Be like Boaz!

Alpha from Ancient Access Products. The Blind Squirrel's 'Monday' Morning Notes. Year 4; Week 15 of 2026.

Can everyone please take a breath. We have been dealing with a hot war in the Middle East for over a month yet it is a tough eye test to find an asset class (ex crypto, SaaS and precious metals) that is actually still in a drawdown of over 10% from its 52 week highs.

Global energy, industrial and agricultural supply chains have been damaged and, in some cases - Qatari LNG trains spring to mind - the repair job will be measured in years. Yet financial asset markets are pricing the ‘all clear’ and that any longer-term economic damage will just ‘buff out’ - as the auto body shop foreman might say.

The 🐿️’s response to this week’s cease fire ‘announcements’ has not been to join the hordes reaching for a stack of blue (buy) tickets - even when it comes to positions that I really like on a (current situation-adjusted) long term view. Looking at you Brazilian equities.

Instead, this rodent prefers to continue to polish his post-war risk asset ‘shopping list’ - these include the ShinyAcorns™, EM Tech and ‘Straya Ruggedization’ baskets as well as a complete refresh of ‘EuroMIC’ - the soon to be ‘NWOMIC’ (NWO = New World Order) - basket of global defense stocks (next weekend’s report - Drey members have already had some early previews on this).

This rodent is working harder than ever - just not pushing any buttons…

But there may be some candidates for an exception…

Alpha from (old) Access Products

When it comes to public equities, I could argue that there is no reason for closed-end mutual funds (‘CEFs’) to exist in the modern day. It is not hard to understand why asset managers like these sources of permanent fee-generating capital so much, but in a modern market that has more low cost ETFs than individual stocks, what purpose do they serve?

CEFs still make complete sense - in fact I would argue they are superior to ETFs as a collective investment vehicle when the underlying asset is illiquid (e.g., private equity, credit products, real estate). As long as investors fully understand that the lack of on-demand redemption is a feature not a bug.

Investors in CEFs should expect these vehicles to trade at a (sometimes very) wide discount to the value of their underlying assets (NAV). This, however, really should not be the case when the underlying investment is liquid public shares.

