free!!

Audio only version (for paid subscribers)

Podcast Summary

Introduction

Ben (Benny) introduces Ameesh Agarwal, CIO of University Place Asset Management (‘UPLAM’), for a special data center-focused episode

Ameesh’s background: UPLAM has historically been an alternative assets investor — opportunistic credit and real estate across geographies

Entry into data centers was organic: demand for capital outpaced supply, creating attractive risk-adjusted yields; LPs (primarily insurance companies and securities firms) had appetite to invest via infrastructure arms

Data center underwriting mechanics are similar to real estate — long-duration, income-producing assets

The AI CapEx Supercycle & Scale of Spending (Minute 3)

The 2023 ChatGPT/OpenAI “aha moment” triggered rapid AI diffusion and the concept of “a country of geniuses in a data center”

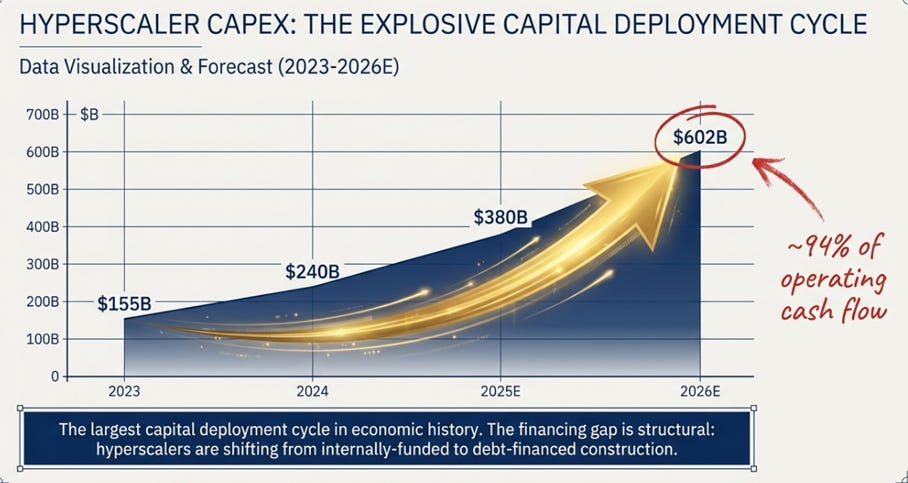

Hyperscaler CapEx estimates: ~$600B initially for 2026, revised to ~$800B; total proposed hyperscaler spending is $1.1T

Per NVIDIA’s earnings call: 50% of forward GPU demand is hyperscalers, 50% is neoclouds and others — total sector CapEx consensus is well north of $1T

Capital requirements can only be met by the largest companies; smaller players are structurally disadvantaged

SpaceX / xAI Discussion — Colossus, Grok & TAM Claims (Minute 4)

SpaceX’s upcoming IPO and the question of whether its terrestrial AI compute (Colossus I & II) is included in the $1T CapEx figure

Ameesh is skeptical of xAI’s position: xAI/Grok claims a $27T TAM (close to US GDP), with ~90-93% attributed to AI, but xAI only captures ~3-4% of the actual AI frontier lab market

Ameesh personally uses Anthropic every day but doesn’t know “a single person besides Twitter users who use Grok”

Colossus is effectively acting like an Iren or CoreWeave — leasing GPUs, providing compute to Anthropic (paying ~$1.5B/year, representing $25B of revenue) — a pure GPU-rental model, not a frontier lab

🐿️: “There’s two trillion dollars riding on that being a reality” — skepticism is noted but the stakes are enormous

Data Center Economics 101 — Real Estate Analogy & Key Metrics (Minute 7)

Data centers are not fundamentally different from real estate leasing: long-term leases (10–15 years, with 5–10 year extensions), similar to warehouse leases

Key metric difference: real estate = price per sq ft; data centers = price per megawatt

Location hierarchy: Tier 1 markets (Northern Virginia, downtown Chicago) > Phoenix/Austin > remote locations — just as Manhattan sq ft > New Jersey sq ft

Location matters for: fiber access, “meet me rooms,” latency, network nodes, available/reliable power, and water for GPU cooling

