Concentrating on China

Rebuilding the 🐿️'s post-Hormuz China book. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 18 of 2026.

In last week’s note covering the opportunity in the Asian life insurance sector, I mentioned that I was working on reorganizing my concentrated China ‘Acorn’ book in part to make room for these 2 new additions but also to tilt the portfolio’s focus as we gross it back up once the Hormuz Crisis is in the rearview mirror. I am now ready to share it.

But First, a Quick Macro Hit

China’s headline Q1 GDP growth print (5.0% YoY) was optically a ‘beat’ but most Sino-watchers were quick to point out that heavy (export driven) front-loading of industrial output in January and February was already fading by the end of the quarter.

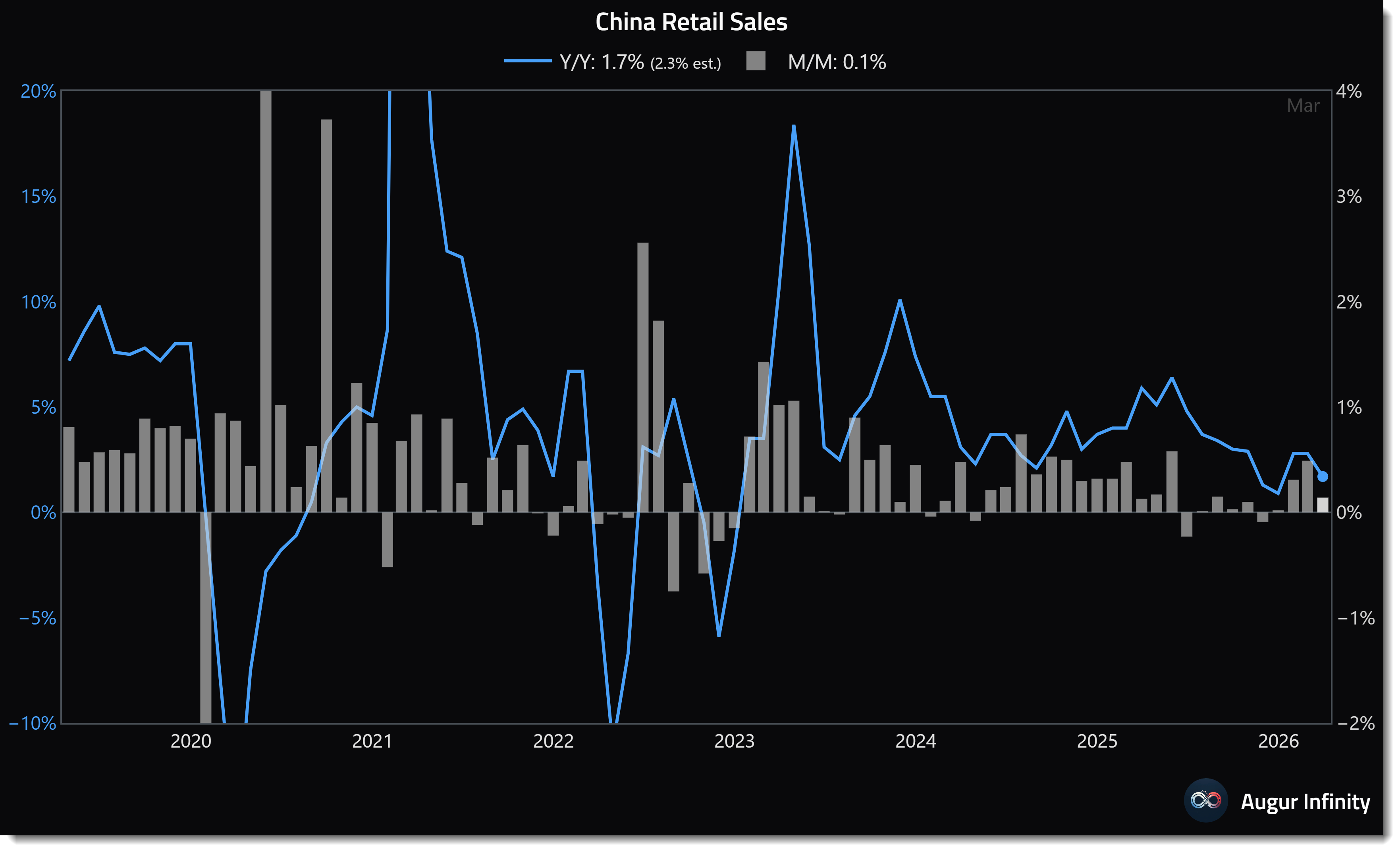

The consumer remains the weakest link. We saw retail sales growth fall back sharply in March.

