Blighty and the Binface Bottom

Re-underwriting UK risk assets. The 🐿️'s 'Monday' Morning Notes. Year 4; Week 28 of 2026.

“I will be a unity candidate and pledge to build at least one affordable house.” Count Binface, July 2026.

Monday sees Andy “we’ve got to get beyond this thing of being in hock to the bond market” Burnham enter No. 10 Downing Street unopposed. 3 weeks later, we get to see if the populist fever dream has hit an absurd and terminal climax in the form of Nigel Farage being vanquished in the Clacton by-election…by a bin.

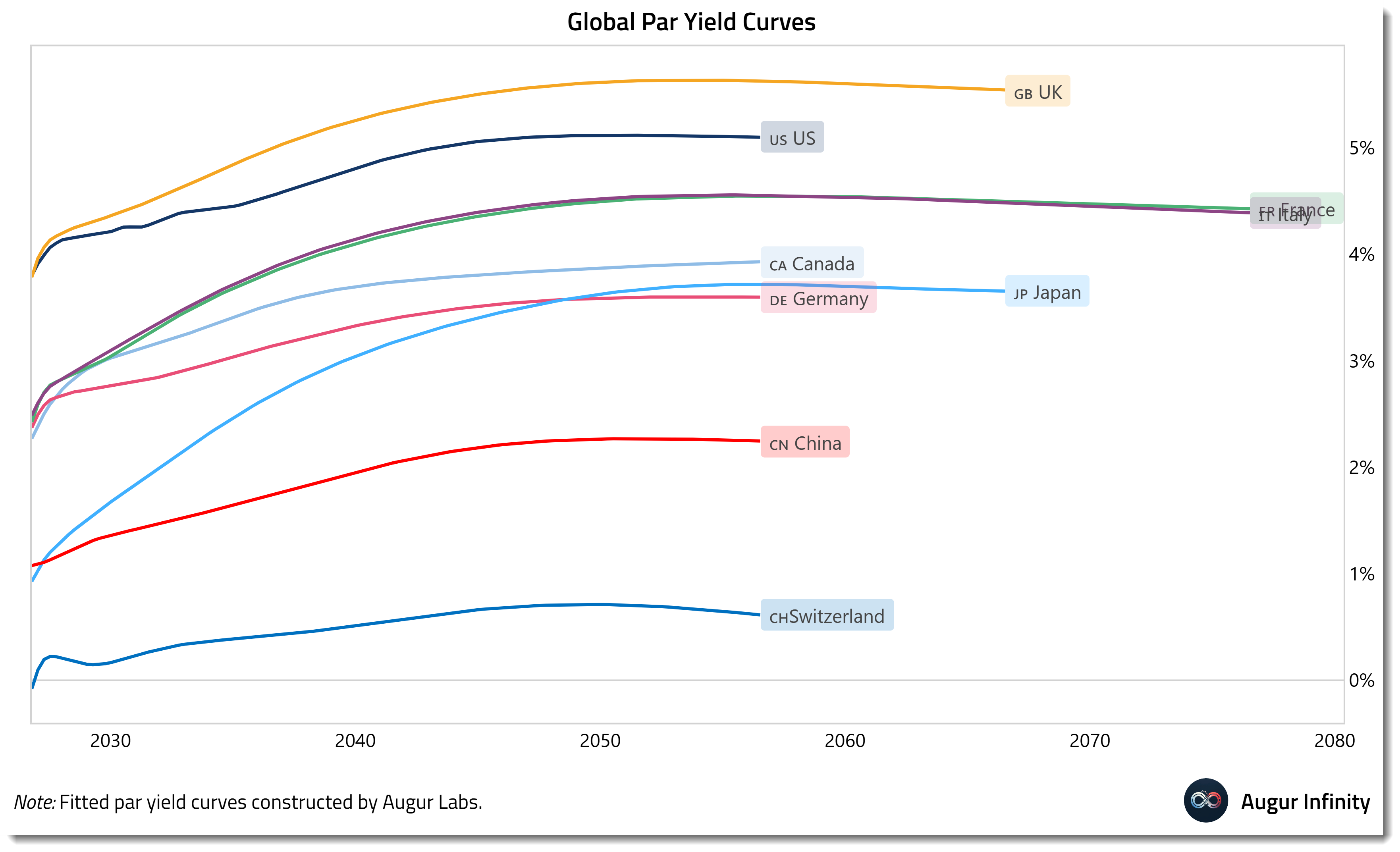

It would be darkly fitting for that kind of political theatre to coincide with bond markets throwing another tantrum at UK fiscal policy. UK gilts are topping the global sovereign bond league table in ways that will be a headache for the ‘King of the North’s incoming Treasury team.