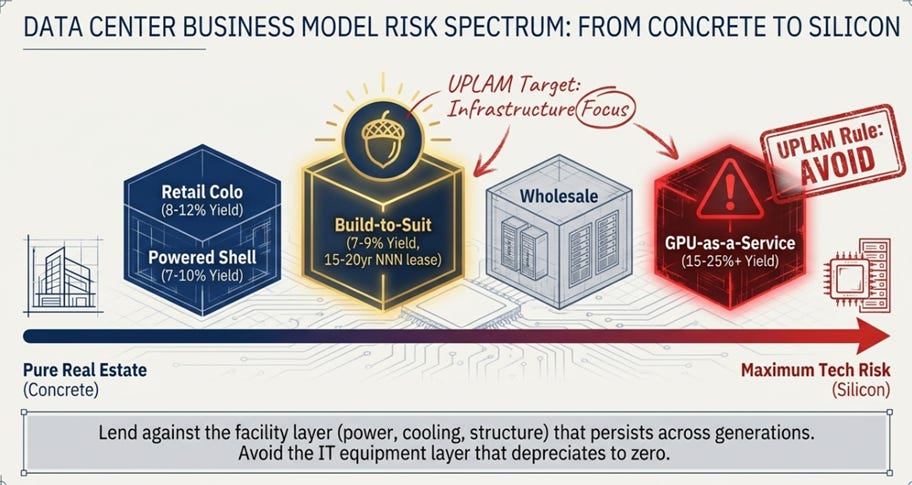

The four critical underwriting factors: (1) Location → (2) Power → (3) Developer/Sponsor quality → (4) Tenant quality

Experienced developers (Vantage, Aligned, Compass One) vs. overnight opportunists — Ameesh sees clear differences in sophistication and underwriting quality

Ameesh’s firm finances the base layer (shell + power), not the GPU layer — by analogy, the “roads” needed regardless of which car wins (Mercedes, BMW, train etc.)

The shell and power have indefinite useful life (”Virginia is not going anywhere”)

GPUs are the problem: useful life is debated — Michael Burry says 2–3 years, hyperscalers underwrite 4–5 years, Ameesh uses 6–7 years as a generous assumption

Even aircraft leasing has a longer economic lifespan than GPU hardware

Risk is not fully eliminated for the shell lender: if the tenant (who owns the GPUs) fails, the lease collapses; tenant quality is therefore paramount

Hyperscalers (Amazon, Google, Microsoft) are the best tenants — fortress balance sheets, multiple downstream service layers that generate higher revenue per GPU CapEx than pure intermediaries

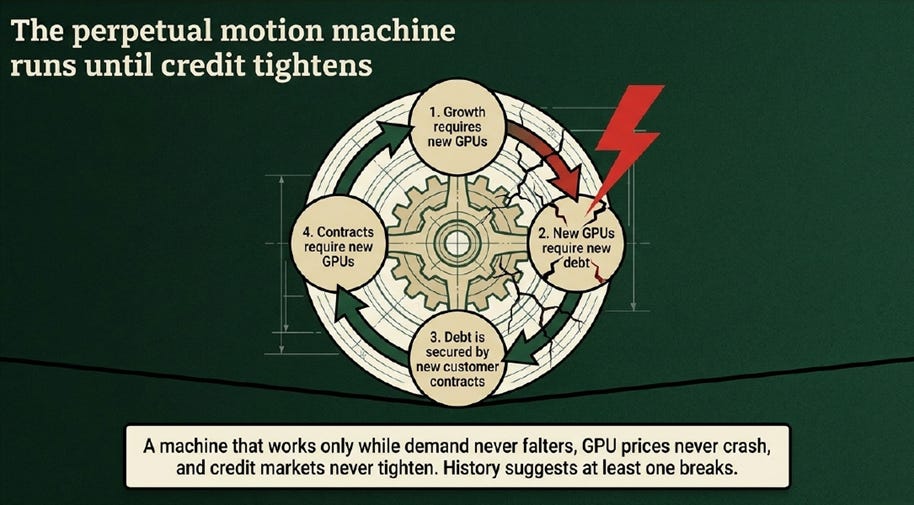

CoreWeave’s Unit Economics — The WeWork Analogy (Minute 16)

CoreWeave’s business model: rent GPUs from NVIDIA, take on leverage, lease compute to frontier labs and hyperscalers — a pure intermediary with no proprietary software (all open-source) and no moat beyond GPU access

Revenue generates negative unit economics: buying a GPU that depreciates in ~7 years and leasing it out does not generate enough revenue to repay CapEx at any reasonable WACC

CoreWeave positions itself as a “systems integrator” — but every cloud provider offers the same capability

WeWork parallel: WeWork leased office space, sub-leased it at a loss, dressed it up as a “software company” and “community platform”; CoreWeave does the same with GPUs; the buzzword is “AI infrastructure” instead of “community”

Leverage amplifies the problem: “leverage makes any bad investment worse”

CoreWeave’s debt position: ~$27B drawn, ~$13–15B remaining capacity across credit lines and delayed draw facilities

Revenue target: ~$10B for 2026; even if quadrupled to $40B at steady state, the business remains problematic when measured on EBIT (not EBITDA) with 4–5x debt/equity ratio