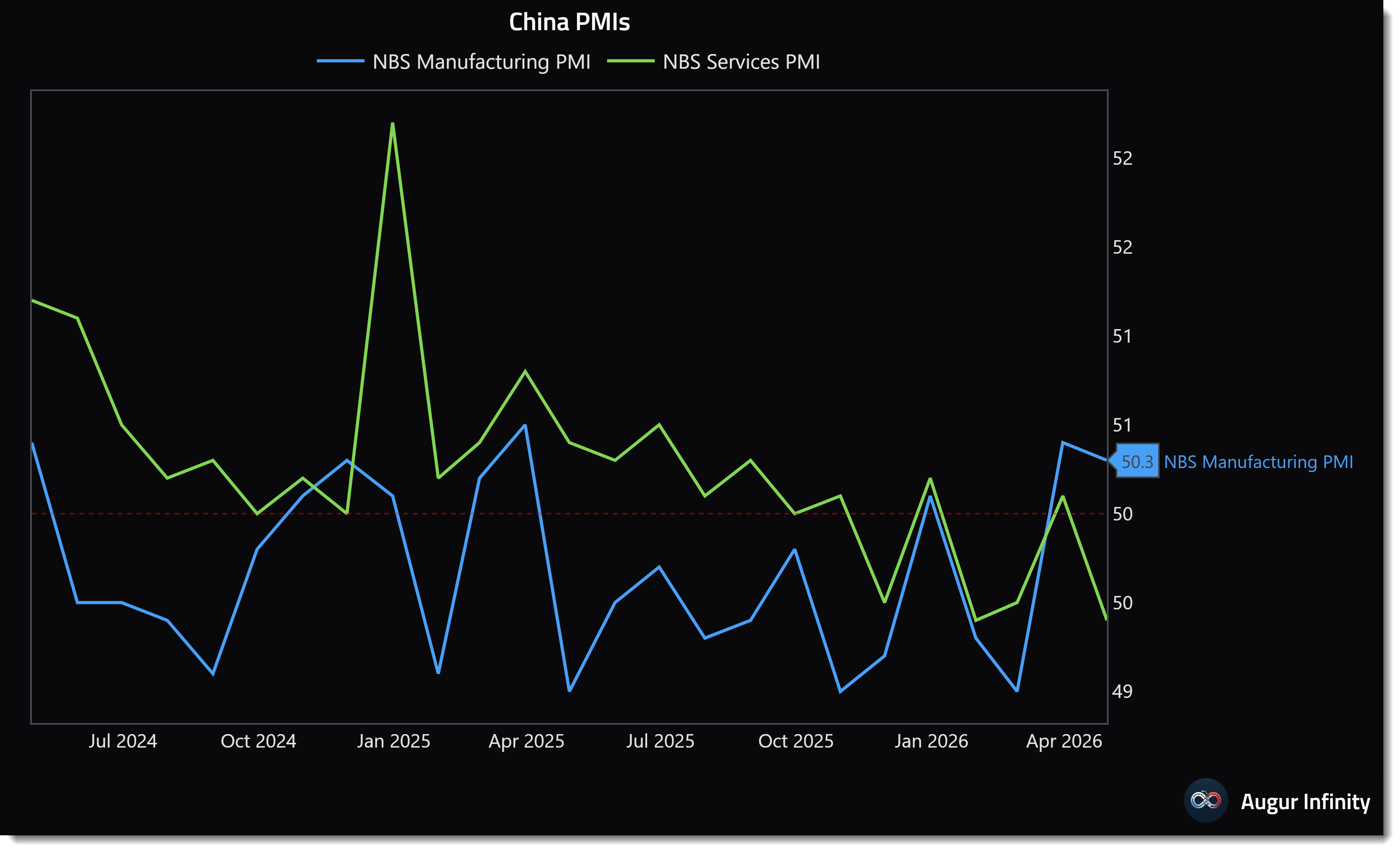

Services PMIs dropped back into contractionary territory, with Manufacturing PMIs staying just above the line.

Will it be enough to keep factory-gate inflation above the zero bound? March’s +0.5% (largely energy-driven) PPI print was the first positive one in 41 months.

