Batik Shirt Comeback!

The Blind Squirrel's Monday Morning Notes, 2nd September 2024.

Story time with the 🐿️. Some Labor Day reminiscences!

Leading us to a deep value play in Southeast Asia.

Batik Shirt Comeback!

It’s Labor Day weekend and too many column inches have already been devoted to that Nvidia earnings call watch party. Some 🐿️ reminiscences to start with instead.

Let me take you back to the late Summer of 1999. This rodent is a new arrival in Asia, working in Hong Kong on the ECM desk at ING Barings. Most of team there are still desperately trying to pretend that they do not work for the Dutch Post Office a European bancassurance group and remain misty-eyed about those buccaneering days of Baring Securities which had been brought to a shuddering halt 4 years earlier by the Nikkei futures straddle selling activities of a young trader called Nick Leeson.

The vibe in Hong Kong at the time was actually remarkably upbeat given that barely a year had passed since the Asian currency crisis of 1998. Many close friends in the market had had to flee from Jakarta with barely the shirts on their backs to catch the last flight out of a city in flames and overrun by rioters the previous May.

In Hong Kong, the HKMA, the local central bank now owned a massive 10% of the Hang Seng Index having intervened to defend the HK dollar currency peg the previous summer. It will happen again Kyle 😉. I had been moved out from London earlier that year to work on the process for selling that stake down.

The 🐿️ would like to pretend that this posting was a function of this rodent’s deep and relevant expertise as related to the matter at hand. The more likely reason was that the incumbent team had zero interest in getting bogged down with the daily grind of memos and civil service briefings required by that sort of government advisory work. They had better places to be.

The 1990s had seen a few ‘Red Chip’ IPOs but the deal business out of mainland China was still a small part of the Asian investment banking fee pie. Korea and Taiwan offered up a few opportunities for bankers to earn a crust. However, the ‘Tiger’ economies of Southeast Asia were where all the action was!

Fast forward a decade and the picture could not have been more different. Asia investment banking was China. Full stop. Entry level Asian investment banking positions were really only available to native Mandarin speakers.

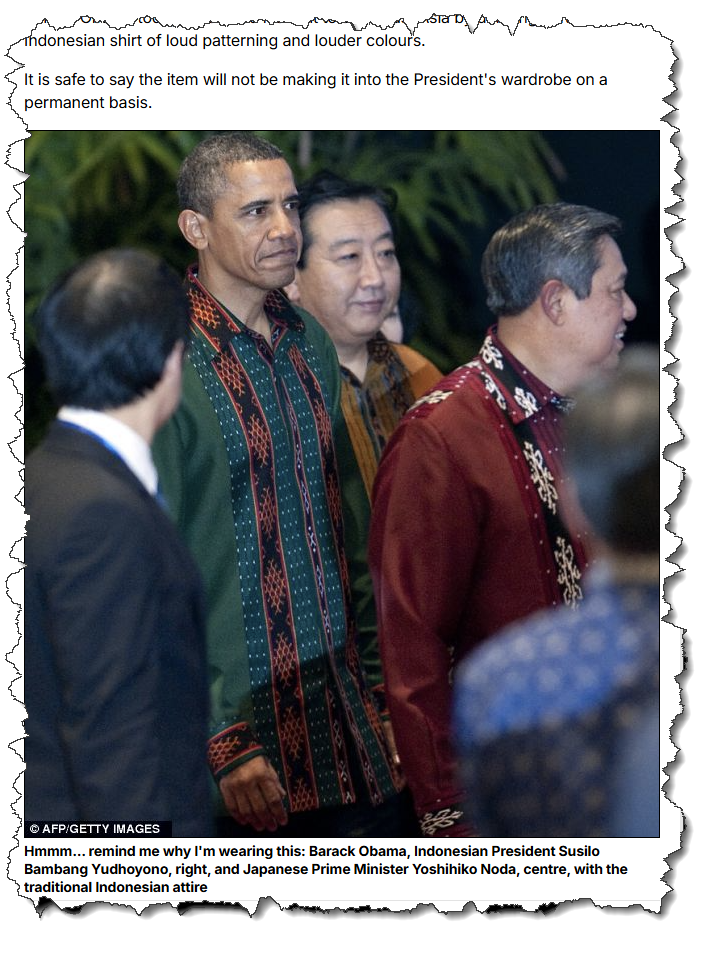

Southeast Asian capital markets business was a rounding error for the P&Ls of the global banks and pretty much everyone was looking the other way unless it was to snigger at a US President that was being forced to wear a Batik shirt at an ASEAN conference!

In the past 3 years, the institutional allergy to Chinese risk assets has largely driven a maniacal fervor for Indian equities which regular readers will know has had this rodent scratching his head. With the exception of some fleeting investor romances with Vietnam and some Covid-era ASEAN tech darlings like Sea Limited SE 0.00%↑ and GRAB Holdings GRAB 0.00%↑, the equity markets of SE Asia have largely been ignored.

Serious investor conversations about the region have largely only been in the context of the Wall Street and Hollywood implications of the 1MBD scandal in Malaysia; the geopolitics of the South China Sea shipping lanes; or of the energy transition where Indonesia is the ‘Saudi Arabia’ of nickel.