The Valuation Methodology Problem — “Make DCF Great Again” (Minute 21)

Investment banks model CoreWeave to its one peak EBITDA year, apply an EV/EBITDA multiple, and declare a valuation — this is fundamentally wrong

EBITDA multiples assume perpetual cash flows; CoreWeave’s cash flows are NOT perpetual because they require constant CapEx reinvestment equal to GPU depreciation cycles

Correct approach: normalize EBITDA by replacement CapEx based on GPU useful life; at any assumption (4, 5, 6, or 7 years), with 10% residual value, the business is insolvent

The cash flow pattern: negative at CapEx → negative for years → briefly positive → CapEx cycle repeats; IRR is approximately 2–3%

Rupert frames it: “It’s an equipment leasing business — what’s the value of the equipment, how long is there value to it? This ain’t ski rental” (skis pay for themselves in two rentals; GPUs take 6–7 years)

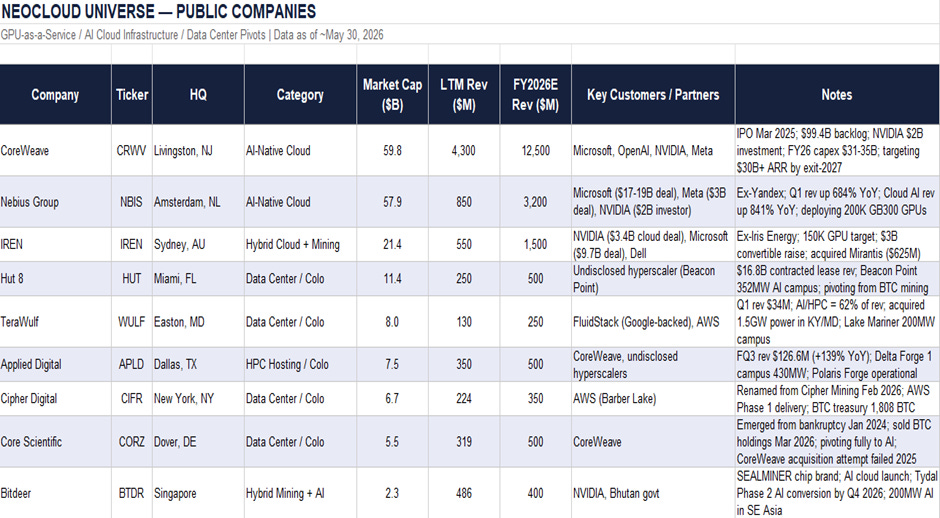

NeoCloud Taxonomy — Not All Are Equal (Minute 23)

Ameesh distinguishes between fundamentally different neocloud business models:

Pure shell/power providers (Applied Digital, Cipher Mining/TeraWolf — former Bitcoin miners): provide power and shell only, lease space to hyperscalers or neoclouds; do NOT buy GPUs; power is their moat

Full-stack integrated operators (Iren, Nebius): own the power + shell AND buy the GPUs — end-to-end integrated

GPU-only neoclouds (CoreWeave, Fermi): lease power/shell from a developer (paying a substantial premium), buy GPUs on leverage, lease compute out — highest cost structure

Why Iren and Nebius are better positioned than CoreWeave:

They own their own power/shell (no premium lease payments to developers, who target double-digit returns / 2x money over 6–7 years)

They carry the long-life power/cooling asset on the balance sheet (much longer depreciation)

Unit economics are “slightly better” — but GPU depreciation risk still exists for both

CoreWeave’s structural disadvantage: must sign leases at a significant premium (vs. hyperscalers) because developers price in higher risk; all that margin is extracted before GPU revenues are even considered

“The only reason CoreWeave exists is so NVIDIA has an alternate customer versus hyperscalers who will eventually come for Jensen’s margins”

Ameesh agrees: CoreWeave is a “distribution shelf” for NVIDIA — not a business with proprietary IP or moat

NVIDIA’s $2B investment in CoreWeave is effectively free optionality: NVIDIA received $2B+ back in GPU revenues the same year; if CoreWeave succeeds, the investment multiplies; if not, principal is recovered

Historical parallel: Lucent financing its own customers during the dot-com era (keeping the build-out going, then collapsing)

Anthropic now trains on Google TPUs (not NVIDIA GPUs) specifically because Google made early investments — NVIDIA failed to invest and lost the customer

NVIDIA’s moat deepened by customer lock-in: high switching costs once companies build on GPU infrastructure; that’s the strategic logic behind financing distribution channels

Power Scarcity as the Durable Moat — Former Bitcoin Miners (Minute 36)