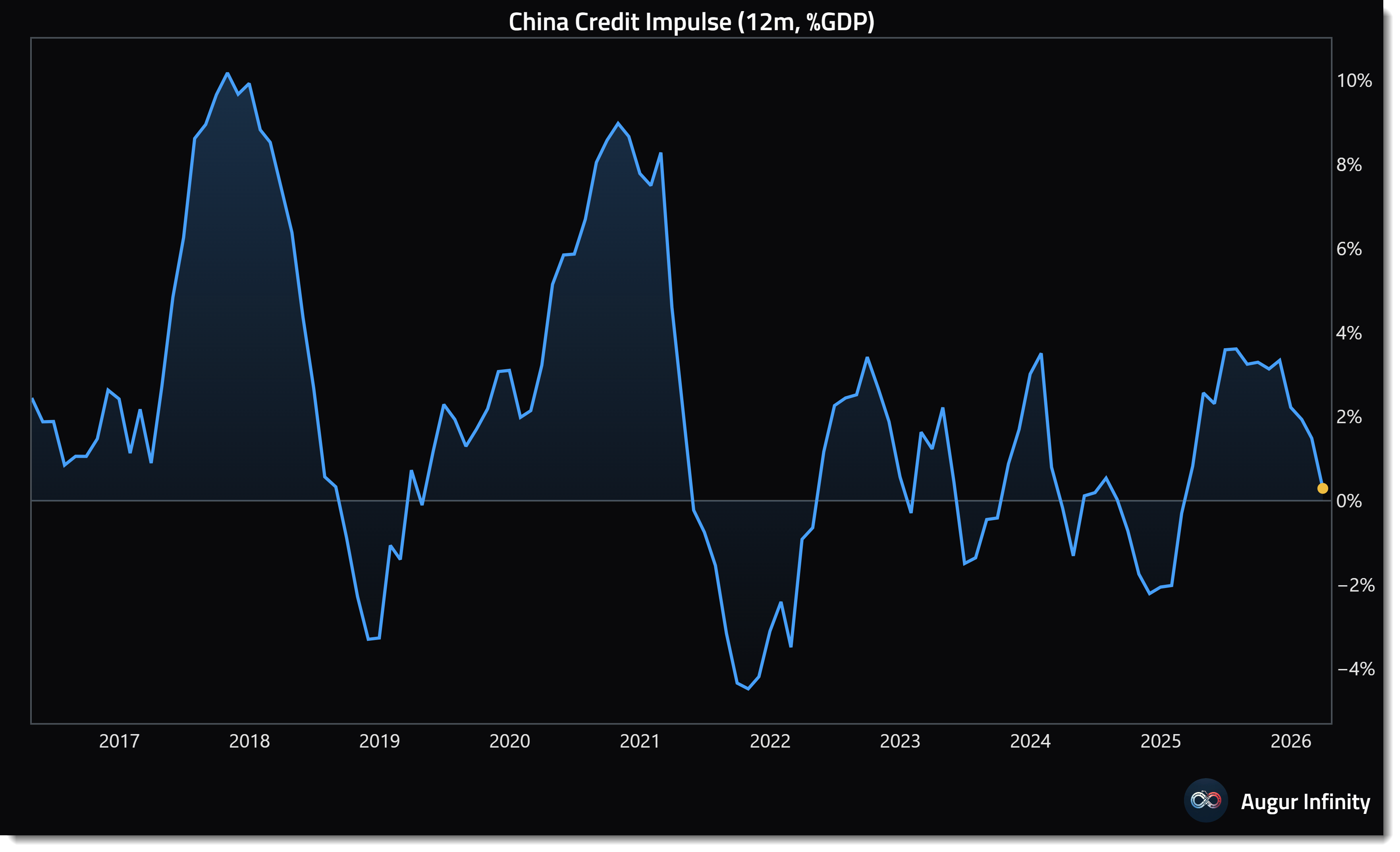

On the fiscal side, Beijing appears to have kept its powder dry in Q1, holding stimulus in reserve rather than front-loading spending.