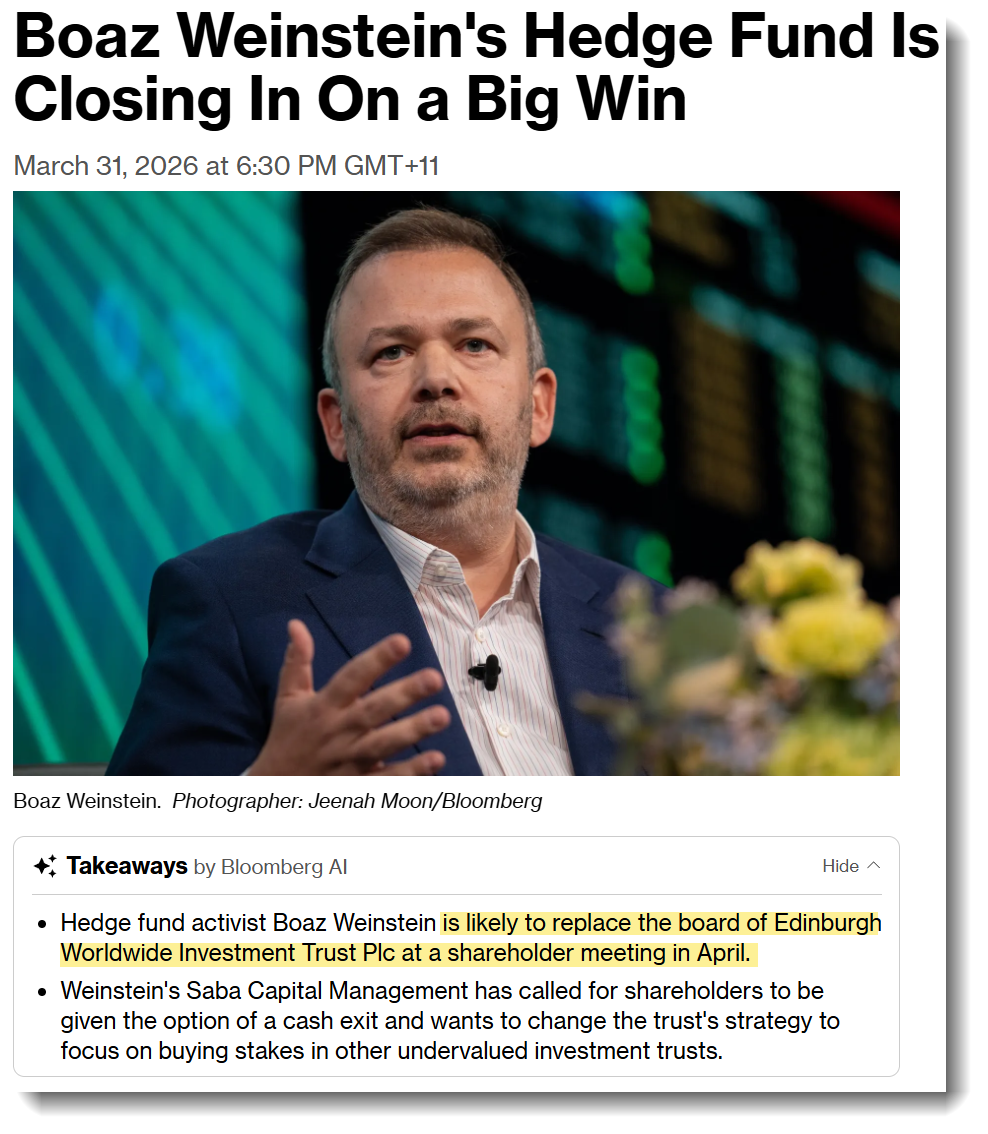

Activist investors such as Boaz Weinstein’s Saba Capital are absolutely correct when they argue that asset managers could do a much better job of shrinking these discounts by selling liquid underlying investments (at NAV) or taking on modest leverage to re-purchase or tender for discounted CEF shares in the open market.

However, it is only once Boaz parks an army of attorneys on the lawns of these asset managers and litigates to reassign the investment management contract that the fund houses reluctantly start to take action.

Back in 2023, after successful campaigns in the US, Saba’s activism crossed ‘the pond’ to shake up the sleepy world of the UK’s investment trust sector (the British version of a CEF). Weinstein continues to terrorize the clubby boardrooms of Edinburgh and the City of London to this day.

Quick History Lesson

In 1868, the Foreign & Colonial Government Trust (now known as the F&C Investment Trust (‘FCIT’) and still listed on the London Stock Exchange) was founded as the first collective investment scheme specifically designed to bring ‘stock market investing’ to those of ‘moderate means’.

The explicit original mandate was to democratize capital, allowing investors to access a diversified portfolio of high-yielding emerging market sovereign bonds and railway infrastructure projects. FCIT was famously the only investment trust share which John Maynard Keynes included in the portfolio he managed for his father in the run up to WW1. I wrote about FCIT - the original EEM 0.00%↑ in more detail last June.

These days, investment trusts are the preferred vehicle for holding illiquid alternative assets such as PE and venture capital, renewables projects and other infrastructure assets and commercial property. The closed-end structure prevents the liquidity mismatches that frequently blow up open-ended vehicles during market panics.

UK trusts maintain strong, independent boards of directors with genuine fiduciary power. It is not uncommon for a UK trust board to fire an underperforming asset manager and hand the mandate to a rival shop. Even if Boaz does not think this happens nearly enough. He’s probably right.

The origin story for US CEFs is darker. They did not hit mainstream until the “roaring (19)20s” when they gained immense popularity, utilizing unchecked leverage to offer synthetic high yields. The promoters also had an unpleasant habit of using them as dumping grounds for illiquid assets that could not be sold in the open market. When the 1929 crash hit, that leverage wiped out retail punters.

The Investment Company Act of 1940 was eventually passed a decade later to impose borrowing limits on the CEFs but the sector never recovered its luster. These days the space is dominated by yield-chasing vehicles for retail investors, heavily skewed towards ‘muni’ bonds, MLPs and option overwriting strategies.

But there are a couple of diamonds in the rough. More on that later.