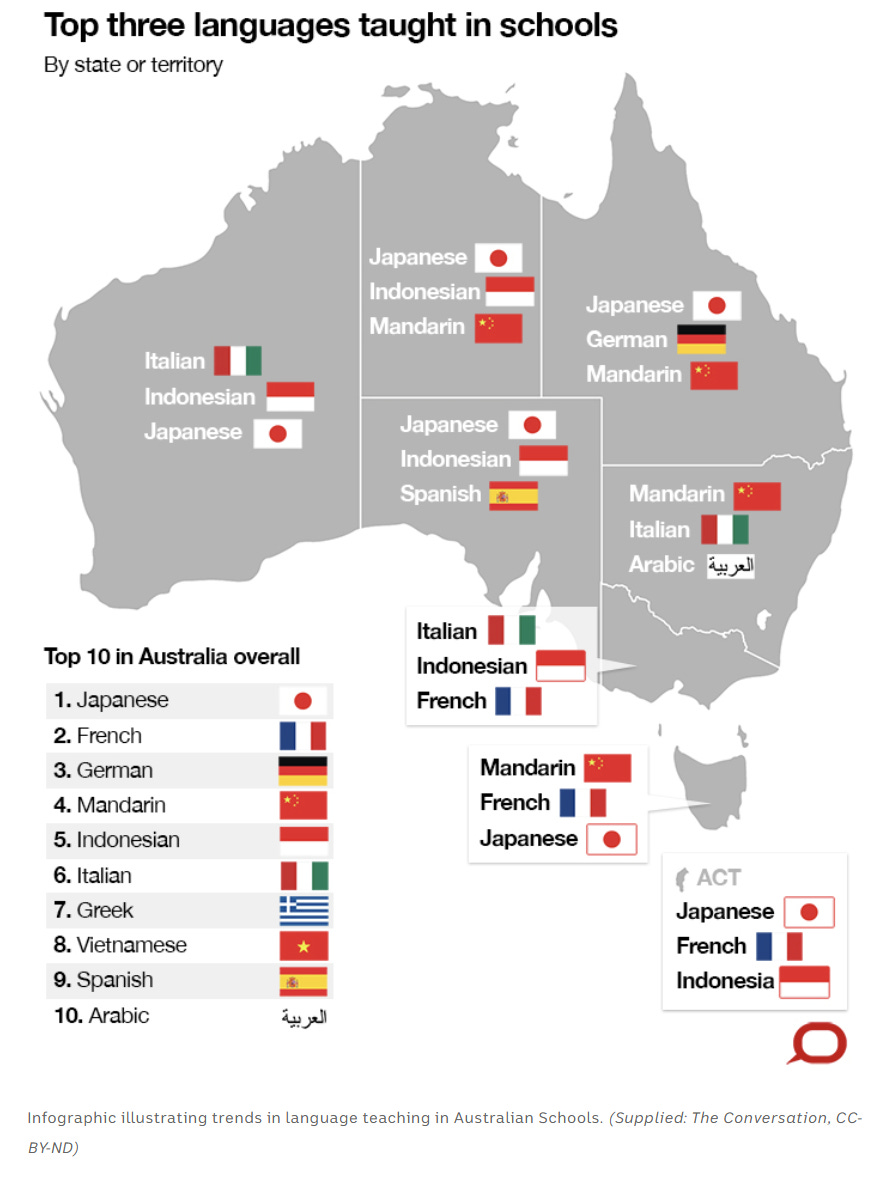

I have been thinking for some time that this could be an oversight. I remember being surprised and then thinking that of course it made perfect sense that Bahasa was one of the more popular foreign languages taught in Australian schools. Doh! Indonesia, population of 280 million, GDP of $1.4 trillion growing at 5%+ sits just off our northern shores (albeit the one with all the saltwater crocs!).

The Indonesia / ASEAN file on my PC was starting to grow thicker when my pal

led with ‘ASEAN Dawn’ in his weekly Cascade note 2 weeks ago.

Chase is a bit younger than the 🐿️. As such, this part of the world has been of negligible interest to the mainstream investment community for pretty much 100% of the time he has been involved in markets. But my friend has a great ability to see around corners and the fact that his antennae are also sensing a potential comeback for Southeast Asia is comforting.

Equity investment options. Both Indonesian and Filipino equities can be accessed via iShares ETFs that track their respective MSCI Indices.

Neither vehicle is that large or liquid. However, 🐿️ has a more interesting idea, one which brings us neatly back to those earlier reminiscences about Hong Kong in the late 1990s.

Back in 1999, ING Barings had just taken up grandiose residence on multiple stories of the newly completed IFC One office tower on Hong Kong’s harbor front. A (a pre-Leeson!) Baring Securities had signed a trophy lease on the space moments before the firm’s demise and ING takeover several years earlier!

The investment banking department was connected to the trading floor via a sweeping spiral staircase. I vividly remember the collective groan from the equity sales desk when ‘TS’, a senior corporate financier, was spotted descending those grandiose stairs 30 minutes before market close with a large grin on his face.

TS’s shiny black brogues gracing the trading floor at that time of day only meant one thing. The bank would be on the hook to raise some money after the close and any planned visits to The Captain’s Bar or other less glamorous watering holes of Central or Wan Chai would need to be put on hold. It was going to be a late night!

The fact that it was TS sauntering over to us on the ECM desk also (very much) narrowed down the alternatives of which company we would be doing a deal for that night. TS’s largest only client was building an empire from the embers of a post financial crisis Southeast Asia.

That empire is still alive and well to this day. It is spectacularly cheap and looks like it wants to break out.

Don’t miss out! Please consider becoming a paid subscriber to receive the other 60% of 🐿️ content (including the identity of this empire!), member Discord access (The Drey) and even merch!