“Never bet against engineers” — over time, efficiency improvements will reduce power and cooling requirements per unit of compute

However, even as efficiency improves, the grid is backed up and cannot be built overnight; demand growth is outpacing efficiency gains for the foreseeable future

Larger data centers are increasingly pursuing behind-the-meter on-site generation — Ameesh’s firm finances some of these

50% of US citizens wouldn’t want to live next to a nuclear power plant; the figure for AI data centers is 70% — permitting is getting harder, not easier

Former Bitcoin miners (Applied Digital, TeraWolf, others) with existing power rights are being valued as scarce commodity plays by the market — tough shorts even with stretched valuations because power scarcity is real and durable

Ameesh’s firm now shies away from deals where power is “in the backlog” vs. in hand; deals with power secured vs. speculative pipeline are fundamentally different underwriting scenarios

Capital Markets Deep Dive — Credit Pricing, Debt Structure & Risk (Minute 39)

Credit spread differentiation: hyperscalers (investment grade) price at ~200bps over SOFR; neoclouds price at ~400bps over SOFR

Neoclouds increasingly unable to access private credit; CoreWeave recently resorted to the junk bond market (7–7.5% coupon)

Junk bond buyers are not sophisticated underwriters — they are bond traders relying on ratings, with no concept of GPU depreciation cycles; “they have no idea what they’re financing”

Parallel explicitly drawn to 2007–2008: insurance companies, Asian and European desks buying paper without understanding the underlying — “Belgian dentists backing the truck”

CoreWeave’s Debt Structure — SPE Tranching & Capital Waterfall (Minute 42)

CoreWeave has multiple tranches: revolvers at the corporate level + SPE-level debt secured by underlying contracts and GPUs

SPE loans are written to depreciate in line with GPU lifecycles (~4–5 years), meaning revenue flows first to repay SPE debt before reaching the parent

By the time revenues “hit the parent,” they are already collateralized

At the corporate level: senior unsecured creditors are exposed with minimal credit enhancement

LTV of 90–95% being written in some deals — “just be the equity guys” at 5% credit enhancement

The system requires capital markets to remain permanently open: “any jam in the capital markets could cause major problems across the stack”

Neocloud debt is material and growing in the high-yield index; insurance companies globally are buying this paper through products designed specifically for that market

The Offtake Agreement Dependency (Minute 45)

Google previously guaranteed lease payments for tenants (e.g., FluidStack) as a mechanism to push Google TPU adoption — Google has since stopped providing these “credit wrappers”

Credit wrappers are becoming less common — hyperscalers are pulling back from guaranteeing neocloud leases

Neocloud financing is now entirely codependent on hyperscaler offtake agreements with no credit guarantee backstop

If a hyperscaler pulls back or cancels a contract, the domino effect across the entire neocloud financing stack is severe

The Magnetar Trade Analogy — 2007 CDO Parallel (Minute 49)

Ben and Ameesh connect the CoreWeave ecosystem to the Magnetar trade of 2006–2007:

Magnetar bought CDO equity tranches, owned senior tranches, and purchased mispriced CDS — effectively keeping the CDO market alive 18–24 extra months

Today, Magnetar is the largest shareholder of CoreWeave — same playbook, different asset class

The circular financing dynamic: Magnetar/Google get paid via GPU revenues/cloud revenues while simultaneously being long the equity — structured to be OK either way

Banks financing these deals retain zero risk (fee-driven), are not underwriting the assets, and are likely buying CDS against the same companies on different desks — “the same bankers retailing the risk”

Investment Analysis Quality — “The Gap Between Perception and Reality”

Ameesh’s critique: most hedge funds, investment analysts, and sell-side do not understand what they are underwriting in AI infrastructure

Analogy: a semiconductor analyst covering photonics (Lumentum), memory (SK Hynix), and CoreWeave is covering completely different businesses — requires fundamentally different frameworks

The single most important input for CoreWeave valuation — GPU depreciation cycle — is routinely omitted or improperly handled in bank models

Investment banks show the EBITDA-positive year, apply a multiple, and move on — ignoring that it is NOT a perpetuity

Incentive misalignment: pod shop time horizons of 1–3 quarters, trend followers and passive funds dominate flows, bankers just want to get deals done for fees

How Does It Play Out? Catalysts & Positioning (Minute 55)

CoreWeave has minimal economic value and debt spiral tendencies. The market is fragile: the gap between perception and reality is rarely this wide

Math can be right but “you can still lose your shirt” going against momentum in open capital markets

Goldman’s numbers show the year-over-year first derivative of CapEx growth is peaking right now — the rate of acceleration is topping out

Framework: find the most robust (long) vs. the most fragile (short) in a capital market state transition

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.