The Barings Play Book

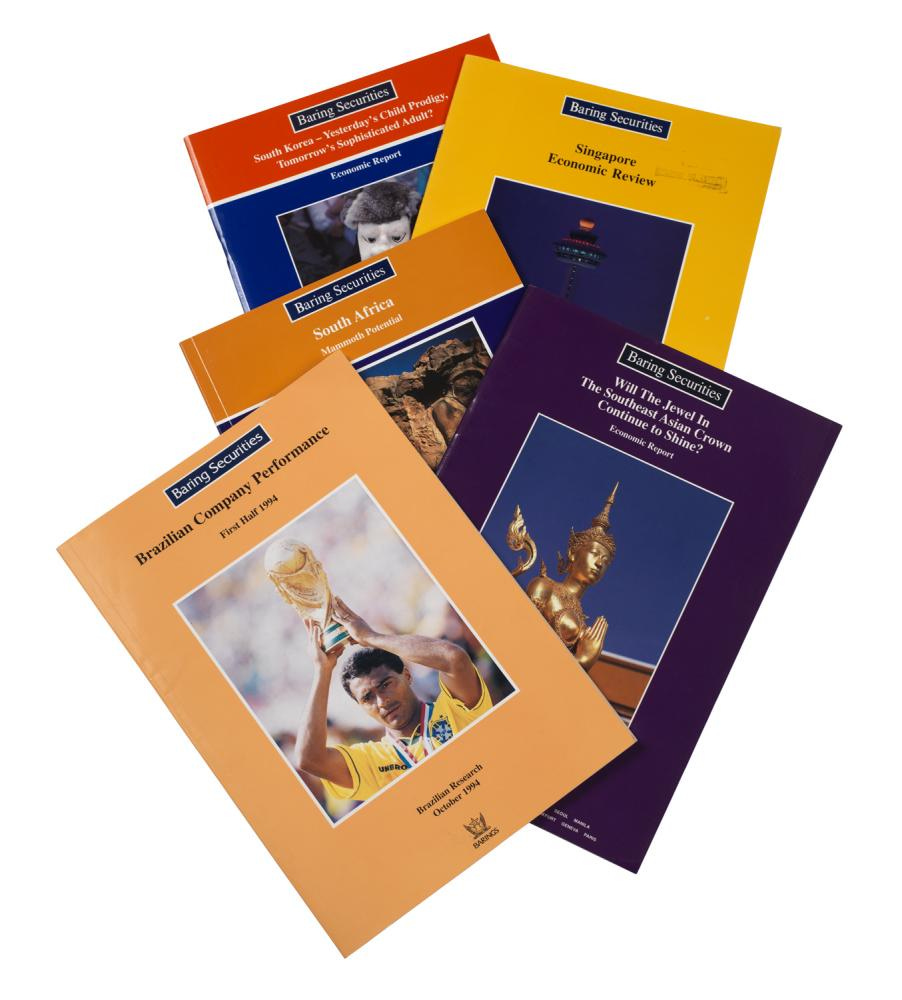

The 🐿️’s first permanent job in finance was at the soon-to-detonate British merchant bank, Barings. Baring Securities was at the forefront of emerging market investment banking in the early 1990s. There was a well established playbook.

A satellite office would be opened in Taipei / Seoul / Bangkok / Jakarta / Santiago and a research team would go straight to work writing “The Country Book” - a glossy market initiation report containing a bit of macro plus profiles of the dozen largest listed stocks - invariably a cement company, a brewery and a couple of banks.

Many of these new markets would be impossible for most (even institutional) investors to invest in directly due to either foreign ownership restrictions or the lack of local custody arrangements that would satisfy their fiduciary mandates.

Shortly thereafter, Baring Asset Management would launch its latest investment trust - “The Barings [insert name] Country Fund” as an access product for global institutional investors and wealth managers. Some of the funds even traded at a premium to NAV as investors chased the latest ‘hot’ new EM.

Within a couple of years, most large international investors had figured out their direct market access issues and the 🐿️ and his colleagues had executed London-listed GDR or New York listed ADR offerings for the blue chips in these countries - for those investors who still did not have direct access and those that did but wanted to buy their favorite EM stocks at a small discount.

The country funds had served their initial purpose and would gradually start to trade to a discount to NAV until they started to attract the attention of the ‘trust-busting’ predecessors of Boaz Weinstein. Barings’ investment bankers would be hired to organize the defense and ultimate restructuring. The circle of life was complete!

Before we get to the main topic, a quick 🐿️ PSA:

Stop press (with some closed end fund news!) An UzNIF Update! On Thursday the Uzbekistan / Templeton privatization fund announced its ‘Intention to Float’ (detailed press release) on the London Stock Exchange. This announcement means that we are likely to see deal structure and pricing information within a matter of weeks.

The🐿️ will be following this situation closely (hopefully with the assistance of his frontier market sherpa Scott ‘Yurta’ Osheroff). Current market conditions may require a much steeper discount to NAV than might normally be required. This rodent is doing the work! Link to my UzNIF report from last November below. 👇

The Opportunity

Back to those potential exceptions that might lure the 🐿️ away from his current buying strike.