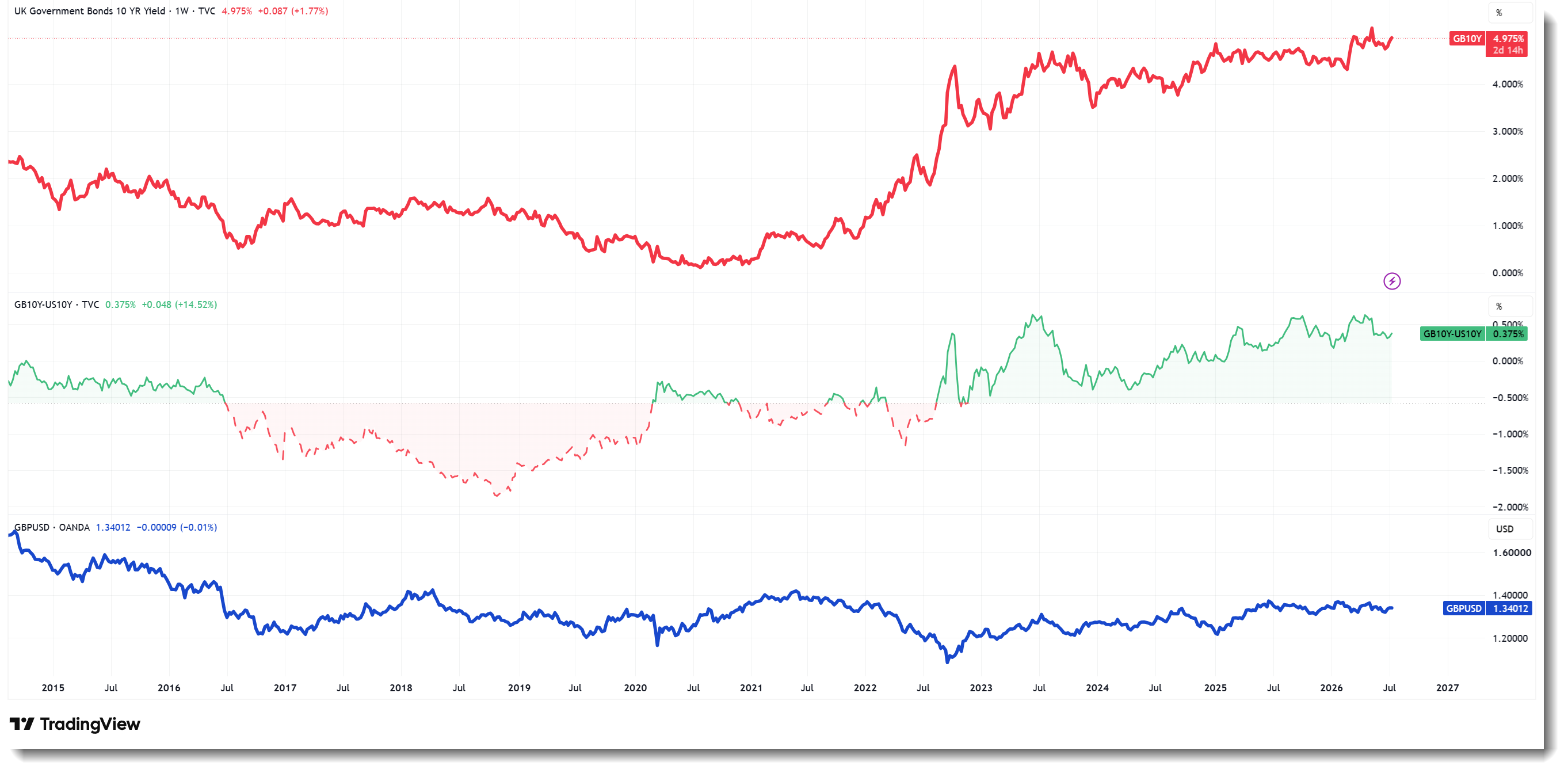

Benchmark 10-year yields are sitting at a meaningful absolute and relative (to US Treasuries) premium to Truss / Kwarteng / “lettuce” peak of late 2022.