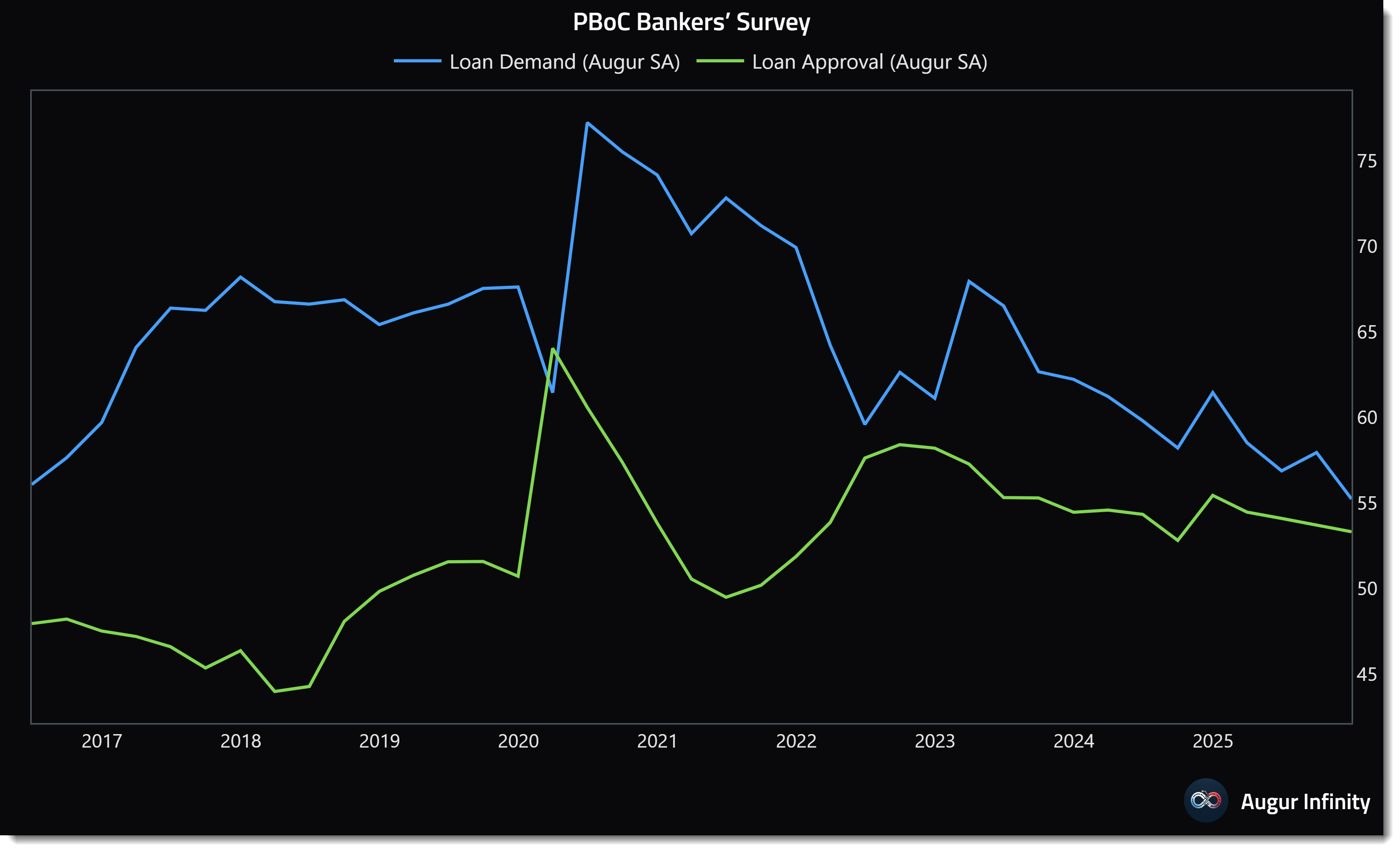

Loan demand continues to fall off.

The key macro takeaway is not that China is suddenly in a state of rude economic health. Growth is still uneven; policy is still selective; and market leadership is shifting faster than the 🐿️’s existing portfolio has so far this year.

Current Positioning

If the Strait remains closed for a protracted period of time, all bets are off. However, assuming that global economic damage from the Iran War can be contained at somewhere close to current projections, the 🐿️ remains a China equity bull.