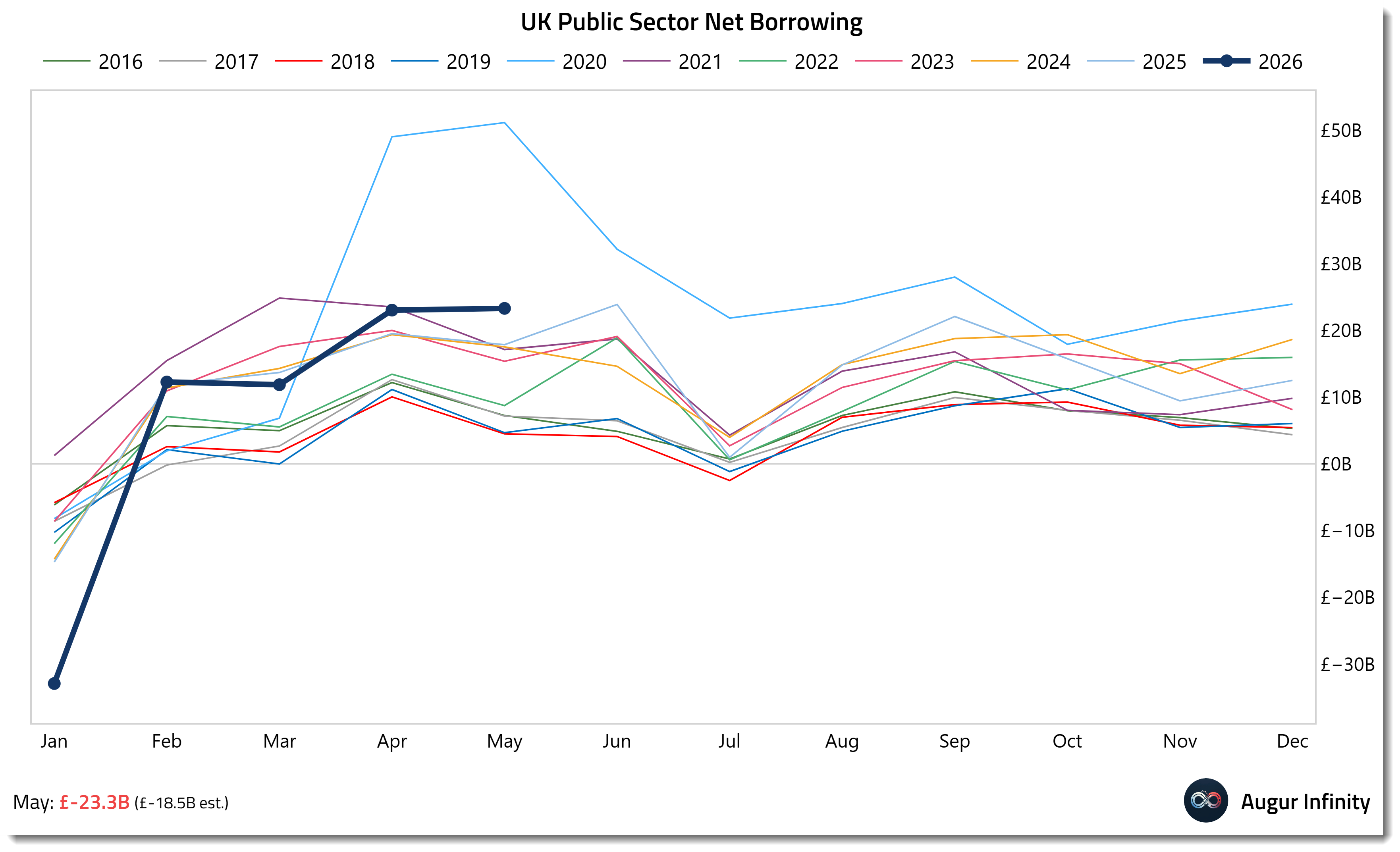

Not hugely surprising with the UK’s public sector net borrowings sitting at levels (ex-Covid) not seen since Brexit a decade ago.

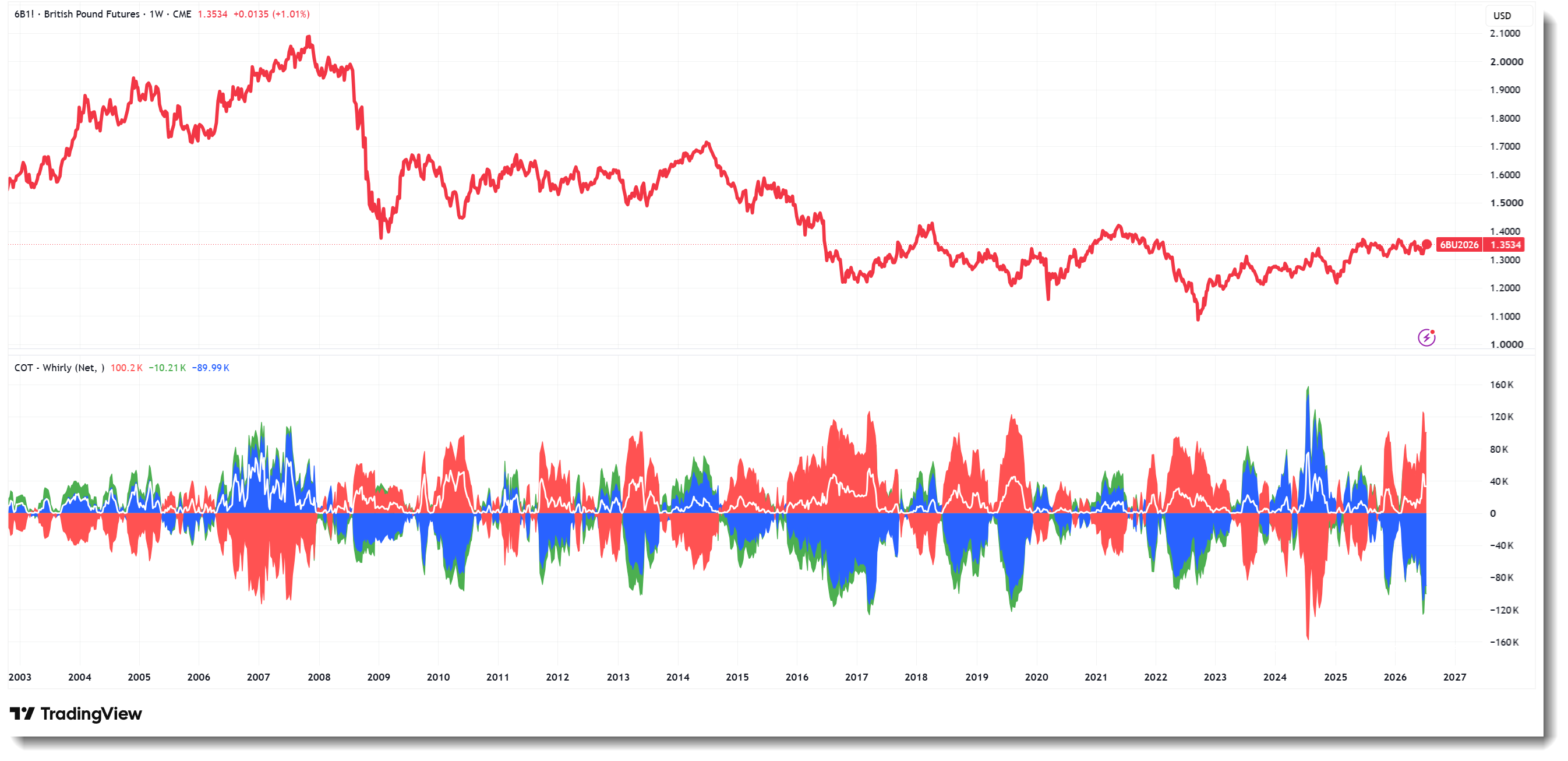

Speculative short positions in CME GBP futures are at Brexit-era extremes, with high open interest.

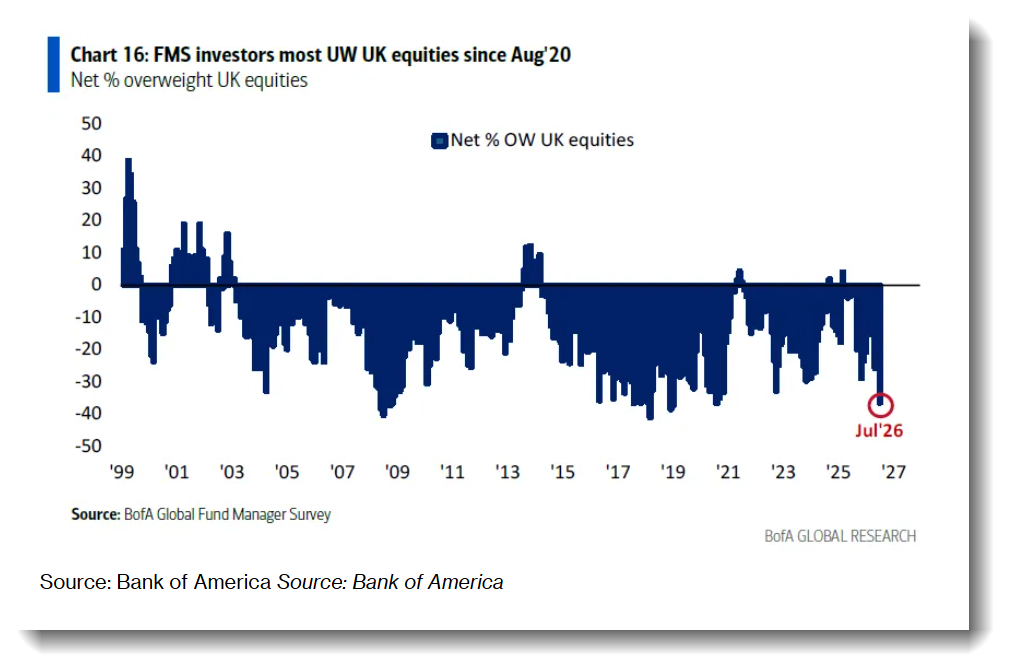

The latest BofA fund manager survey has UK equities underweights tracking in line with the political chaos period that came in the wake of the EU Referendum. Outflows by domestic UK mutual funds reached almost £20 billion in Q1, the highest of recent years.

UK assets have become the Millwall Football Club of global risk. To make matters worse, England lost against to arch foes Argentina in the semis. When the sell signals get this extreme, the 🐿️ is inclined to fade! Feels like the perfect opportunity to re-underwrite our position in UK small and mid-cap stocks.

Let’s dig in…