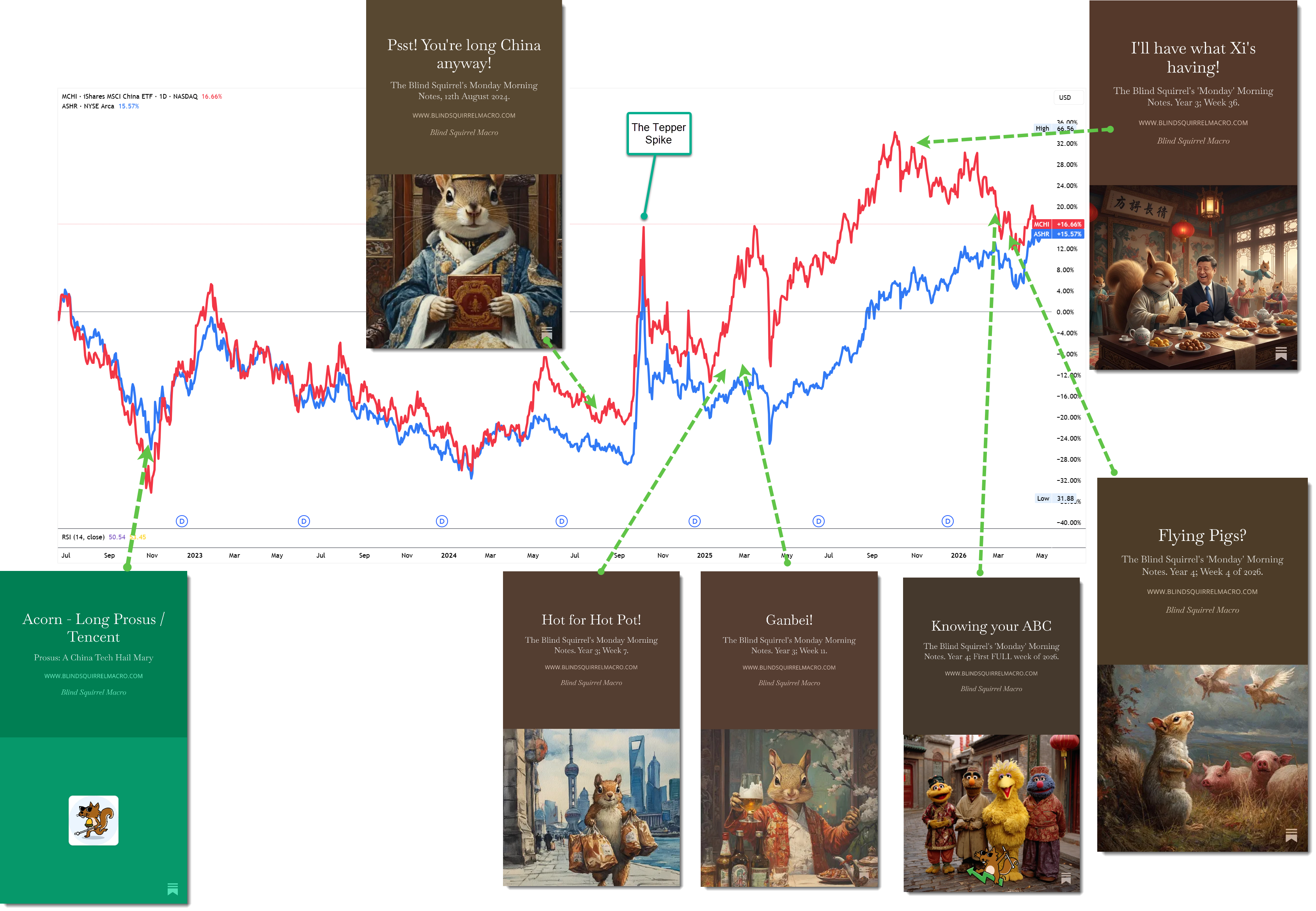

Let’s recap position from the start (plotted below against the MSCI China and CSI 300 in USD since mid 2022). My first post-pandemic foray back into Chinese equities dates back to October 2022 (a lonely time!). By August 2024, China was back to a significant overweight position in the Acorn (alpha) book (well ahead of that ‘Dave Tepper spike’ in September 2024).

We added consumer focused baskets in early 2025 before listening to Beijing’s call for ‘rational investing’ in September and diluting the consumer angle with lower beta telecom and power infrastructure exposure. The latter worked well, the former got hit with a new tax bill.

In January we increased explicit China exposure to our BUSHY™ (beta) portfolio via the ASHR 0.00%↑ and FXI 0.00%↑ ETFs (previously the portfolio’s overweight China exposure came via DVYE 0.00%↑ and EMQQ 0.00%↑ ). We also added a position in WH Group (288.HK) which we closed last week as the pork giant’s stock finally responded to rising global corn prices.

We started aggressively de-grossing both BUSHY™ and the Acorn equity book in early February and were most of the way done before everything kicked off in the Middle East.

The 🐿️’s current China positioning sits as follows: